blog

Cracks in Private Credit: How the Late Cycle Stress Test Is Really Playing Out

David Vatchev, Head of Tokenization

24 March 2026

Private credit entered 2026 in a clear late-cycle phase. This is not a systemic break, but a sharp differentiation across structures, sponsors and strategies. A large refinancing cycle across sponsor-backed loans originated during the low-rate era is approaching, creating a natural stress test for leveraged capital structures. Stronger, better-protected deals continue to fund, while weaker or aggressively structured transactions are coming under increasing pressure. For allocators, the question has shifted from “Is private credit the new bank?” to “Which parts of private credit are structurally resilient?”

How stress is showing up

Stress is becoming visible in the plumbing of the market rather than only in headline defaults. Workout activity and documentation changes are a key signal. Amend-and-extend transactions, maturity pushes and covenant resets are increasingly preferred to clean refinancings, particularly in cyclical or highly leveraged deals. While formal defaults have risen, the more important indicator is the broader increase in stressed situations, PIK toggles and tighter cash-leakage controls.

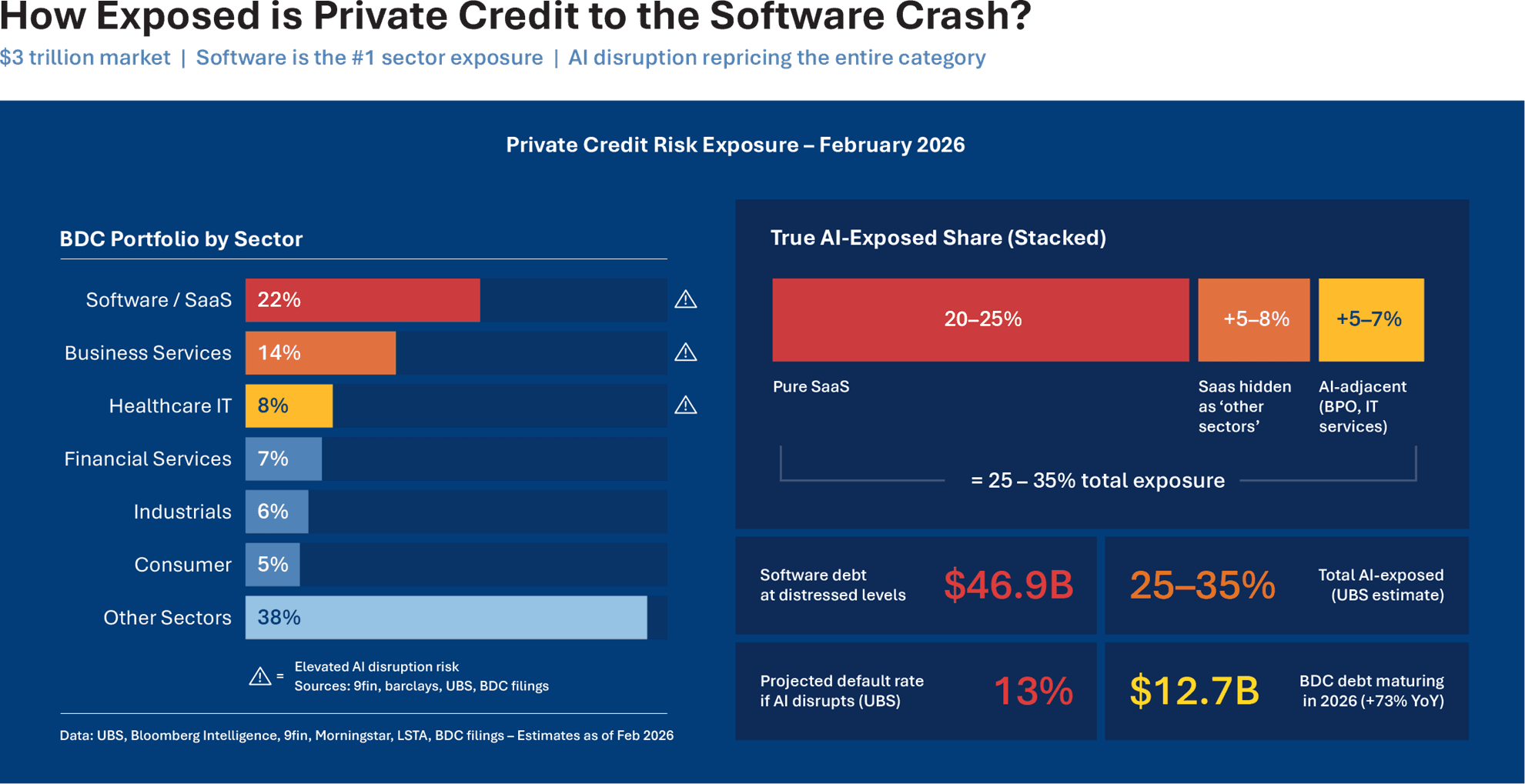

Managers are spending more time on waivers, restructurings and recoveries, and less time deploying into large, plain-vanilla sponsor transactions. At the same time, new deals are being priced at wider spreads, and the gap between top-tier sponsors and the rest of the market has widened in both pricing and access to capital. Software provides a clear example of this dynamic. Now one of the largest sector exposures in private credit, the sector faces pressure as AI disruption and valuation compression collide with high leverage.

Recent analysis suggests roughly 25% of private credit deals are linked to SaaS companies, with around 20% of the USD 3 trillion market exposed to software and AI-sensitive industries. Syndicated and private credit loans backing large take-privates such as Citrix, Zendesk and Avalara have appeared on secondary trading lists at discounts, while BDCs and large managers report increasing stress within software portfolios:

