blog

The Return of Zero:

Why Negative Rates Are Coming Back

The post-pandemic rate cycle has one more act. It ends where the last one did - below zero. The question is not whether, but when, and how fast we get there.

Francesco Filia, Founder and CEO

29 April 2026

There is a passage in Gibbon's Decline and Fall where he observes that the Romans, even as the legions pulled back from the Rhine, found reasons to believe the frontier was not really contracting. Each retreat was tactical, each concession local. The empire was not ending; it was adapting. Something similar is happening in fixed income markets today. Central banks have spent two years congratulating themselves on the inflation fight - and they have, on that narrow metric, largely won. But the broader monetary order they are returning to is not the stable normal of the pre-2008 textbooks. It is the low-growth, debt-saturated, technology-deflationary world they escaped briefly between 2021 and 2023. And in that world, rates do not stay at 4 or 5 percent. They slide back toward zero, and then past it.

Let us be precise about what we mean. The Pavlovian reflex to today's supply shocks - oil above $75, gasoline costs filtering into every CPI category, geopolitical premia baked into commodity curves - will keep rates marginally elevated through the near term. Markets will talk themselves into a "higher for longer" consensus one more time. Some will be right, briefly. But these are surface disturbances. The underlying sea is moving in the opposite direction, pushed by forces that are structural, chronic, and in several respects entirely unprecedented.

