blog

Matching Adjustment, Private Credit & Solvency UK: Developments in Structured Credit

Sebastian Maciocia, Director of Capital Formation, UK

31 March 2026

Across the UK insurance investment landscape, one theme continues to shape portfolio construction: capital efficiency matters as much as yield.

While the growth of private credit has attracted significant attention in recent years, insurers approach the asset class through a distinct lens. Allocation decisions are rarely driven by a simple search for spread. Instead, they are shaped by the regulatory frameworks that govern capital treatment. At the centre of this dynamic sits the UK’s Matching Adjustment (MA) regime, now evolving under Solvency UK.

What has changed in the current environment is the pressure on insurers to find incremental returns in a world of compressed spreads. As traditional credit markets tighten, attention is increasingly turning towards structured exposures capable of delivering both predictable cash flows and capital-efficient treatment (though it should be noted that any such allocations remain subject to credit, liquidity and regulatory risks, and outcomes are not guaranteed).

A regulatory-driven private credit landscape

UK insurers do not allocate to private credit in isolation from regulation. Their investment frameworks are heavily influenced by the mechanics and benefits of the Matching Adjustment.

Under the MA regime, insurers can receive a capital benefit when they hold assets whose cash flows closely match the long-dated liabilities associated with insurance policies. In practice, this allows insurers to discount those liabilities at a rate that reflects the expected returns on matching assets rather than relying solely on risk-free curves.

To qualify for inclusion in MA portfolios, assets generally need to exhibit long-dated maturities, investment-grade credit characteristics, and fixed or highly predictable cash flows. Because the capital relief associated with the MA can be substantial, asset selection is often filtered through structures designed specifically to meet these criteria. As a result, insurers frequently access private credit through securitised exposures or structured formats, rather than through traditional direct lending strategies.

Solvency UK and the emergence of “Highly Predictable” assets

Recent reforms under Solvency UK have introduced an additional degree of flexibility through the creation of a “Highly Predictable” (HP) asset category within Matching Adjustment portfolios.

HP assets are those whose cash flows remain largely contractual but may include a limited degree of uncertainty. While these assets can now contribute to MA portfolios, the framework introduces clear safeguards. Their contribution is capped at a portion of the overall MA benefit, and insurers must apply an additional uplift to the Fundamental Spread (FS) to reflect the possibility of cash-flow variability. Governance requirements also remain rigorous, with the Prudent Person Principle continuing to guide investment decision-making.

For asset managers, the introduction of the HP category represents a carefully balanced form of regulatory innovation. The framework allows for a broader range of assets to be considered, but it places the burden of proof firmly on managers to demonstrate that cash flows are transparent, robust, and intended to be predictable, subject to market and credit risks.

