blog

The Rise of Asset-Backed Digital Rails

David Vatchev

16 December 2025

Yield Hunting in an Unstable Climate

The classic 60/40 portfolio has faced challenges under recent market conditions. In today's high-rate, volatile macroeconomic environment, equities and bonds have moved in lockstep, gutting the traditional benefit of diversification [1]. As a result, investors are currently exploring different types of income streams.

This pivot is confirmed: industry surveys show over 70% of fund managers expect to increase allocations to alternative assets like private debt [2]. This demand is accelerating the convergence of traditional finance with the digital asset ecosystem.

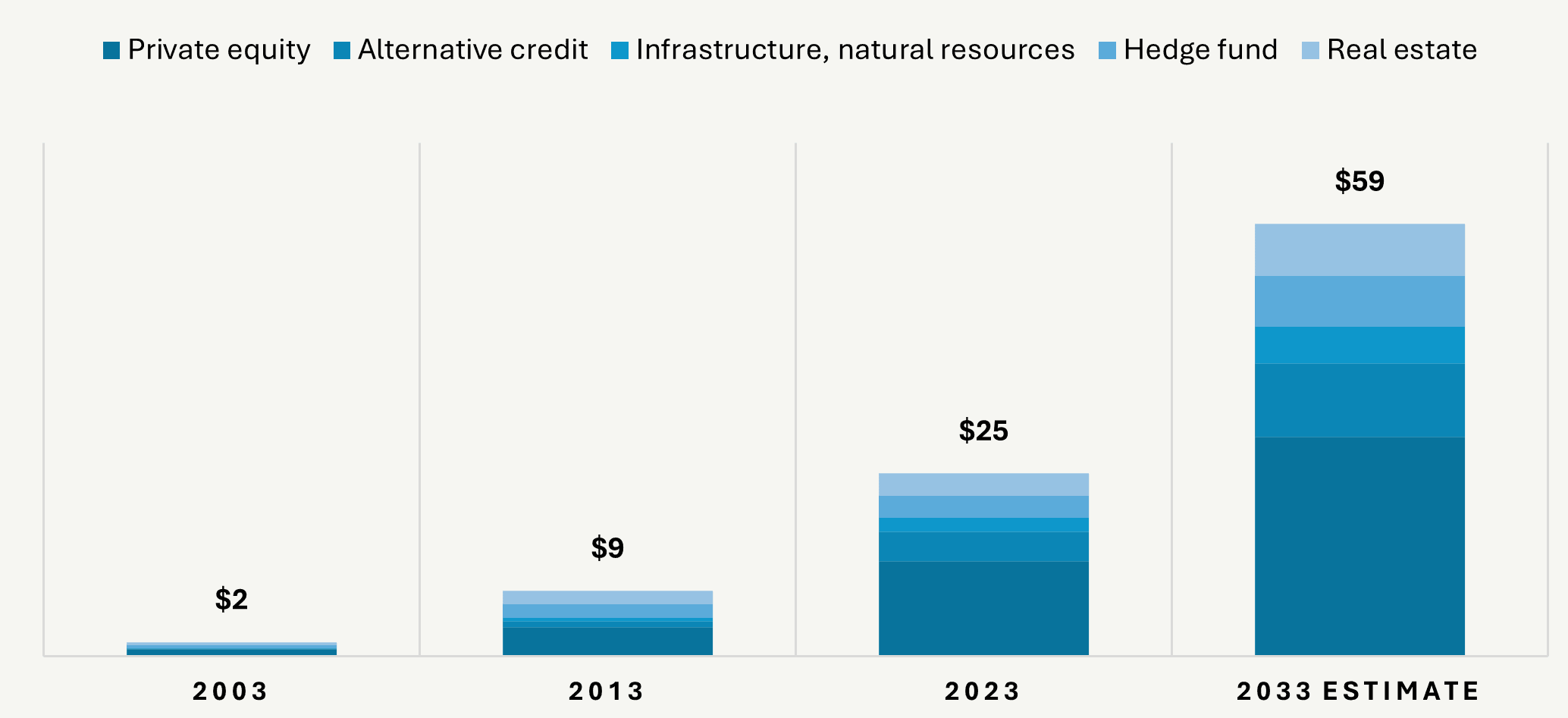

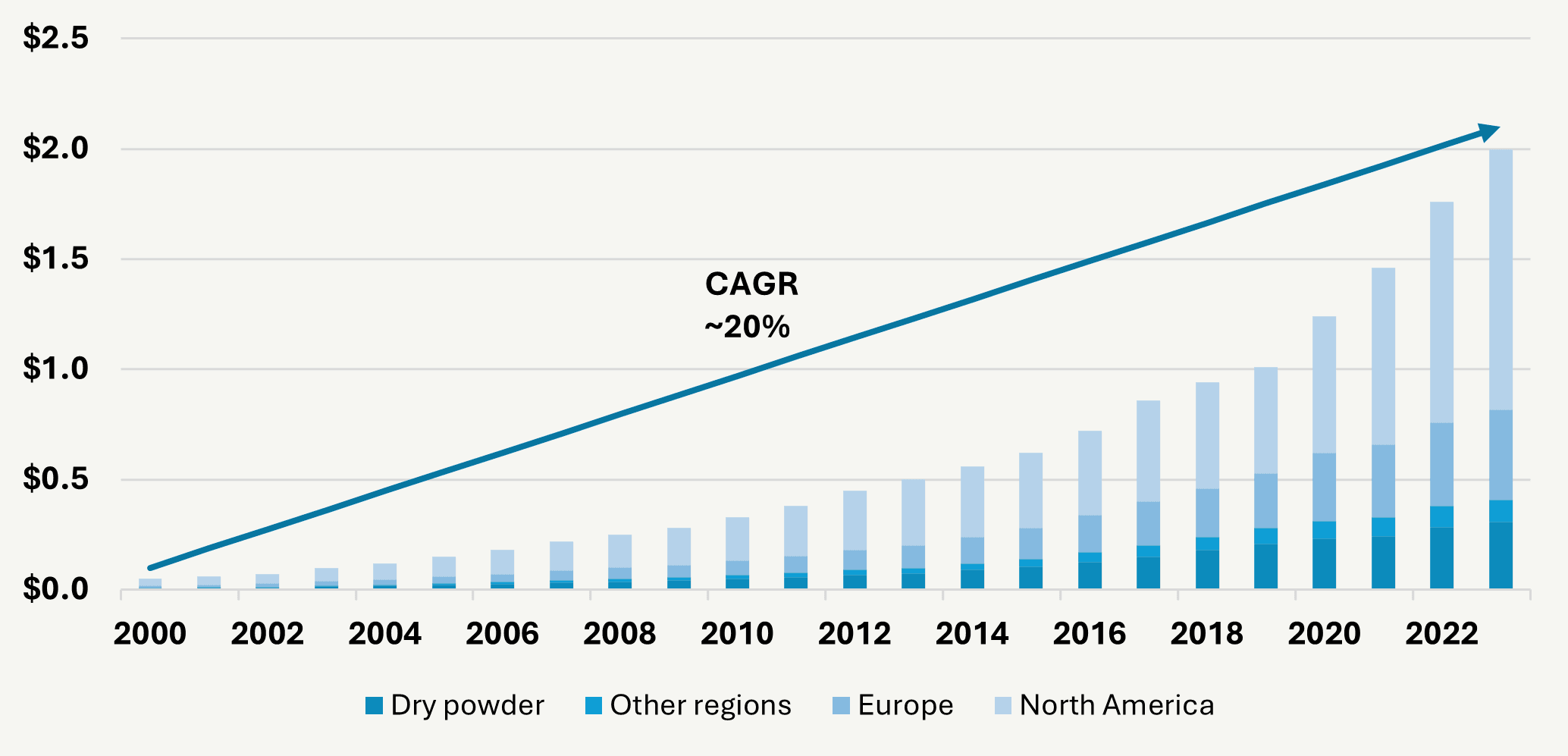

Figure 1: Global alternative assets under management (US$ trillions)

Source: Bain and Company, August 2024

The Digital Solution: Stablecoin Yield Goes Institutional

Digital assets, particularly stablecoins, are no longer a niche technology; they are a critical global liquidity rail. Data from Visa's on-chain analytics show stablecoin transaction volumes have surged, facilitating over $52 trillion in total volume over the last 12 months [3]. This shift is foundational, driven by the belief that more and more retail users will turn to wallets instead of traditional bank accounts.