I. The Deflation Engine Nobody Wants to Name

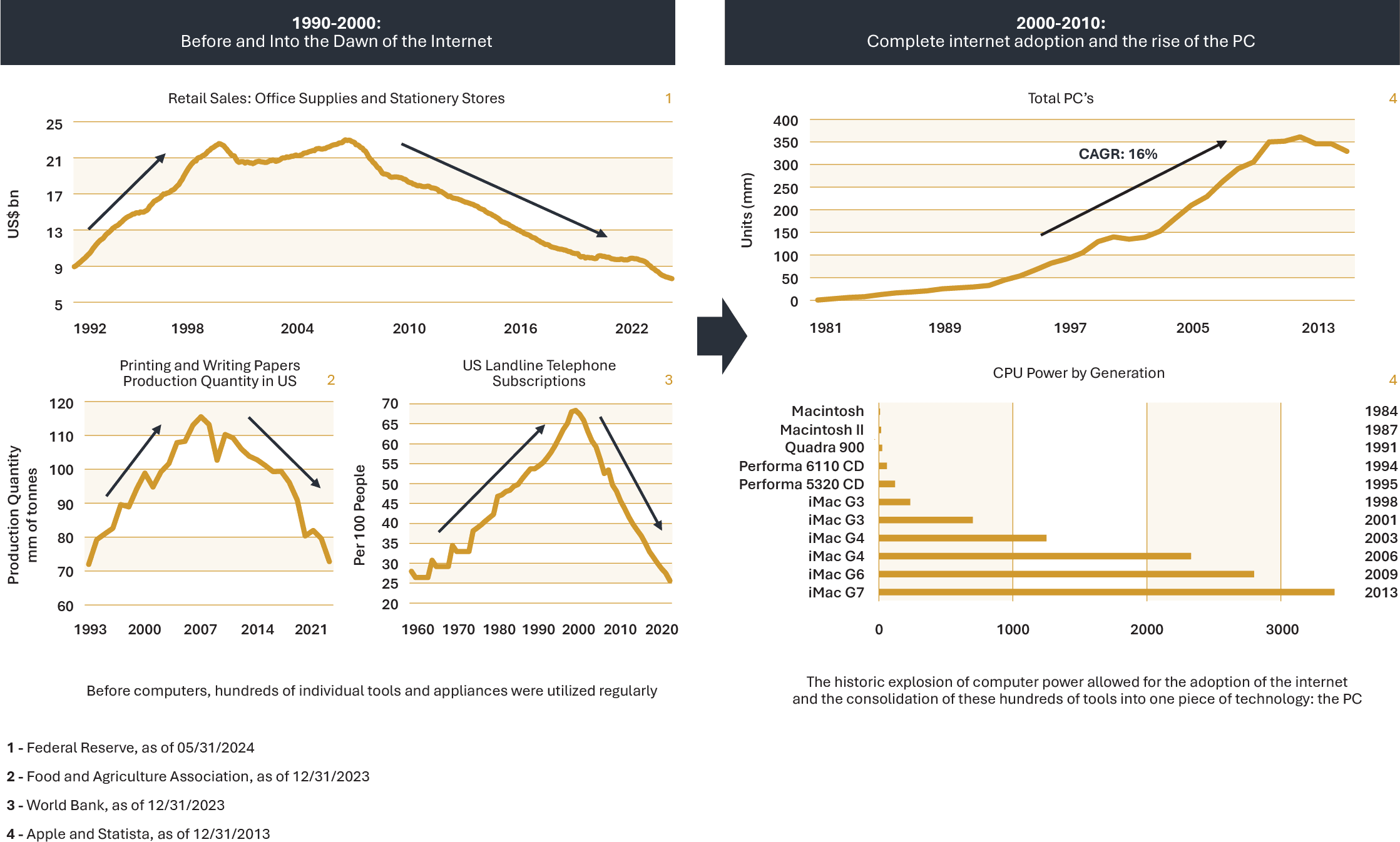

Historians of technology will note that every general-purpose technology of sufficient power eventually colonises the price level. Steam collapsed the cost of manufactured goods in the 1820s and 1830s, producing exactly the kind of paradox we see today: rising productivity, concentrated profits, widespread disruption, and falling prices for the things that matter to ordinary households. Electricity repeated the pattern after 1900. The internet did it again, slowly at first and then gaining momentum and impacting everything from music to taxis to hotel rooms.

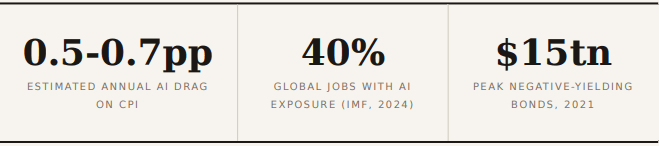

Artificial intelligence is the next iteration. But there is a crucial difference in degree. Previous technologies replaced muscle or routine process. AI replaces cognition across the full cost curve - in white-collar services, in legal work, in software development, in financial analysis, in customer service. Everything costs less and is available in significant quantities. This is not a cyclical phenomenon. It is not something the Federal Reserve can calibrate against. It is what economists call a supply shock of indefinite duration, and its net effect on prices is disinflationary – bordering on deflationary.

Note: Fasanara estimate, based on assumed AI productivity pass-through to prices; as of April 2026.

The Federal Reserve Bank of St. Louis published analysis in 2025 showing that occupations with the highest AI adoption recorded the steepest unemployment increases between 2022 and 2025. Computer and mathematical roles – the most AI-exposed categories – saw some of the largest job losses1. This is not creative destruction at the usual pace. Workers displaced by AI do not immediately find equivalent-wage substitutes and, as a result, they often spend less. And when a significant share of a consumer economy spends less, the monetary logic of higher rates begins to collapse.

