blog

From Yield Engine to Liquidity Bridge: Asset-Based Finance's Role in Institutional Portfolios

David Vatchev

27 January 2026

Introduction

Asset-based finance (ABF) sits at an inflection point. What was once primarily positioned as a yield engine within private credit portfolios is increasingly valued for predictable amortisation, structural resilience, and liquidity-like characteristics that support portfolio construction under uncertainty. This shift reflects a broader reassessment of private markets. Institutional allocators are placing greater emphasis on strategies that deliver realised cash flows, structural discipline, and balance-sheet optionality, rather than relying solely on headline return metrics.

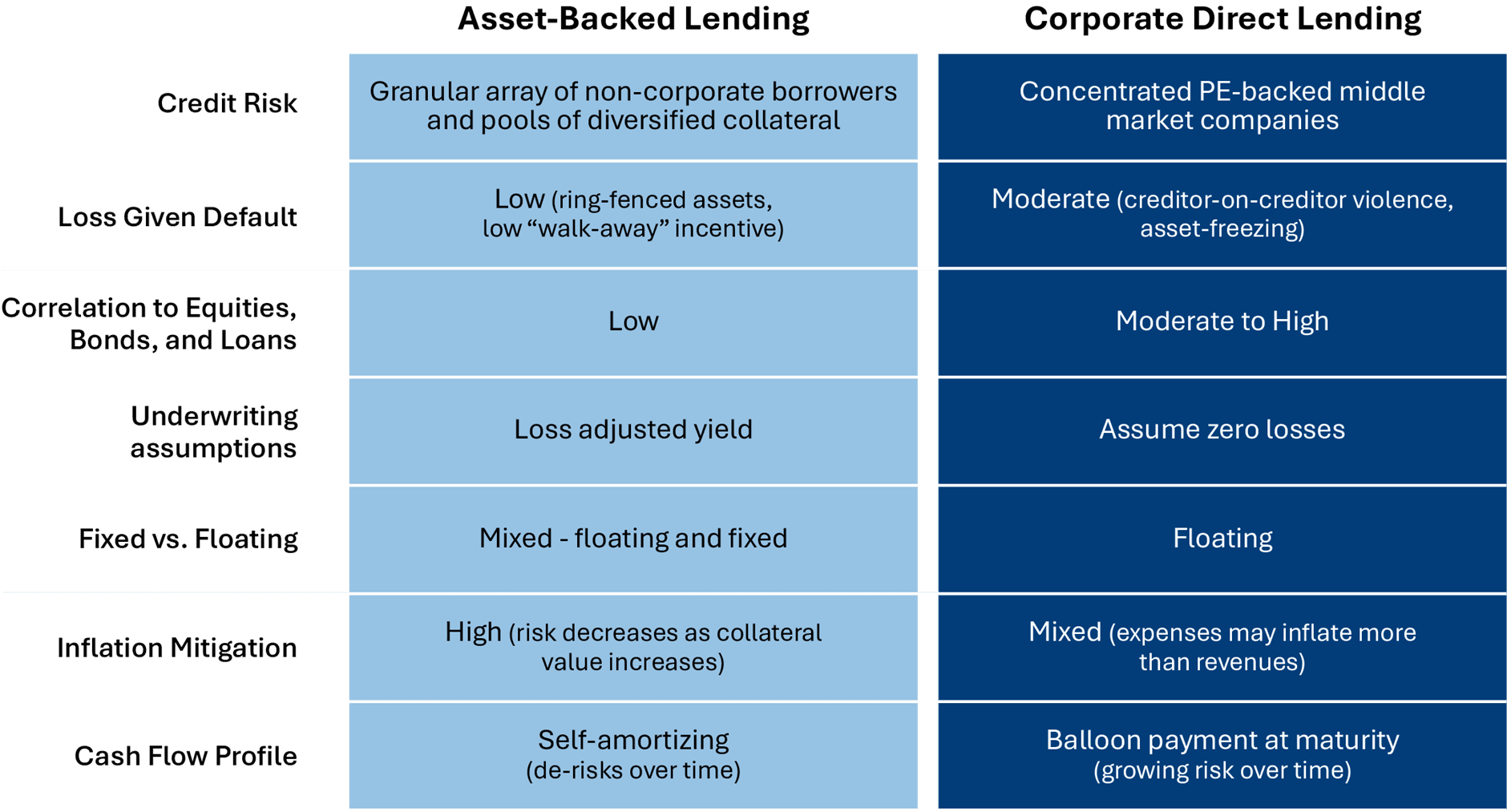

A Structurally Different Flavour of Private Credit

ABF refers to financing secured by contractual cash flows from identifiable assets such as receivables, leases, or instalment payments. The assets themselves collateralise the financing and directly support repayment. This contrasts with unsecured corporate lending, where repayment is primarily dependent on borrower cash flows and refinancing conditions.

Source: TCW

A defining feature of ABF is built-in amortisation. Principal is returned alongside interest throughout the life of the facility, rather than being deferred to a terminal maturity. These cash flows can be reinvested or retained, providing a natural source of liquidity and progressive risk reduction as portfolios season.

Market Stress and Liquidity Repricing

The market dislocations of 2022–23 exposed the fragility of many liquidity assumptions across private markets. Several semi-liquid and interval strategies encountered pressure as redemption promises proved difficult to honour under stress.