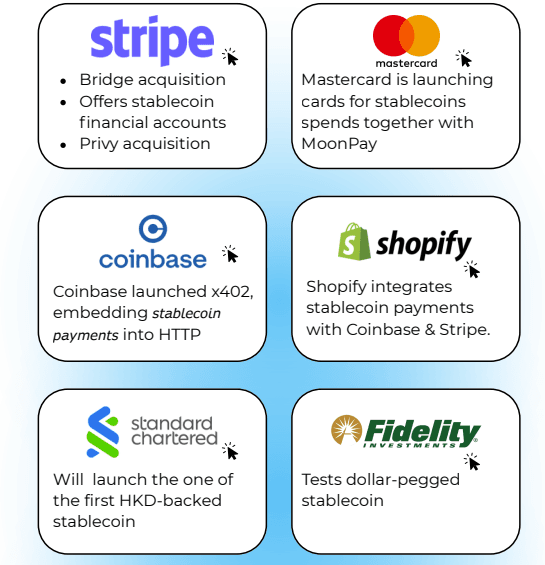

Mainstream finance is moving to capture this market. High-profile acquisitions signal that digital payments are the strategic path forward for satisfying the universal hunger for yield and efficiency:

Source: Money Movement 2.0| fiftyone.xyz How Stablecoins Are Rebuilding Global Finance and Commerce

This institutionalisation was dramatically signalled by Aave Labs' acquisition of Stable Finance [4]. Stable was a fintech firm that simplified stablecoin savings, allowing users to deposit cash or crypto and earn interest via automated on-chain strategies. The strategic rationale: fold consumer-friendly UI and technology into permissionless Decentralised Finance (DeFi) rails.

Source: Nagarro.com

This move suggests a potential future for digital assets beyond speculation, with an emphasis on real-economy applications, converging DeFi and mainstream consumer savings tools.. The pursuit of yield is the driver, confirming the lesson learned from the 2022 crypto yield platform collapses [5], where investors demanded transparent, non-speculative digital income. The core challenge is differentiating the source of that yield:

- Endogenous (Internal): Generated within the crypto ecosystem itself (e.g., staking, liquidity provisions, native token rewards etc) and highly correlated with the overall crypto market and its inherent volatility.

- Exogenous (External): Generated outside the crypto ecosystem, derived from real-world assets (RWA) like SME loans, mortgages, or invoices. This source aims to provide uncorrelated, stable cash flows, decoupling the yield from on-chain liquidity risk; However, they may involve other forms of risk, including operational, credit, or other liquidity factors.

Most of DeFi is endogenous and circular, meaning returns are often correlated and unstable. A crucial distinction is emerging between volatile, crypto-native yields and potentially more stable yields generated by real-world credit.

While high-profile apps enable easy access to general DeFi yield, increasingly investors are focusing on sourcing exogenous yield from granular RWA portfolios, such as SME receivables and consumer loans, which can offer additional diversification benefits. RWAs represent a massive amount of latent exogenous capital (commodities, private credit, FX, etc.) and present the greatest opportunity to expand DeFi beyond its circular state. This difference in yield source can help provide more predictable and uncorrelated returns compared to some other strategies*:

Source: Pantera Capital

*No yields are guaranteed and capital remains subject to risk.

From Bank Retreat to Fintech Rise: The New Lending Disintermediation

Even before digital assets, a quiet revolution in credit was underway. Post-2008, stricter capital rules (like Basel III/IV) forced traditional banks to scale back lending, creating a massive financing void, especially for mid-sized companies and niche sectors. This retreat created a structural gap swiftly filled by private lenders.

