blog

Local Investing at Scale: SME Working Capital Finance for LGPS Pools

Sebastian Maciocia, Director of Capital Formation, UK

23 June 2026

This article reflects the views of Fasanara Capital Ltd as at the date of publication. The observations and opinions expressed are intended for general discussion purposes only

The next phase of Local Government Pension Scheme reform changes the practical question for LGPS investors. Local investing is no longer only a policy preference or reporting theme. Under the Pension Schemes Act 2026 and associated LGPS pooling and investment regulations, administering authorities must articulate a high-level local-investment objective, including a target range, within their investment strategy, while having regard to relevant local economic priorities and growth plans.

This does not mandate uneconomic investment. The government’s Fit for the Future response is clear that the purpose is not to direct capital but to ensure local investment continues and is strengthened under the new pooling framework. Authorities retain responsibility for strategy; Pools are expected to implement it, conduct due diligence and consider local opportunities.

That distinction matters. The opportunity is not “local at any cost”, but local investment that meets fiduciary standards: appropriate risk-adjusted return, diversification, liquidity, governance, operational robustness and evidence of local benefit.

The policy backdrop: “local” is broader than a single council boundary

The Pension Schemes Act 2026 provides an important clarification. For an LGPS scheme manager, “local investments” include investments in, or for the benefit of, people living or working in either the manager’s own area or the areas of other scheme managers in the same asset pool company.

In practice, “local” can be implemented at Pool-geography level: the combined footprint of the Partner Funds in a Pool. That is critical for SME finance. A narrowly ring-fenced, authority-by-authority approach may struggle to achieve scale, diversification and origination density. A Pool-geography approach supports the same policy intent while diversifying across counties, sectors, counterparties and supply chains.

The 2026 regulations reinforce this model. Asset pool companies must take reasonable steps to implement an authority’s strategy and, when implementing the local objective, consider local opportunities and projects. Authorities must also report progress against their local investment objective.

For Pools, local investing must therefore be investable, measurable and governable. It must move from narrative to mandate design.

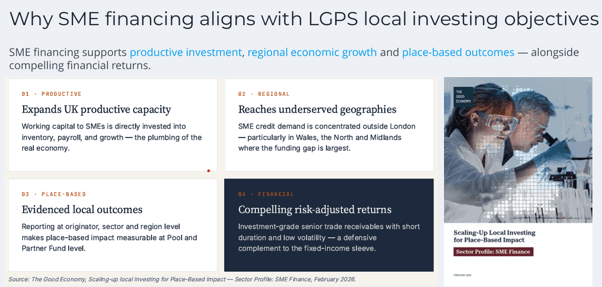

Why SMEs should sit at the centre of the local-investment discussion

SMEs are not a niche allocation theme. At the start of 2025, they accounted for 99.9% of UK private-sector businesses, 60% of private-sector employment and 51% of private-sector turnover.

For LGPS investors, this makes SME exposure directly relevant to place-based outcomes. SMEs employ local workforces, rent premises, purchase goods and services, pay taxes and anchor supply chains across sectors that matter to local authorities, from construction and logistics to healthcare, retail and the foundational economy.

The financing need is structural. British Business Bank research shows that challenger and specialist banks accounted for 60% of gross lending to smaller businesses in 2024, outperforming the UK’s big five banks for the fourth consecutive year. The research shows the proportion of smaller businesses using finance declined from 50% in Q3 2023 to 43% in Q2 2024, while credit cards and overdrafts remained common sources of working capital.

If banks are less able or willing to serve granular SME working-capital demand at scale, specialist origination, data-enabled underwriting and non-bank finance become essential delivery channels. The LGPS local-investment agenda gives that channel strategic relevance.

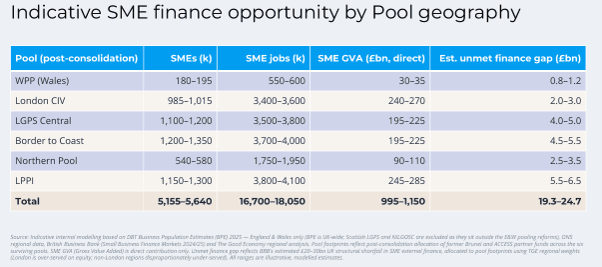

Fasanara’s research estimates that, across post-consolidation Pool-geographies in England and Wales, there are approximately 5 million SMEs, creating around 17 million jobs, generating roughly £1 trillion of direct SME GVA, with an estimated unmet finance gap of £20-£25 billion. The opportunity is distributed across every major Pool-geography, not concentrated in one region or sector.

Why working capital finance is a fiduciary route to SME exposure

Not all SME finance is suitable for institutional portfolios. Equity-like growth capital, unsecured SME loans and venture debt may carry risks that do not fit every LGPS allocation. Working capital finance secured against trade receivables is different.

In a receivables model, an SME has typically delivered goods or services and issued an invoice to a buyer. Financing advances cash against that receivable, helping the SME fund payroll, inventory, suppliers or growth while awaiting payment. The investor’s exposure is to a short-dated receivable, often owed by a larger corporate debtor, with a self-liquidating maturity commonly measured in 30 to 90 days.