Source: Saastr

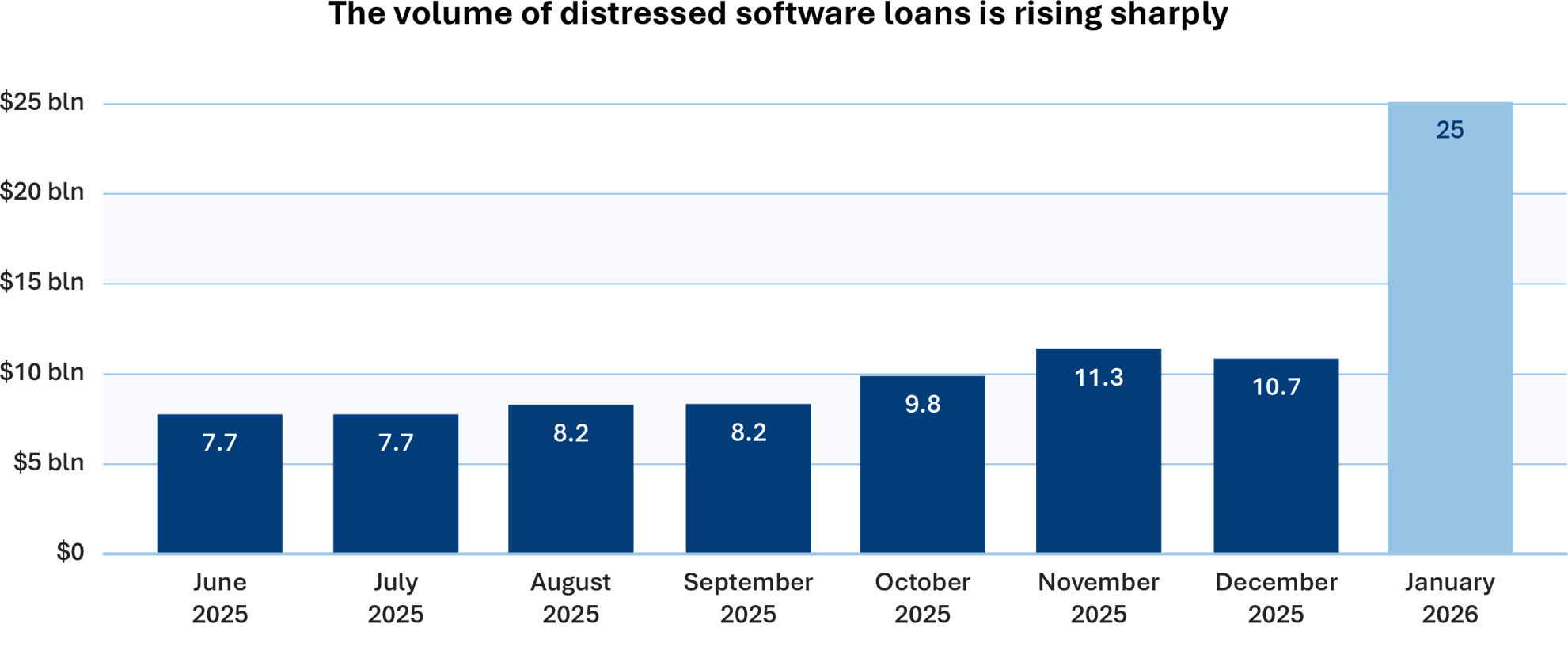

According to PitchBook data, software loans account for nearly a third of distressed credit in liquid markets, highlighting the sector’s growing role in private credit risk dispersion:

The gap between best-in-class sponsors and borrowers and the rest of the market has widened, both in pricing and access to capital, with software-exposed credits a prominent example of this dispersion. Data also suggests that stress, while still manageable, is gradually broadening through increased workouts, PIK structures and a growing number of stressed situations.