II. The Secular Stagnation Trap, Revisited

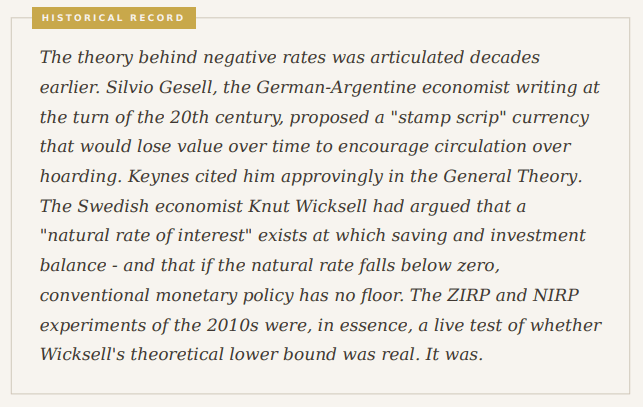

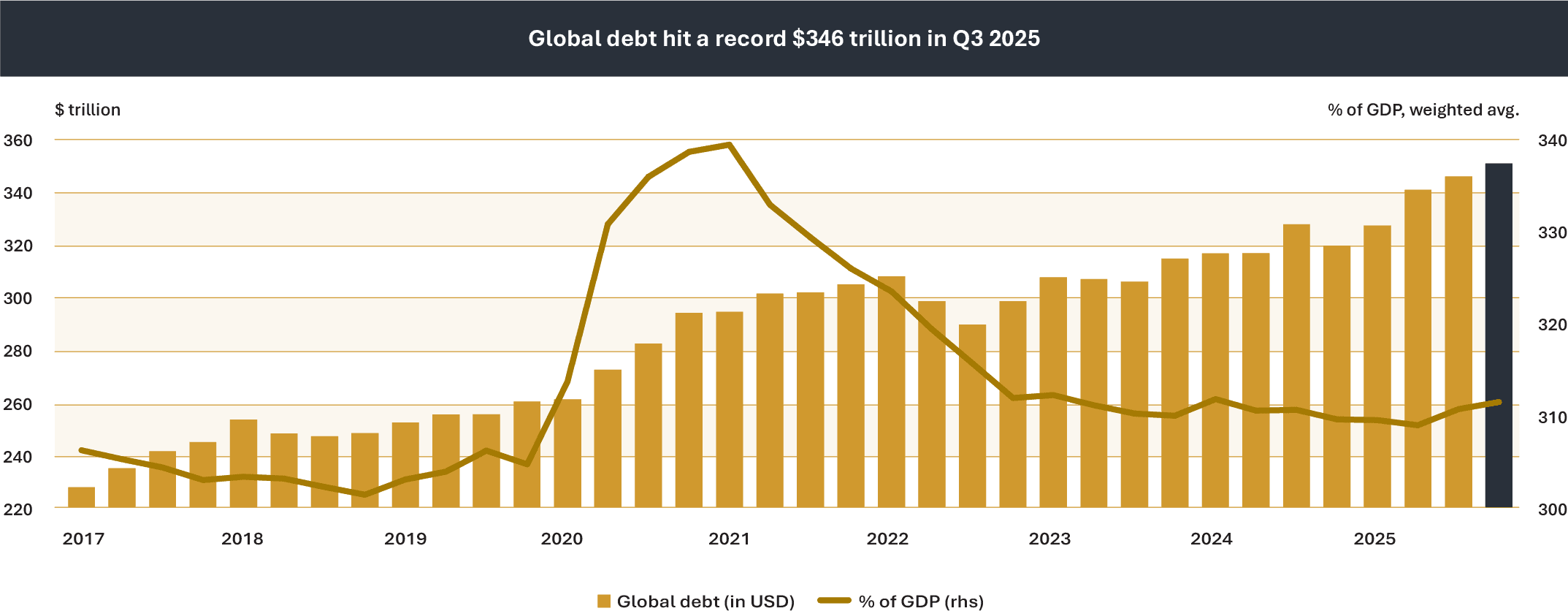

It is easy to forget, given the inflation episode of 2021-23, that the dominant macroeconomic problem of the previous fifteen years was the opposite one. From 2009 to 2021, the world's major central banks spent their credibility and their balance sheets trying to generate inflation. The ECB cut its deposit rate below zero in June 2014 for the first time in its history. Denmark had gone negative two years prior, and Japan’s central bank followed in January 2016. By the peak of the negative-rate experiment in 2021, something in the order of $15 trillion in global bonds carried negative nominal yields. A fifth of all sovereign and corporate debt was priced such that holding it to maturity guaranteed a loss.

We have previously described this market phase as a "Financial Hallucination" - the era in which the basic laws of finance, including the time value of money itself, were suspended. An investor lending to the German government for thirty years and receiving back less than the principal (yield hitting approximately -0.002% first on August 2, 2019) is not participating in a bond market. They are participating in a collective fiction, sustained by institutional inertia and regulatory compulsion, in which the word "yield" had lost any meaning. However, that hallucination ended in 2022 and now, the question is whether we are sleepwalking back into it.