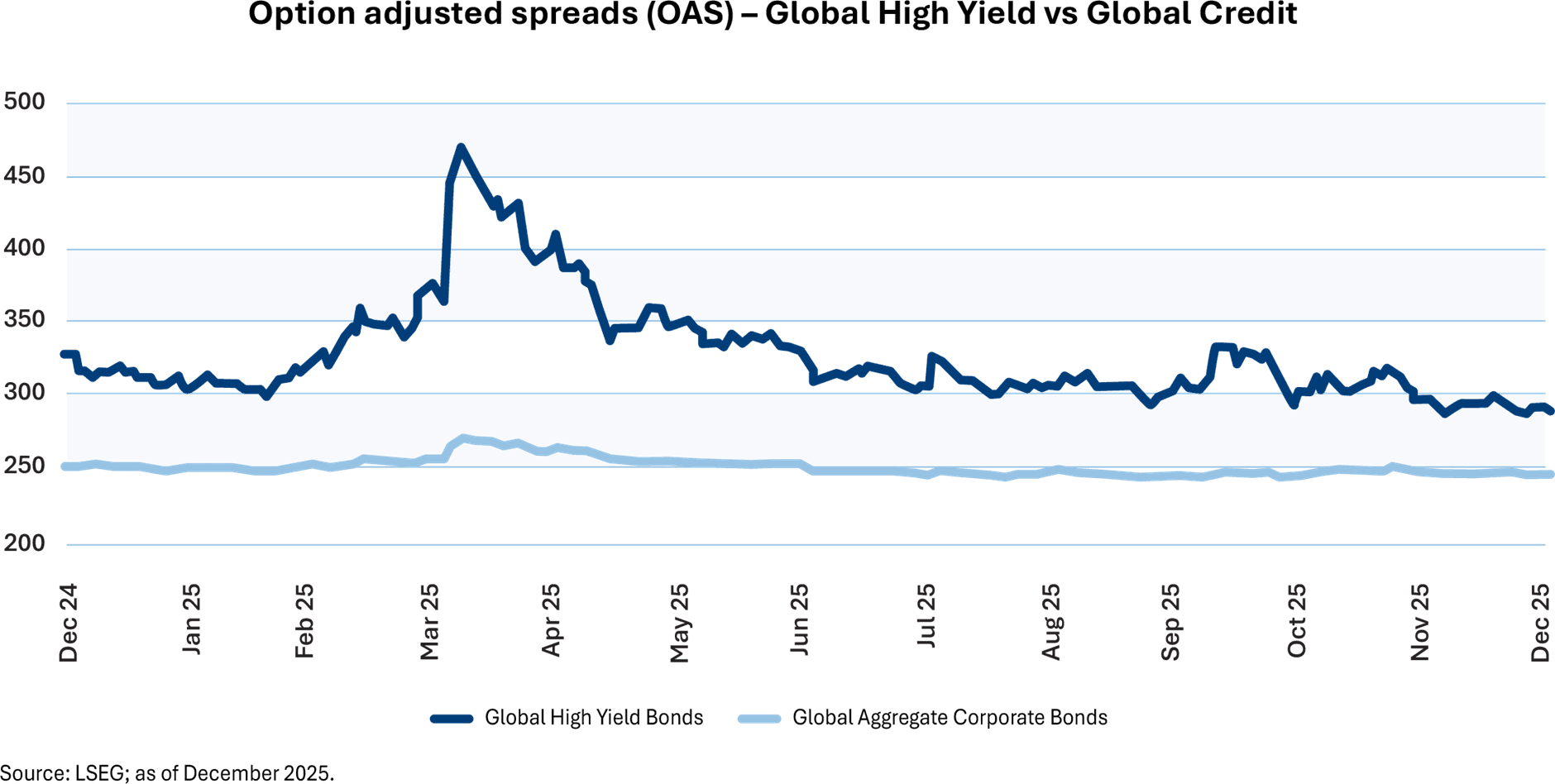

Spread compression and the private credit puzzle The broader market backdrop adds another layer to this dynamic. One of the most frequently discussed topics at industry conferences this year has been the extent to which credit spreads remain compressed across global markets.

For insurers, the implications are significant. With spreads tight, the incremental return available from simply moving down the credit spectrum is often limited. Yet the risk implications of doing so remain meaningful, particularly within highly regulated balance sheets.

This environment reinforces the importance of the Matching Adjustment itself. Rather than relying purely on yield, insurers can enhance portfolio economics through capital relief embedded in the regulatory framework. In effect, the MA regime allows capital efficiency to substitute for incremental credit risk as a source of return (though MA benefits are conditional and depend on eligibility, modelling assumptions, governance and market/liquidity conditions).

Structured credit regains attention

Against this backdrop, securitised credit and structured exposures are attracting renewed attention within insurance portfolios. Investment-grade tranches of securitisations are increasingly viewed as building blocks for MA portfolios, particularly where they provide clear and stable cash-flow profiles. Infrastructure securitisations represent one of the most mature examples of this trend, but interest is expanding into adjacent areas such as asset-based finance and diversified multi-asset structures.

In practice, insurers tend to focus on a consistent set of characteristics when evaluating structured credit opportunities. Cash flows must be transparent and easy to model, while structures themselves should remain relatively simple rather than highly engineered. There is also a preference for origination-led strategies, where asset managers control underwriting standards, rather than opportunistic purchases of secondary market exposures. Independent third-party ratings can also play an important role, particularly in specialised credit segments where investor familiarity may be lower.

The underlying narrative is subtle but important. Insurers are not seeking unconventional risk exposures. Instead, they are looking for capital-efficient structures capable of generating spread through disciplined structuring, while maintaining the predictability required for MA eligibility.

Solvency UK: a conditional green light

The Solvency UK reforms, finalised through PRA Policy Statement PS10/24, came into force on 30 June 2024. The reforms broaden the types of assets that can potentially qualify (subject to strict regulatory criteria) for Matching Adjustment treatment while reinforcing regulatory oversight.

In addition to introducing the Highly Predictable asset category, the regime places greater emphasis on governance and internal validation. Insurers must attest to the calibration of Fundamental Spread assumptions and demonstrate that their MA portfolios remain consistent with prudent risk management principles. The Prudential Regulation Authority (PRA) also retains the ability to review and modify MA permissions where necessary.

Taken together, these changes do not represent a relaxation of regulatory standards. Instead, they signal the regulator’s intention to allow asset innovation within a framework that prioritises transparency and predictability.

A structural opportunity

In conversations across the industry, many insurers emphasise that corporate balance sheets remain broadly resilient and that the credit environment has not yet experienced a full cycle since the global financial crisis.

Whether or not that assessment proves correct, the evolving regulatory framework suggests that the opportunity set emerging around structured credit is likely to be structural rather than cyclical. As insurers continue to optimise portfolios for capital efficiency, the ability to deliver predictable cash flows through well-designed structures becomes increasingly valuable.

For asset managers operating in this space. The opportunity focus is not simply on offering credit exposures, but on building transparent, disciplined and regulatorily compatible structures designed to support insurers’ long-term liability-matching needs.

Disclaimer

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell, or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investors or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with their financial professionals. The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Past performance does not predict or guarantee future results. Investing involves risk; principal loss is possible. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. Fasanara Capital Ltd, is authorised and regulated by the Financial Conduct Authority (“FCA”).

Important information on risk

Investing involves risk. The value of any investment and the income from such can go down as well as up, and you may not get back the full amount invested. Past performance is not a guarantee of future returns. Changes in the rate of exchange may also cause the value of overseas investments to go up or down. This information represents the views of Fasanara Capital Ltd and its investment specialists. It is not intended to be a forecast of future events and/or guarantee of any future result. Information was obtained from third party sources which we believe to be reliable but are not guaranteed as to their accuracy or completeness. There is no assurance that an investment will provide positive performance over any period of time. This information does not constitute investment research as defined under MiFID.