Against this backdrop, ABF has re-emerged as a structurally resilient form of non-bank capital. By financing assets with reliable contractual cash flows and short durations, ABF provides liquidity that is generated internally through asset behaviour rather than dependent on secondary markets or refinancing cycles. In this sense, ABF functions as a practical liquidity bridge between volatile public markets and long-dated private assets.

Looking ahead to 2026, ABF portfolios occupy a strategic position within institutional allocations, particularly in the context of potential “grey swan” risks:

-

Sticky inflation & interest rate unpredictability Prolonged price pressures could sustain interest-rate volatility and challenge long-duration fixed-income exposures.

-

Geopolitical escalation & supply chain disruptions Renewed or intensified conflicts may disrupt trade flows and trigger risk-off shocks across global credit markets.

-

AI-driven valuation distortion & risk repricing Concentrated optimism in technology sectors raises the risk of sharp repricing events and market-wide liquidity compression.

-

Erosion of dollar dominance and structural shifts in payments Structural currency transition risk could reframe reserve asset status and cross market liquidity dynamics.

In this environment, strategies with stable amortisation mechanics provide a financial anchor. By delivering in-cycle cash flows and predictable principal return, ABF supports portfolio resilience without relying on favourable market conditions.

As a result, ABF is increasingly reframing how core private credit allocations are constructed:

• Lower duration risk than traditional leveraged loans. • More predictable cash delivery than opportunistic credit strategies • Amortising cash flows relative to longer-dated, bullet-maturity structures

These characteristics position ABF as a functional allocation, above and beyond a source of incremental yield.

What Differentiates Winners?

While the ABF universe has expanded rapidly, outcomes remain highly dependent on structure and execution. Certain attributes consistently correlate with durable performance and liquidity quality:

-

Liquidity design: Amortisation driven principal return reduces reliance on exit windows or secondary market depth.

-

Collateral and data discipline: Granular, asset-level data and near-real-time monitoring enable more accurate risk assessment and cash-flow validation.

-

Tech-enabled risk oversight and governance: Automated monitoring, integrated dashboards, and stress analytics improve early-warning detection and portfolio control.

Sources: Alternative Credit Investor, CSC Global, Deal Catalyst ABF Survey

Fasanara’s Approach to ABF

ABF has been central to Fasanara’s investment approach for more than a decade. The firm’s focus on structured receivables, fintech-enabled origination, and short-duration cash-flow assets predates the recent reappraisal of liquidity and risk within private credit markets.

Fasanara began building ABF strategies at a time when private credit was largely defined by direct lending and long-dated corporate exposure. From inception, portfolio construction, risk management, and liquidity design have been shaped by the practical realities of managing large volumes of granular, short-dated assets across multiple market cycles.

Receivables as the Structural Foundation

Fasanara’s ABF strategies are anchored in receivables and similar contractual cash-flow assets that amortise naturally over short horizons. These assets are typically linked to real economic activity, including trade receivables and digital invoices generated by SMEs.

Portfolios are composed of very large numbers of small, independent exposures across geographies, sectors, and counterparties. This degree of loan-level diversification materially dampens idiosyncratic risk and contributes to the stability of portfolio cash flows over time.

A Technology Platform Built for Scale

Managing ABF portfolios at institutional scale requires a fundamentally different operating model from traditional credit. Millions of individual exposures, multiple originators, and diverse jurisdictions introduce complexity that cannot be addressed through periodic reporting or manual oversight.

Fasanara’s ABF platform has evolved to integrate originators into technology infrastructure to enables asset-level data ingestion and continuous risk monitoring.

Liquidity by Design

Recent market cycles have reinforced that liquidity is driven by asset behaviour rather than fund structure labels. Fasanara’s ABF strategies rely on amortisation as the primary source of liquidity, with principal repayment embedded in the asset itself and observable at the individual exposure level.

This liquidity profile reflects first principles portfolio design built around short asset duration, zero structural leverage, and extreme granularity, materially reducing asset–liability mismatch from the outset.

Structural Discipline Tested Across Cycles

These characteristics have been tested across multiple market environments, including COVID-era dislocations, rate hiking cycles, and periods of fintech specific credit stress. The emphasis on construction over optimisation has allowed portfolio behaviour to remain stable even as market conditions shifted materially, while the same structural features also create optionality in how portfolios can be accessed, without compromising underlying credit discipline.

Conclusion: Leading with Liquidity in 2026

As institutional allocators assess private markets against the backdrop of persistent macro uncertainty, the premium on dependable cash flows and structurally embedded liquidity becomes increasingly pronounced.

ABF is evolving from a yield engine into a liquidity bridge that helps anchor portfolio construction across cycles. For allocators focused on risk discipline, transparency, and balance-sheet flexibility, this transition reflects a structural shift in how private credit is understood and deployed.

Disclaimer

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell, or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investors or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with their financial professionals. The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Past performance does not predict or guarantee future results. Investing involves risk; principal loss is possible. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. Fasanara Capital Ltd, is authorised and regulated by the Financial Conduct Authority (“FCA”).

Important information on risk

Investing involves risk. The value of any investment and the income from such can go down as well as up, and you may not get back the full amount invested. Past performance is not a guarantee of future returns. Changes in the rate of exchange may also cause the value of overseas investments to go up or down. This information represents the views of Fasanara Capital Ltd and its investment specialists. It is not intended to be a forecast of future events and/or guarantee of any future result. Information was obtained from third party sources which we believe to be reliable but are not guaranteed as to their accuracy or completeness. There is no assurance that an investment will provide positive performance over any period of time. This information does not constitute investment research as defined under MiFID.