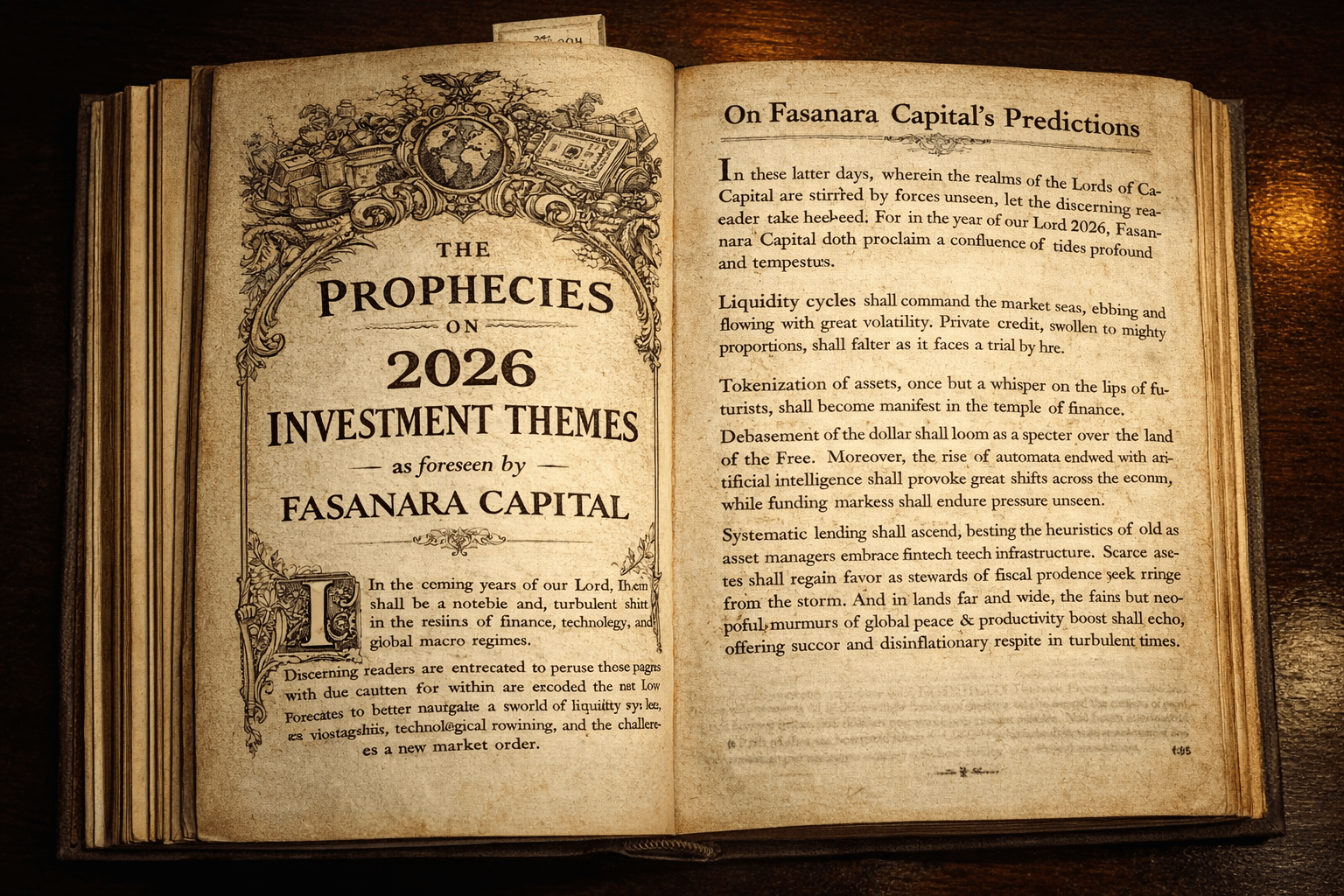

Fasanara Capital's Key Themes for 2026

Francesco Filia

29 January 2026

A framework for navigating a world of liquidity cycles, asset inflation, credit fragility, and technological rewiring.