In the U.S., non-bank lenders have grown from just 20% of the mortgage market in 1990 to over 65% today [6]. Globally, non-bank financial institutions now account for nearly 50% of all financial assets [7]. This disintermediation fuelled an explosive boom in private credit.

Figure 5: Private credit providers’ AUM (US$ trillions)

Source: Accenture

Now, investors are looking beyond concentrated corporate loans toward Asset-Based Finance (ABF), which is secured by pools of financial and real-world assets (like invoices or consumer loans) rather than a single company's promise to pay.

- Structural Insulation: ABF provides insulation from corporate risk. Repayment depends on the predictable cash flow from the assets themselves.

- Scale: This ABF market is enormous (estimated up to $40 trillion globally [8]), but historically inefficient.

- Fintech Supercharge: Fintech platforms, backed by AI and big data, can now originate and service millions of small, diversified loans globally in a seamless, automated fashion**.

**Note: Cash flows and valuations depend on borrower performance, servicing and legal enforceability; market size estimates vary; technology-enabled origination/servicing can introduce operational, data, cyber and model risks. Liquidity and outcomes are not guaranteed; capital is at risk.

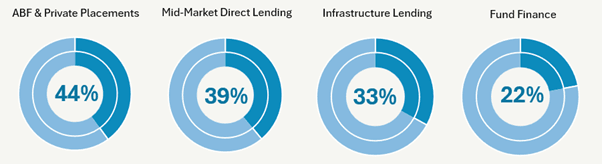

Portfolios built around contractual, asset-backed cash flows and high granularity aim to limit exposure to single-name risk [9]. This explains why this strategy is gaining institutional interest: A Moody's survey [10] found that 44% of insurers surveyed plan to increase their holdings in private credit over the long term, with particular interest in ABF and private placements.

Figure 6: Outlook and appetite of top 30 insurers to increase private credit allocations

Source: Macfarlanes, Moodys Ratings, PitchBook

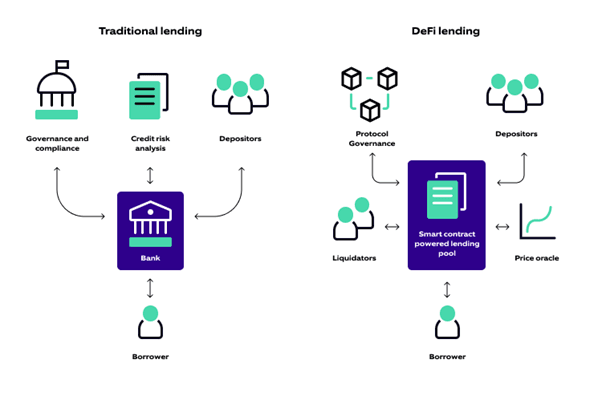

Real-Economy Credit on Chain

Lending is shifting from the opaque balance sheets of banks to the transparent, tech-enabled domain of non-bank platforms. Fintech platforms rewired the pipes of credit. The next revolution, tokenisation, is supercharging those pipes.

It introduces 24/7 liquidity, transparency, and "composability" (the ability to program assets) to the once-illiquid world of private credit. Tokenisation converts shares in a credit fund into digital tokens on a blockchain, which can increase liquidity and aims to enhance yield. Potential benefits for investors can include:

- Liquidity: Investors can use their tokens as collateral to borrow stablecoins instantly, which creates a "repo-like" function for private assets [11].

- Yield: Tokenisation can offer differentiated yield opportunities through DeFi composability [12].