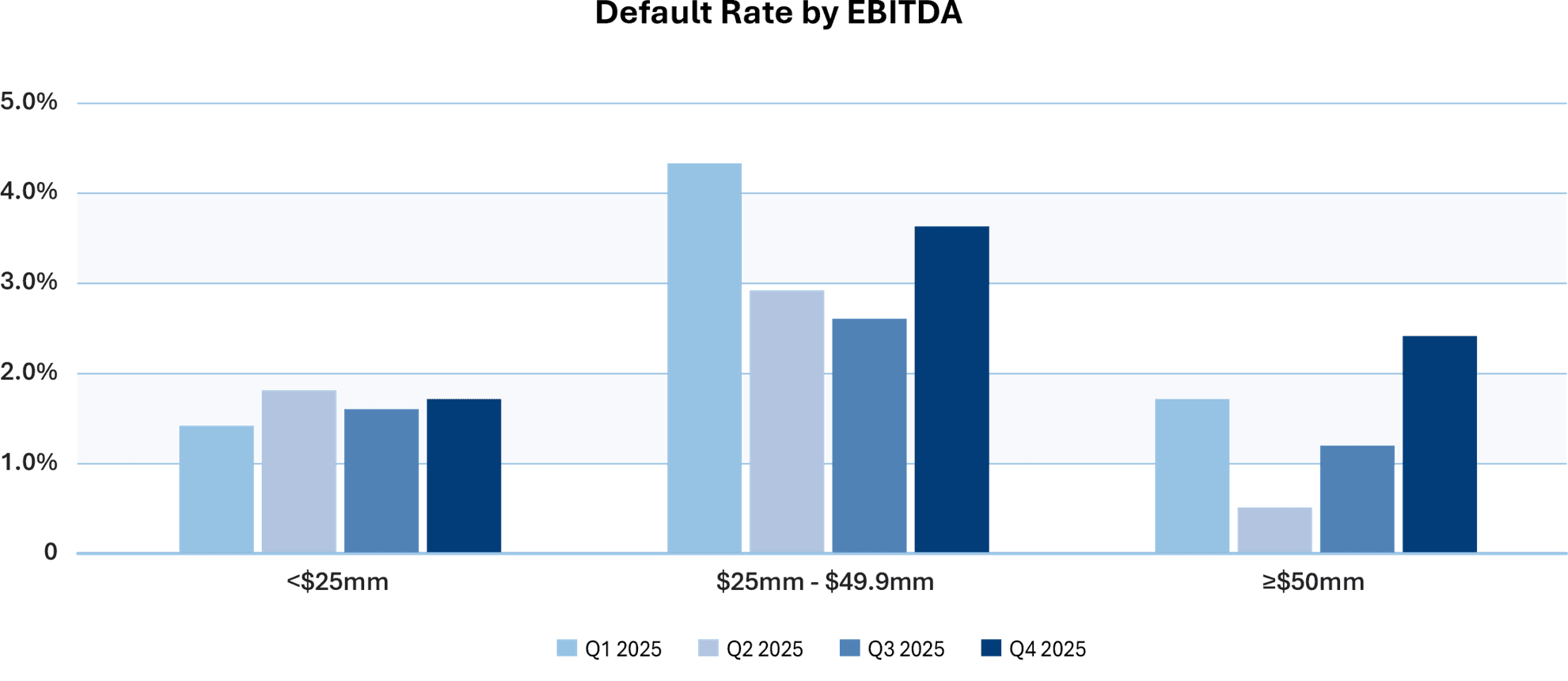

Strategies reliant on rapid exits through IPOs, secondary buyouts or easy asset sales are also facing headwinds in a slower M&A environment and a more selective equity market. Portfolios with large, concentrated positions in a small number of borrowers or sectors are therefore experiencing volatility more acutely than highly granular books.

Why senior, short‑duration, granular credit stands out

Senior, short-duration, granular credit behaves differently because of how risk is carried and repaid, not simply because of its label. Short-dated, self-liquidating exposures mean each collection cycle reduces risk and refreshes the portfolio, allowing it to adjust more quickly to changing conditions.

Structures anchored in receivables, invoices, or operating cashflows generate frequent performance data and rely less on modelled enterprise values. Issues tend to surface earlier through delinquency or collections trends, providing greater visibility and more time to intervene. Portfolios built from thousands of small exposures can absorb individual defaults without destabilising overall returns (though it should be noted that granular portfolios may still experience losses in adverse market conditions). This contrasts with single-name or small-basket portfolios, where stress in one borrower can potentially materially influence outcomes.

The role of asset‑backed finance

Asset-backed finance (ABF) has moved from a specialist niche to a core building block in diversified private credit allocations. Allocators increasingly utilise ABF strategies to access private credit returns with different risk drivers and lower correlation to sponsor-backed corporate lending.

Lending at the operating-asset level, with direct claims on cashflows and collateral, creates a distinct risk profile. Unlike sponsor-backed direct lending, where exposure can hinge on a single borrower, asset-backed finance relies on diversified pools of receivables whose repayment is tied to underlying cashflows rather than enterprise value.