1. Regime Change: Liquidity Cycles Dominate All Asset Pricing

2026 marks a further departure from the 2010–2020 low-volatility, QE-supported market regime. Global liquidity is increasingly seen as a significant factor influencing asset prices, though outcomes remain uncertain and subject to multiple variables.

The defining characteristic of the post-2020 world is not inflation or geopolitics per se, but the end of predictable liquidity. Markets are no longer governed by stable discount rates and slow-moving fundamentals, but by abrupt expansions and contractions of global dollar liquidity. In such an environment, asset prices respond less to valuation than to funding conditions, margin availability, and balance sheet constraints. This may favour investors who can sense liquidity inflection points early and manage portfolios dynamically, rather than those anchored to equilibrium assumptions that no longer hold.1

Fasanara's view:

- Tactical liquidity-based models gain relevance over valuation-based arguments.

- Rapid swings in global dollar liquidity require high-frequency macro sensing and adaptive risk positioning.

- Multi-asset liquidity fragility becomes a core portfolio risk.

2. Cracks in Private Credit: The Late-Cycle Stress Test Begins

Incoming is the first systemic stress in private credit after years of explosive growth, covenant erosion, and risk-shifting.

After a decade of rapid expansion, private credit now confronts the arithmetics of higher rates and tighter refinancing conditions. This is not a systemic collapse, but a long-overdue differentiation between robust, data-driven underwriting and structures built on cheap leverage and optimistic assumptions. The stress will be uneven, favouring seniority, short duration, and diversification over financial engineering. In this sense, the coming adjustment is less a crisis than a re-pricing of discipline.

Fasanara's view:

- Not a collapse, but a sorting-out: Platforms with robust origination and data-driven underwriting may be better positioned in periods of stress.

- Financing costs remain structurally higher → weaker sponsors struggle with refinancing cliffs.

- Senior secured, short-duration, granular credit benefits from flight-to-quality and stable carry.

3. Tokenization & Digital Market Infrastructure Hits Escape Velocity

The industry reaches true institutional adoption: capital markets begin migrating to tokenized rails for real-world assets (RWA), settlement, collateral mobility, and capital efficiency.

In our view, Tokenization is no longer a speculative experiment but an infrastructural shift in how capital markets function. The migration of assets onto programmable rails promises faster settlement, improved collateral mobility, and enhanced transparency. For private credit, this may represent a structural improvement: cashflows become observable, risk becomes measurable in real time, and liquidity ceases to be purely episodic. As with previous financial revolutions, the winners will be those who integrate early and shape standards rather than merely adopt them.

Fasanara's view:

- Fasanara becomes both a supplier (credit portfolios, trade finance assets, invoice pools) and a beneficiary (improved liquidity, reduced settlement friction), however, the impact of these developments remains subject to market and operational risks.

- Tokenized private credit becomes an investable asset class, with transparent cashflow data and on-chain risk visibility.2

- Partnerships with fintech rails and digital custodians accelerate.

4. Dollar Debasement Risk Returns: Scarce Assets Regain Appeal

If the “New Fed Chair doesn’t play by the rules,” a Grey Swan event may unfold—YCC, policy slippage, or re-expansion of the balance sheet—scarce assets and alternative stores of value outperform.

The credibility of fiat systems ultimately rests on restraint. Should political or institutional pressures force renewed monetary accommodation, the risk of gradual debasement re-emerges. In such circumstances, assets that combine scarcity with cashflow resilience tend to outperform. This is not a rejection of fiat money, but a recognition that portfolios must be constructed for regimes where policy discipline cannot be taken for granted.

Asset classes benefiting:

- Bitcoin & digital monetary assets

- Gold, energy infrastructure

- Cashflow-generative short-duration credit

- Hard-tech equities

Fasanara's view:

Exposure to real assets, liquid alternatives, and digital asset strategies may help diversify portfolios.