The ECB and Bank of Japan (BOJ) ended their negative-rate experiments when the post-Covid inflation spike gave them cover to normalise. The BOJ's first rate hike in seventeen years came in March 2024. But the underlying conditions that drove them to negative rates in the first place - demographic decline, debt overhang, technology-driven disinflation, weak domestic demand - have not changed. In Japan's case, they have, if anything, intensified. The SNB cut its policy rate to zero as recently as June 2025, a signal that the European rate environment is already moving back toward the edge.

Source: Institute of International Finance Global Debt Monitor, Q3 2025; reported by Reuters/Anadolu, December 2025.

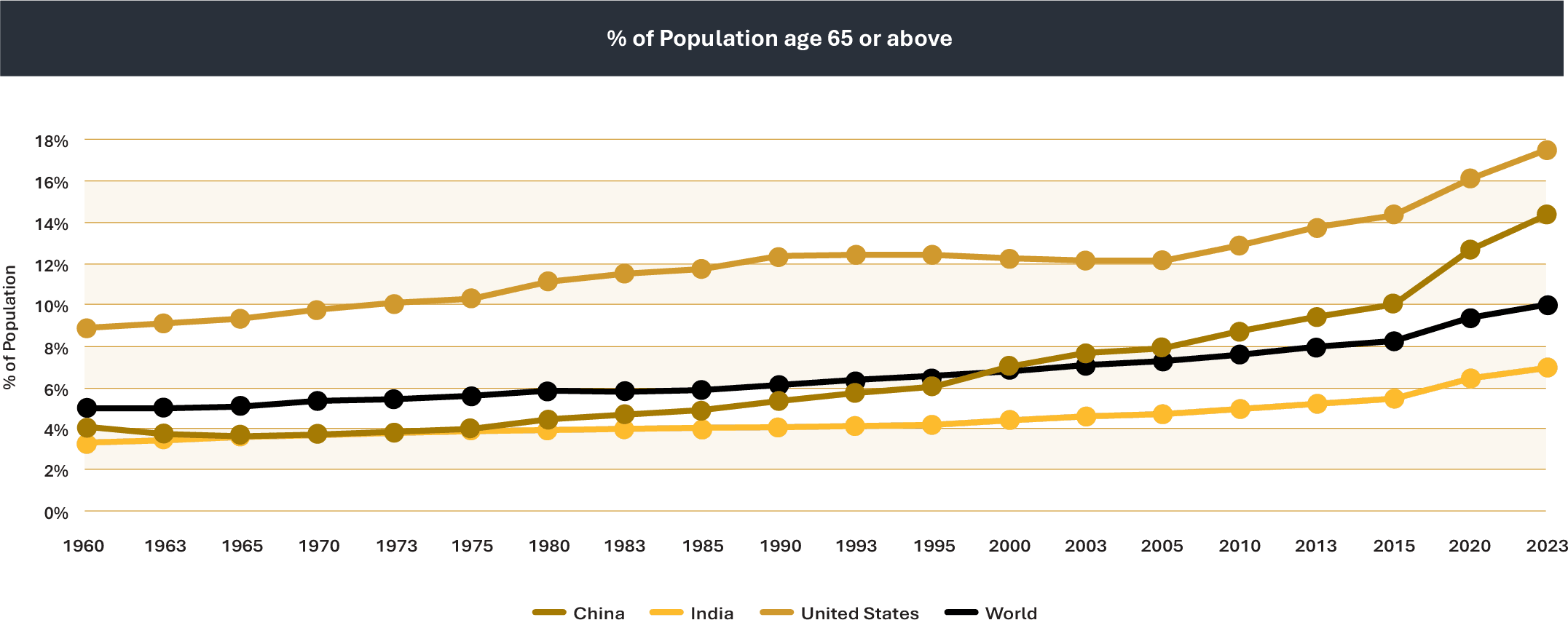

Source: World Bank World Development Indicators, Population ages 65 and above (% of total population), based on UN World Population Prospects; data to 2024.

III. The Recession Nobody is Counting

The last conventional, endogenous US recession ended in June 2009. The expansion that followed lasted 128 months, the longest in the NBER’s chronology, before being interrupted by the extraordinary Covid contraction of February–April 2020. The current cycle has therefore not lasted seventeen uninterrupted years in the formal statistical sense, but the US has gone nearly two decades without a classic private-sector credit recession of the 2001 or 2007–09 variety. The historical base rate of US recessions over the past hundred and fifty years is roughly one every seven to ten years.