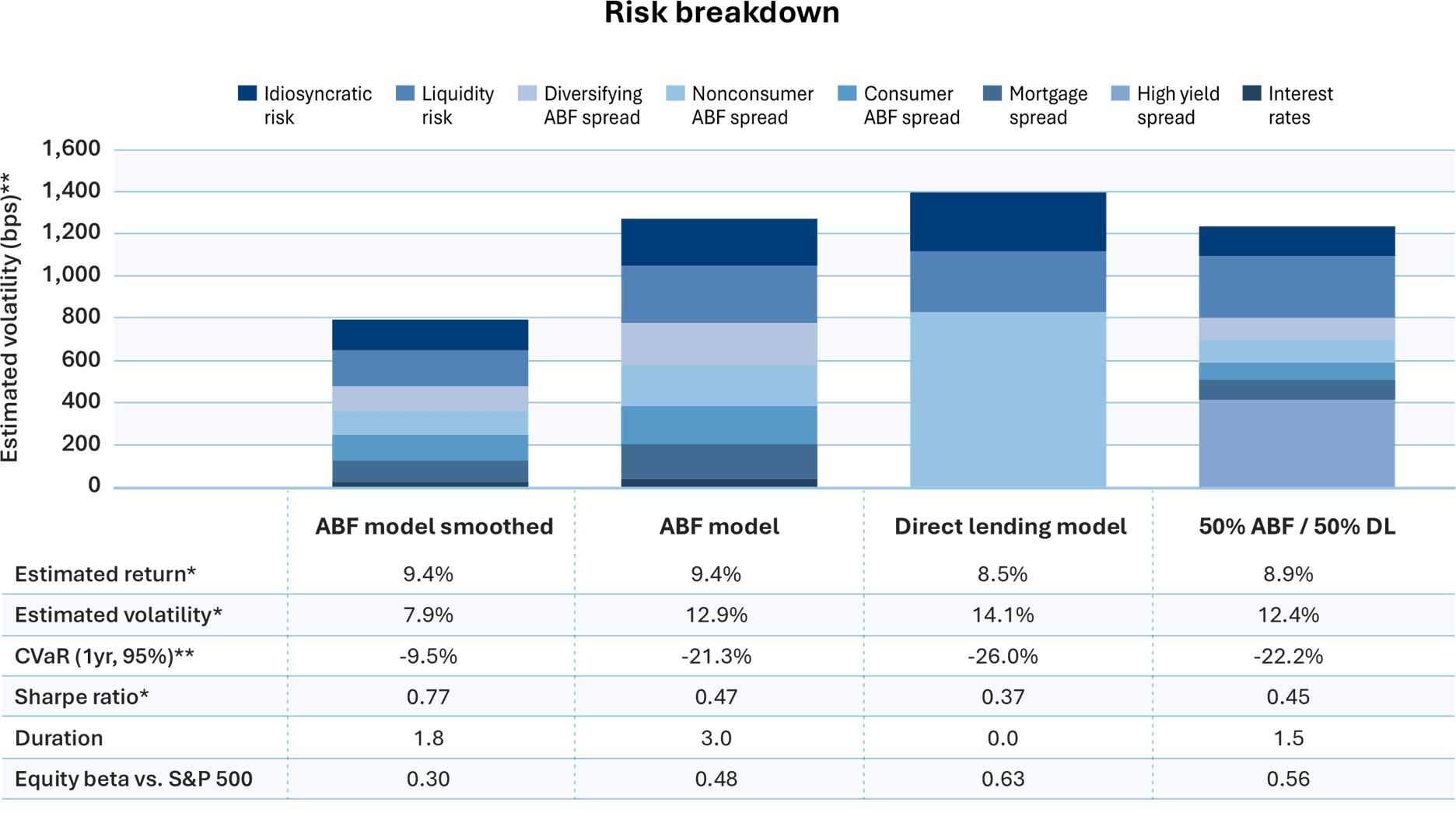

In stress scenarios, this structure can translate into clearer workout options, more predictable recoveries, and greater scope for active management. PIMCO recently modelled the risk-return characteristics of private asset-backed finance versus corporate direct lending, highlighting the diversification benefits of combining the two strategies:

What comes next for private credit

The handling of the 2026–2027 maturity wall across sectors and sponsor types will be a key test of how deep and selective private credit liquidity really is. Many portfolios originated during the low-rate era now face refinancing in a structurally higher-rate environment, creating a natural stress test for leveraged capital structures.

At Fasanara, we expect the pendulum on covenants and structures to continue swinging back toward lender protections. The speed and extent of that shift will heavily influence the quality of this vintage. As more performance data emerges, dispersion between strategies tightly aligned to asset-level cashflows and those more reliant on financial engineering is likely to widen.

The coming period will not determine whether private credit survives, but which underwriting models prove resilient. For allocators, that argues for moving away from treating “private credit” as a single bucket and toward more granular risk budgeting within the asset class.

1Asset-backed finance strategies carry specific risks, including but not limited to credit risk, liquidity risk, and the potential for loss of capital. Past performance is not a reliable indicator of future results.

Disclaimer This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell, or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investors or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with their financial professionals. The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Past performance does not predict or guarantee future results. Investing involves risk; principal loss is possible. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. Fasanara Capital Ltd, is authorised and regulated by the Financial Conduct Authority (“FCA”).

Important information on risk Investing involves risk. The value of any investment and the income from such can go down as well as up, and you may not get back the full amount invested. Past performance is not a guarantee of future returns. Changes in the rate of exchange may also cause the value of overseas investments to go up or down. This information represents the views of Fasanara Capital Ltd and its investment specialists. It is not intended to be a forecast of future events and/or guarantee of any future result. Information was obtained from third party sources which we believe to be reliable but are not guaranteed as to their accuracy or completeness. There is no assurance that an investment will provide positive performance over any period of time. This information does not constitute investment research as defined under MiFID.