5. AI Boom, AI Bust, or AI Productivity Surge? All Three at Once

Financial markets struggle with simultaneity. AI may well disappoint equity investors even as it transforms the real economy. Productivity gains, automation, and cost compression are likely to be disinflationary, yet disruptive to incumbent business models. For credit and macro investors, this creates nonlinear outcomes: lower inflation does not guarantee stability, and efficiency gains may coexist with volatility. The challenge lies in distinguishing financial hype from economic substance.

2026 is the year AI bifurcates:

- Public AI equities may enter a correction

- Meanwhile, underlying AI adoption in the real economy accelerates, lifting productivity and lowering marginal costs in many sectors.

Fasanara's view:

- AI-driven underwriting, risk modelling, anomaly detection, and auto-reconciliation systems become competitive moats.

- AI productivity shocks may be disinflationary, resulting in bond volatility increasing, which leads to credit spreads behaving nonlinearly.

6. Global Funding Stress: Repo, Basis Trades, and Hidden Leverage Come Into View

A Grey Swan scenario—“Liquidity gets pulled; funding markets squeeze”—is increasingly plausible.

Modern finance is held together by fragile plumbing. When funding markets tighten, leverage unwinds rapidly, correlations rise, and assets previously deemed liquid become anything but. The danger lies less in visible leverage than in embedded, maturity-transforming strategies reliant on continuous refinancing. In such episodes, assets with self-liquidating cashflows and short duration regain their appeal as genuine safe harbours.

Implications:

- Basis trades unwind, leading to cross-asset volatility spikes.

- Hidden leverage in private funds becomes visible.

- Demand for self-liquidating, high-granularity receivable pools may increase.

7. From Finance to FinTech Infrastructure: The Rise of Platform Capital

Capital allocators increasingly integrate with technology platforms, creating hybrid entities that originate, underwrite, service, and fund at scale.

Capital allocation is increasingly inseparable from technology. The boundary between asset managers, lenders, and infrastructure providers is eroding, replaced by integrated platforms that originate, underwrite, service, and fund credit in a single loop. This shift mirrors earlier industrial transformations: scale, data, and systems matter more than brand or balance sheet alone. The future belongs to those who control the rails rather than merely ride them.

For Fasanara:

- The model evolves from asset manager to infrastructure provider + ecosystem orchestrator.

- Hybrid rails (data + credit + liquidity) may offer operational efficiencies compared to traditional models.

- Data exhaust from fintech partners drives superior risk scoring and early-warning signals.

8. Systematic, Data-Driven Credit Outperforms Discretionary Lending

In an era of volatility, dispersion, and noisy signals, systematic models become essential.

In volatile environments, intuition is unreliable. Systematic credit models, continuously fed with borrower-level and macro data, offer a decisive advantage over episodic, discretionary judgment. This does not eliminate risk, but it allows earlier detection, faster response, and consistent scaling. As credit markets fragment, dispersion becomes an opportunity for those equipped to measure it precisely.

Key drivers:

- Borrower-level real-time data (bank feeds, ERP, payments).

- Automated servicing and anomaly detection.

- Predictive credit models leveraging high-frequency macro indicators.

Fasanara's view:

A long-standing quantitative DNA + machine learning underwriting + digital origination partners (please note that, as with any form of investing, this approach carries risk and does not guarantee superior outcomes).

9. The Era of “First Principles” Credit Risk Arrives

Investors increasingly abandon traditional credit heuristics (ratings, covenants, backward-looking financials). Rather, they are focussing on structural risk dimensions.

The 3 Foundational Dimensions of Fasanara's model:

- Leverage

- Duration / Maturity

- Diversification

In our view, traditional credit analysis has relied excessively on labels, ratings, and backward-looking accounts. In a nonlinear world, investors increasingly return to fundamentals: leverage determines fragility, duration determines exposure to shocks, and diversification determines survivability. We think this framework is more relevant in determining risk than IG grading status. Portfolio construction approaches vary, and some investors focus on leverage, duration, and diversification.