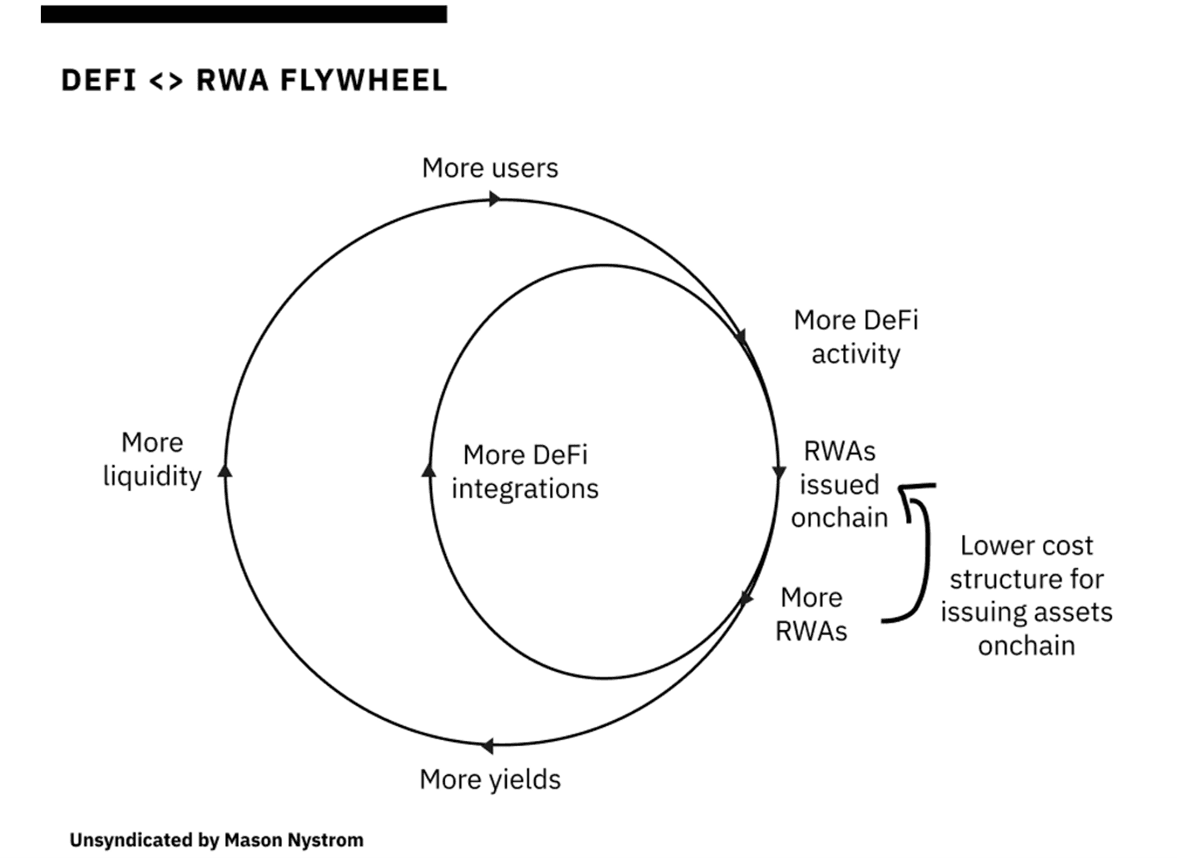

This points to a "digitisation of financial rails," where blockchain systems augment legacy infrastructure. We are seeing the early stages of this, as more traditional assets (from real estate to receivables) move on-chain, creating a flywheel effect [13]. The result is a future where "traditional yield" and "digital yield" converge, most notable in the recent growth of yield-bearing stablecoins:

