blog

Private Credit for Private Wealth Portfolios

Francesco Filia, Founder and CEO, Fasanara Capital

24 November 2025

For decades, Italian private banking portfolios were built on a simple foundation: government bonds that offered safety, yield, and predictability—the pillars of post-war wealth management. That foundation, however, is evolving. As Europe transitions into a new equilibrium after years of volatility, the macroeconomic backdrop—and with it, investors’ priorities—is shifting.

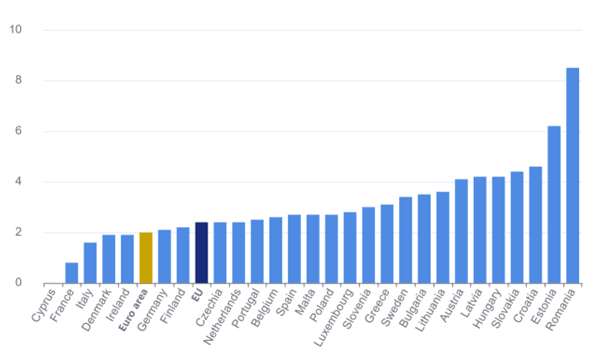

In Italy, inflation has moderated to around 1.6% as of August 2025 (Figure 1). Falling import prices, moderate wage growth, and a firmer euro have restored price stability. Energy, once inflationary, is now broadly disinflationary. In Spain, the picture is more complex: headline HICP is expected to remain around 2.3%, while core inflation recently rose to 2.7%—its highest level in ten months. A tight labour market and rising housing costs have made Spain one of the Eurozone’s more inflationary economies.

This divergence is increasingly shaping portfolio design across Southern Europe. With inflation normalising in Italy but lingering in Spain, investors are refocusing on real yield, diversification, and liquidity—priorities that extend beyond traditional fixed income.

Figure 1: Annual inflation rates (%) across Europe in August 2025

Source: eurostat

From bonds to broader diversification

Italian private banking portfolios still reflect their heritage: large allocations to sovereign and bank bonds, complemented by equities and cash. Yet as yields fluctuate and spreads narrow, investors are broadening their horizons. Typical allocations now combine:

- Fixed income: shorter duration, stronger credit focus

- Equities: more global and thematic, from AI to semiconductors and defence

- Private markets: including private equity, private debt, and infrastructure

- Cash: retained for flexibility, but less central to long-term returns

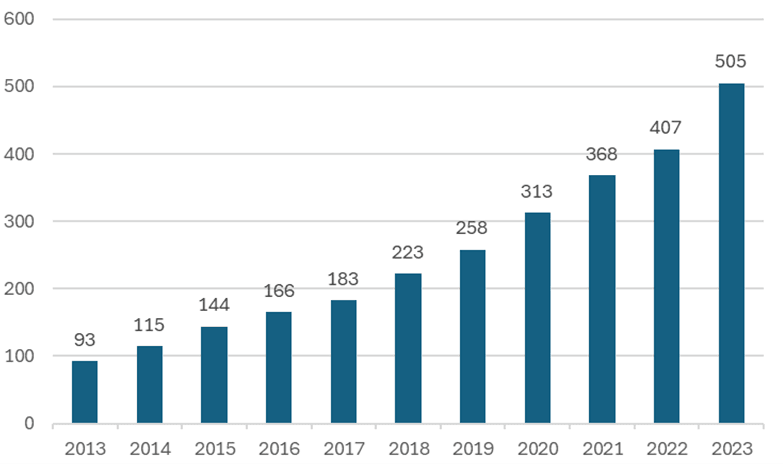

Across both Italy and Spain, one trend stands out—rising interest in private credit (Figure 2), particularly strategies offering real-economy exposure with short durations and limited lock-ups.

Figure 2: European private credit AuM, 2013-2023 (US$ billion)

Source: Preqin

Our approach: real cashflows, not market noise

Founded in 2011, Fasanara Capital manages over $5.5 billion in fintech lending and alternative credit strategies. Its main investment strategy, asset-based financing (ABF), focuses on short-term, secured lending backed by verified invoices and trade receivables from small and mid-sized enterprises (SMEs).

Through a proprietary platform integrating over 140 fintech originators across 60 countries, Fasanara provides financing to SMEs. Each underlying asset typically matures in 30–90 days, allowing for continuous reinvestment and low duration risk.1

Understanding private credit’s resilience

Private credit’s defining feature is its cashflow-based valuation. Unlike private equity—where returns depend on multiple expansion or exit markets—private credit derives value from contractual repayments. Fasanara’s portfolios hold short-term receivables backed by large corporate obligors, with a focus on repayment performance. This approach can help mitigate key risks by:

- Aiming to moderate mark-to-market volatility; though valuations can still fluctuate

- Lower sensitivity to public-market valuation multiples; macro conditions can still affect borrower performance and collateral values

- Reduced dependence on external refinancing/IPO markets

- Regular amortisation as receivables repay and proceeds are typically recycled; timing and liquidity are not assured

In private credit, returns compound through repayment rather than re-rating—a feature that underpins resilience during periods of market stress. For private wealth investors, this could potentially make private credit a natural counterweight to private equity: less cyclical, less correlated, and more predictable.