This has several fiduciary merits for LGPS Pools.

First, it can provide real-economy exposure without long lockups. Short-duration receivables recycle capital quickly, allowing allocations to be adjusted over time and supporting liquidity management.

Second, it can be highly diversified. Rather than relying on a small number of bilateral corporate loans, a receivables portfolio can contain thousands of granular positions across buyers, suppliers, sectors, originators and regions.

Third, it can be measurable. Because invoices are tied to identifiable suppliers, buyers, sectors and regions, reporting can capture SMEs financed, deployment by Pool geography, sector allocation, capital recycled, and concentration by region or buyer.

Risks remain. Receivables finance requires controls around debtor credit quality, invoice verification, fraud, dilution, disputes, concentration, legal true sale, servicing continuity, insurance and recourse. The case is not simply that SMEs need capital, but that specialist, technology-enabled platforms can originate, underwrite, monitor and report diversified receivables in a fiduciary format.

Pool implementation: from local objective to investable mandate

The new LGPS framework creates a practical implementation challenge. Authorities must set a target range for local investments, while Pools must find institutional-quality strategies capable of absorbing Pool-level allocations and evidencing local benefit. Infrastructure, housing and regeneration remain important, but they are often episodic, lumpy, long-duration and project-specific. SME working capital finance offers a complementary route: granular, recurrent and capable of being mapped to a Pool’s geography.

A Pool can begin with a diversified UK SME receivables book, then use reinvestment and origination flows to tilt exposure toward the Pool footprint as eligible assets are sourced. This is more scalable than building a narrowly constrained county-level portfolio from day one and better reflects the statutory Pool-geography definition of local investment.

A well-designed mandate should define the eligible Pool-geography, the asset-level criteria for classifying an exposure as local, and the reporting basis for measuring progress. In SME receivables, this can include SME headquarters, trading location, employment footprint, originator channel, buyer location and sector classification.

Institutional Scale and Operational Infrastructure

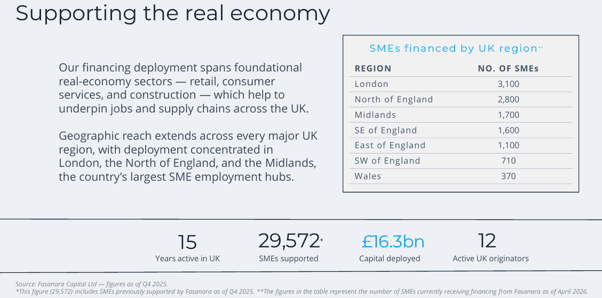

Fasanara operates within the fintech-originated asset-based finance market and has developed technology and origination relationships designed to support large-scale receivables programmes. As of 30 March 2026, the firm reported approximately $5.7 billion of assets under management, relationships with 141 fintech platforms and activity across more than 60 countries.

These characteristics illustrate the type of infrastructure that may be relevant when implementing institutional-scale SME receivables strategies, although approaches and capabilities vary across market participants.

The strategic case for LGPS investors

The LGPS local-investing agenda should not be limited to landmark projects. Housing, infrastructure, regeneration and clean energy are important pillars, but SMEs are the daily transmission mechanism of local economic growth. They employ people, pay wages, purchase stock, deliver services and keep supply chains functioning.

Working capital finance offers a practical way to connect LGPS capital with that real economy. It can sit within defensive private credit, productive finance, fixed-income or alternative credit allocations. Its short duration, self-liquidation, diversification, recurring deployment and measurable local footprint make it relevant for Pools implementing local objectives without compromising fiduciary discipline.

The policy direction is clear: the Pension Schemes Act 2026 broadens local investment to the Pool footprint; Fit for the Future requires objectives to be articulated, implemented and reported, and SMEs are central to the economic case. The missing link is a delivery model that converts policy intent into investable assets.

For LGPS Pools, SME working capital finance should therefore be considered not as a peripheral impact theme but as a scalable local-investment implementation tool. Done correctly, it can support regional growth, strengthen supply chains, provide transparent reporting and deliver a risk-return profile consistent with institutional private credit standards.

The question is not whether SMEs matter to local economies. They plainly do. The question is whether institutional investors can access SME exposure in a diversified, short-duration, reportable and fiduciary form. A Pool-geography receivables strategy is one potential approach.

Disclaimer

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell, or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investors or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with their financial professionals. The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Past performance does not predict or guarantee future results. Investing involves risk; principal loss is possible. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. Fasanara Capital Ltd, is authorised and regulated by the Financial Conduct Authority (“FCA”).

Important information on risk

Investing involves risk. The value of any investment and the income from such can go down as well as up, and you may not get back the full amount invested. Changes in the rate of exchange may also cause the value of overseas investments to go up or down. This information represents the views of Fasanara Capital Ltd and its investment specialists. It is not intended to be a forecast of future events and/or guarantee of any future result. Information was obtained from third party sources which we believe to be reliable but are not guaranteed as to their accuracy or completeness. There is no assurance that an investment will provide positive performance over any period of time. This information does not constitute investment research as defined under MiFID.