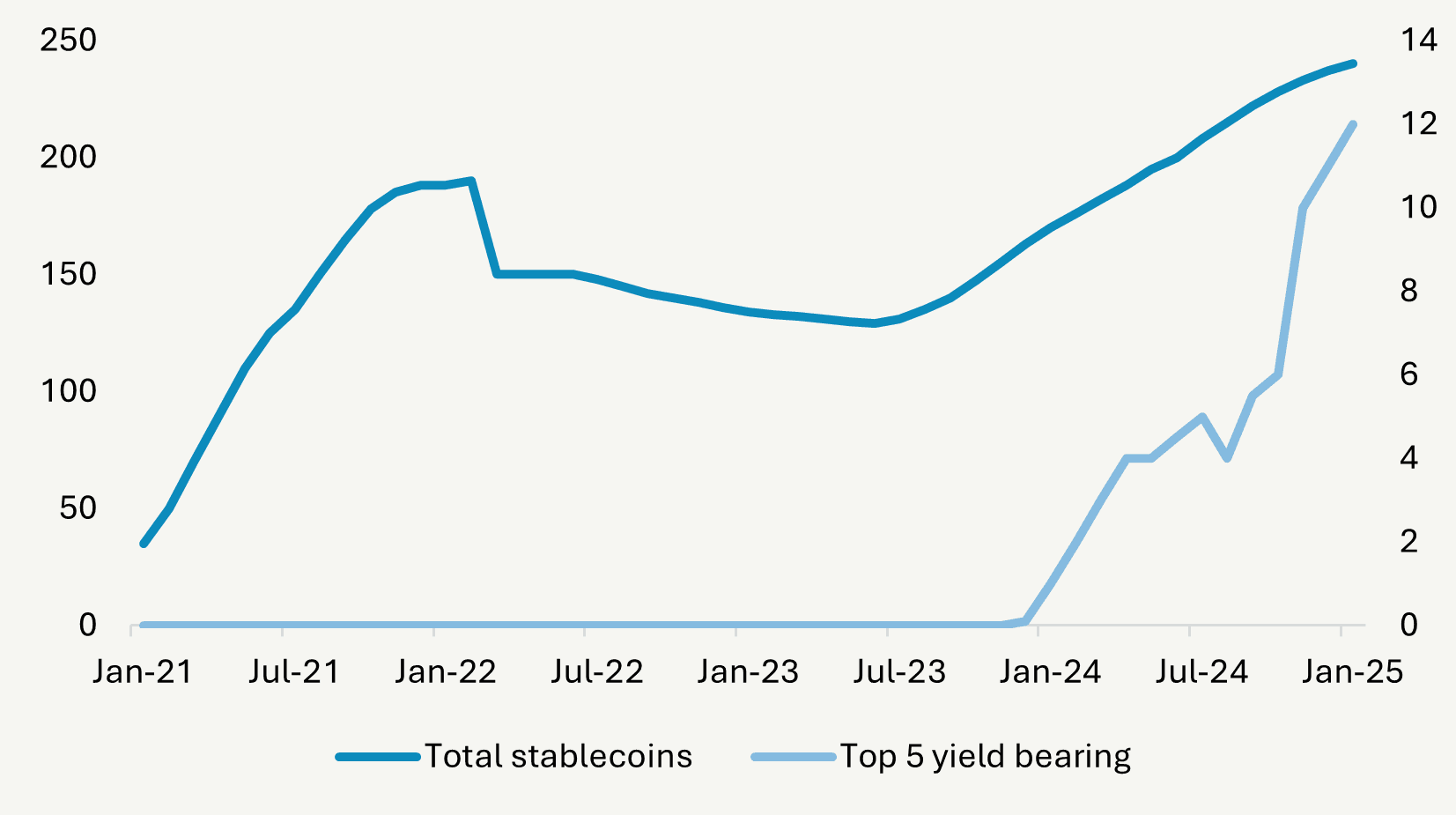

Figure 7: Overall stablecoins market cap & the five biggest yield-bearing stablecoins

Source: The Block, March 2025

A New Paradigm for Yield

The intersection of digital assets and lending is giving rise to a new paradigm for yield that marries the stability of real-world cash flows with the dynamism of blockchain technology. This convergence offers the combination of TradFi rigor and DeFi agility. In practical terms, investors can deploy capital into real, productive assets like loans and receivables, while still enjoying improved liquidity, transparency, and customisable strategies. Assets that were once static and illiquid become dynamically manageable.

The convergence of these trends points to a new paradigm for yield in the digital age: FinTech innovations are removing frictions for everyday investors to earn interest on digital assets, while asset managers are bringing proven credit strategies on-chain.