Integrating private credit alongside real estate, bonds, and equities

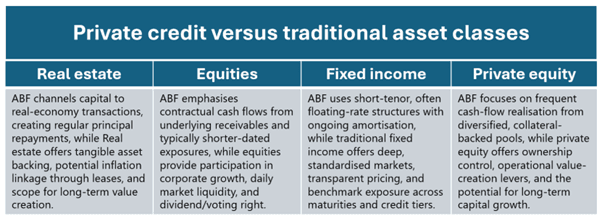

When viewed alongside traditional portfolio pillars, private credit serves a distinct function—complementing real estate, equities, and fixed income rather than competing with them (Figure 3).

Figure 3: Private credit characteristics relative to major asset classes

Source: Fasanara Capital

As portfolios evolve beyond the traditional triad of equities, bonds, and real assets, private credit is increasingly seen as a fourth pillar—grounded in contractual cashflows rather than market valuations.

Technology: turning diversification into discipline

Fasanara uses proprietary data infrastructure to inform its credit allocation and portfolio management processes. The firm’s platform processes around 1.5 terabytes of data daily, integrating live feeds from fintech partners to monitor over 600,000 receivables in real time. Machine learning models underpin the Fasanara Debtor Rating (FDR), recalibrating risk profiles using more than 150 variables per loan.

This aims to enable dynamic pricing, early risk detection, and granular diversification across geographies and sectors. In effect, this technology is intended to transform a once-manual segment of credit into an institutional-grade asset class—transparent, scalable, and continuously optimised.

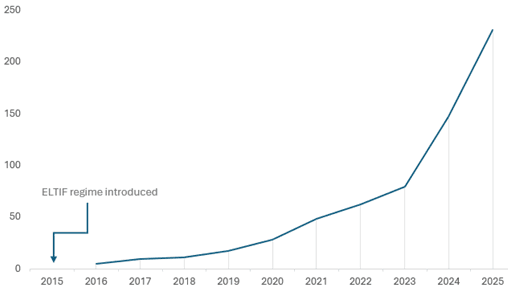

ELTIF: the bridge to private credit democratisation

The introduction of ELTIF marked a key milestone for Europe’s private-markets landscape. The revised framework streamlines eligibility rules, broadens investor access, and increases flexibility in portfolio composition. Under this regime, private-credit strategies—including short-duration, asset-backed lending vehicles—can be offered through regulated structures for qualified investors.

Since implementation, the number of authorised ELTIFs has risen sharply. According to ESMA data, active vehicles have grown from just five in 2016 to more than 230 in 2025 (Figure 4), with the steepest increase following the reform in January 2024—fund numbers nearly doubling between 2023 and 2024.

Figure 4: Number of ELTIFs launched

Source: European Securities and Markets Authority. Data correct as of 31 October 2025.

This acceleration reflects growing demand for long-term private-market exposure and the accessibility introduced under ELTIF. For private banks and wealth managers, it represents a structural broadening of opportunity.

Real impact, measurable scale

As of September 2025, Fasanara’s platform has financed over $115 billion in cumulative volumes and supported more than 100,000 SMEs globally—the manufacturers, exporters, and logistics operators that underpin employment and growth across Europe.

Fasanara’s strategies aim to deploy private capital where banks have retrenched, financing businesses that drive real-economy resilience.

The future of fixed income is private, short-term, and real2

With inflation patterns diverging across Southern Europe, investors are refocusing on stability, liquidity, and diversification within income-generating portfolios. Asset-based finance is emerging as a complementary component within modern fixed-income allocations— offering exposure to real-economy repayments.

For private banks and family offices, this marks an important evolution in portfolio design. In an environment of shifting inflation dynamics, true diversification increasingly depends on assets grounded in measurable cashflows rather than market cycles.

1Maturity profiles and cash flows can vary; reinvestment and duration outcomes are not assured.

2The views expressed are of Fasanara Capital Ltd.

About Fasanara Capital

Fasanara Capital is an independent London-based asset manager and fintech platform specialising in alternative credit and quantitative strategies. Founded in 2011, the firm manages over $5.5 billion on behalf of institutional and professional investors globally.

Through its proprietary fintech lending infrastructure, Fasanara provides exposure to short-duration, asset-backed private credit, financing small and mid-sized enterprises (SMEs) across more than 60 countries. Its Asset-Based Finance (ABF) platform integrates more than 140 originators and processes over 1.5 terabytes of data daily, enabling data-driven credit allocation.

Fasanara Capital’s broader investment capabilities span digital lending, trade receivables, structured credit, and quantitative market-neutral strategies. The firm’s approach combines technology, risk discipline, and real-economy connectivity to deliver scalable, transparent, and diversified sources of return.

Headquartered in London with offices in Milan, Amsterdam, and Abu Dhabi, Fasanara Capital is authorised and regulated by the UK Financial Conduct Authority (FCA).

Disclaimer

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell, or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investors or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with their financial professionals. The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Past performance does not predict or guarantee future results. Investing involves risk; principal loss is possible. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. Fasanara Capital Ltd, is authorised and regulated by the Financial Conduct Authority (“FCA”).

Important information on risk

Investing involves risk. The value of any investment and the income from such can go down as well as up, and you may not get back the full amount invested. Past performance is not a guarantee of future returns. Changes in the rate of exchange may also cause the value of overseas investments to go up or down. This information represents the views of Fasanara Capital Ltd and its investment specialists. It is not intended to be a forecast of future events and/or guarantee of any future result. Information was obtained from third party sources which we believe to be reliable but are not guaranteed as to their accuracy or completeness. There is no assurance that an investment will provide positive performance over any period of time. This information does not constitute investment research as defined under MiFID.