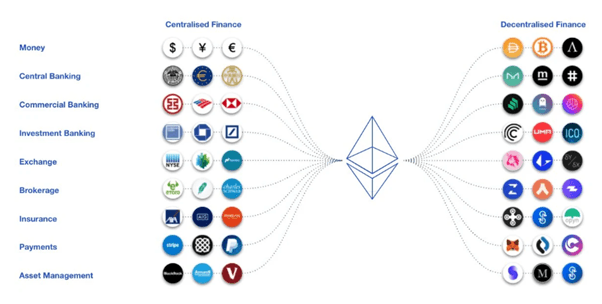

Increasingly DeFi is extending TradFi capacities due to its transparent, 24/7, programmable nature:

Forward-thinking firms can act as bridges between traditional credit and digital finance. This direct-to-investor model not only aims to enhance yield, but also broadens access to opportunities that were once the preserve of large institutions. Today, digital platforms are opening the door for investors to engage with real-economy credit strategies, such as European SME loans or U.S. trade receivables, while recognizing that, like all investments, these carry risks and no guarantees. Still, the ability to allocate capital through regulated, tech-enabled channels offers the potential for more efficient capital flow into the real economy and the potential of generating stable, diversified income in return. Importantly, this shift reflects a broader solution: away from chasing yield in speculative arenas or correlated portfolios, investors are now able to access digitally enabled, asset-backed finance as a reliable alternative.

Conclusion: Yield is Being Rewired

Investors are no longer restricted to the yields banks or bond markets offer. They can also participate in funding the real economy through digital platforms. We are witnessing the creation of a digital yield ecosystem where everyday savers and institutional investors alike can find refuge from correlated markets.

Credit is becoming more distributed, sourced from diverse lenders, wrapped in digital wrappers, accessible globally, and enhancing systemic stability. Investors who explore these novel credit pathways can potentially unlock new sources of uncorrelated diversified income***.

***Capital is at risk and capital gains are not guaranteed.

Disclaimer

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell, or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investors or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with their financial professionals. The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Past performance does not predict or guarantee future results. Investing involves risk; principal loss is possible. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. Fasanara Capital Ltd, is authorised and regulated by the Financial Conduct Authority (“FCA”).

Important information on risk

Investing involves risk. The value of any investment and the income from such can go down as well as up, and you may not get back the full amount invested. Past performance is not a guarantee of future returns. Changes in the rate of exchange may also cause the value of overseas investments to go up or down. This information represents the views of Fasanara Capital Ltd and its investment specialists. It is not intended to be a forecast of future events and/or guarantee of any future result. Information was obtained from third party sources which we believe to be reliable but are not guaranteed as to their accuracy or completeness. There is no assurance that an investment will provide positive performance over any period of time. This information does not constitute investment research as defined under MiFID.

Sources:

[1] Russell Investments (2023). "Is The 60/40 Balanced Portfolio broken? Not Forever."

[2] Carne Group (2024). "Research reveals alternative asset classes are set to see the biggest increase in fund raising in 2024."

[3] Visa (2024). "Visa Onchain Analytics Dashboard."

[4] Coindesk (2024). "Aave Labs Acquires DeFi App Stable in Push for Mainstream Adoption."

[5] Caleb & Brown (2022). "Zero Degrees Celsius: A Deep Dive into the Celsius Liquidity Crisis”

[6] Federal Reserve (2025). "The Role of Nonbank Lenders in Monetary Policy."

[7] International Monetary Fund (IMF) (2024). "Global Financial Stability Report, April 2024."

[8] Fasanara Capital (2025). "The Growth of Private Credit and Fasanara's Asset-Based Finance Advantage”

[9] PIMCO (2025). “Asset-Based Finance: Quantifying Diversification Benefits and Return Potential”

[10] Macfarlanes (2024). "The growth of asset-based finance in private credit markets."

[11] Boston Consulting Group (2024). "Tokenized Funds: The Third Revolution in Asset Management Decoded"

[12] Messari (2024). "The Rise of Real-World Assets (RWA) in DeFi."

[13] Pantera Capital (2025). "The Great On-Chain Migration."