When it arrives - and it may - whether triggered by a trade shock, a credit event, AI-driven labour displacement compressing consumer demand, or the kind of geopolitical accident that markets persistently under price - the Fed will respond as it always does. It will cut. It will cut fast. If the recession is severe enough, the destination for the federal funds rate will not be 2 percent, or 1 percent, or zero. Given threats of mass unemployment, massive debt overhangs and where we are in the demographic cycle, there is a chance that base rates may be quickly brought into negative territory.

IV. The Inflation Myth and the Cost of Living

There is a persistent confusion in public monetary debate that deserves direct challenge. The argument runs: inflation is high, therefore interest rates must be high to stop it. It sounds like logic. However, it is not, or at least not always.

Consider what "inflation" means for the median American household. It means not only the cost of groceries, but also the one of rent, a car, a mortgage. For the roughly 65% of Americans who own homes and carry mortgages, and for the majority who finance car purchases, the answer is borrowing costs. As policy rates rose from near zero to 5.25–5.50%, 30-year mortgage rates also rose sharply. On CFPB calculations, the monthly principal-and-interest payment for a median-priced home rose from about $1,359 in January 2021 to $2,891 at the October 2023 mortgage-rate peak, assuming a 5% down payment. These are not abstract inflation statistics. They are cash, gone from household budgets, every month.

The classical inflation toolkit – price controls where warranted, targeted fiscal intervention, supply-chain investment, and antitrust action against concentrated market power – addresses the root causes of price increases without inflicting borrowing costs on the households least able to bear them. Higher rates fight demand-pull inflation, but are way less effective at tackling cost-push inflation. Much of what afflicted Western economies after 2021 was cost-push and supply-shock inflation. Applying demand suppression to a supply problem is the monetary equivalent of treating a broken leg with aspirin.

V. The Death of Fixed Income (As We Knew It)

At negative rates, we believe a government bond is not a fixed-income instrument, but rather a time-limited storage fee. The investor pays the sovereign for the privilege of lending to it. The nominal coupon is a tax, not a return. The pension fund holding thirty-year Bunds at minus 0.4 percent is not investing. It is warehousing capital and watching it slowly evaporate. As we have written elsewhere, this is not merely a paradox of policy; it is a financial hallucination – a condition in which the time value of money, the oldest axiom of finance, is formally suspended by institutional decree. When that hallucination returns, the asset class that calls itself "fixed income" will again be offering neither.

This is not a temporary anomaly. It is the structural destination of a world in which the supply of safe assets is politically constrained, demographic savings gluts drive demand for duration, and technology continuously suppresses the natural rate of interest. When rates return to negative – and based on our analysis the probability-weighted timeline is within the next five years – the bond as a traditional asset class will face an existential question. Allocators who have spent the past two years rebuilding duration exposure on the assumption that 4% yields are the new normal are positioned for a world that is passing.

VI. Conclusion: Forces Fast and Furious

The historian Fernand Braudel distinguished between the evenementielle – the history of events, political cycles, market moves – and the longue duree, the slow structural forces that operate over decades and centuries. The short-term rates story of 2024-2026 is evenementielle: oil shocks, election cycles, tariff regimes, central bank communications. It will likely dominate the headlines, and probably keep rates above zero through the near term.

But the longue duree is different. An ageing population that saves more than it spends. A technology that simultaneously compresses the cost of everything it touches and relentlessly threatens mass unemployment. A debt burden that constrains growth and eventually constrains the rate at which servicing that debt is politically survivable, let alone mathematically sustainable. A seventeen-year expansion that has borrowed heavily against future recoveries. And a central bank tradition - in Europe, in Japan, and potentially in the United States next - that has already shown it will go below zero when it runs out of conventional room.

The Pavlovian response to today's oil price is to expect tighter money. The structural response, once the Pavlovian reflex has run its course, is the same as it was in 2014, in 2016, and in 2020: easier money until rates are no longer a tool and become, instead, a burden on savers and a gift to borrowers, and this appears to be the signature condition of an era we appear to be returning to faster than most anticipate.

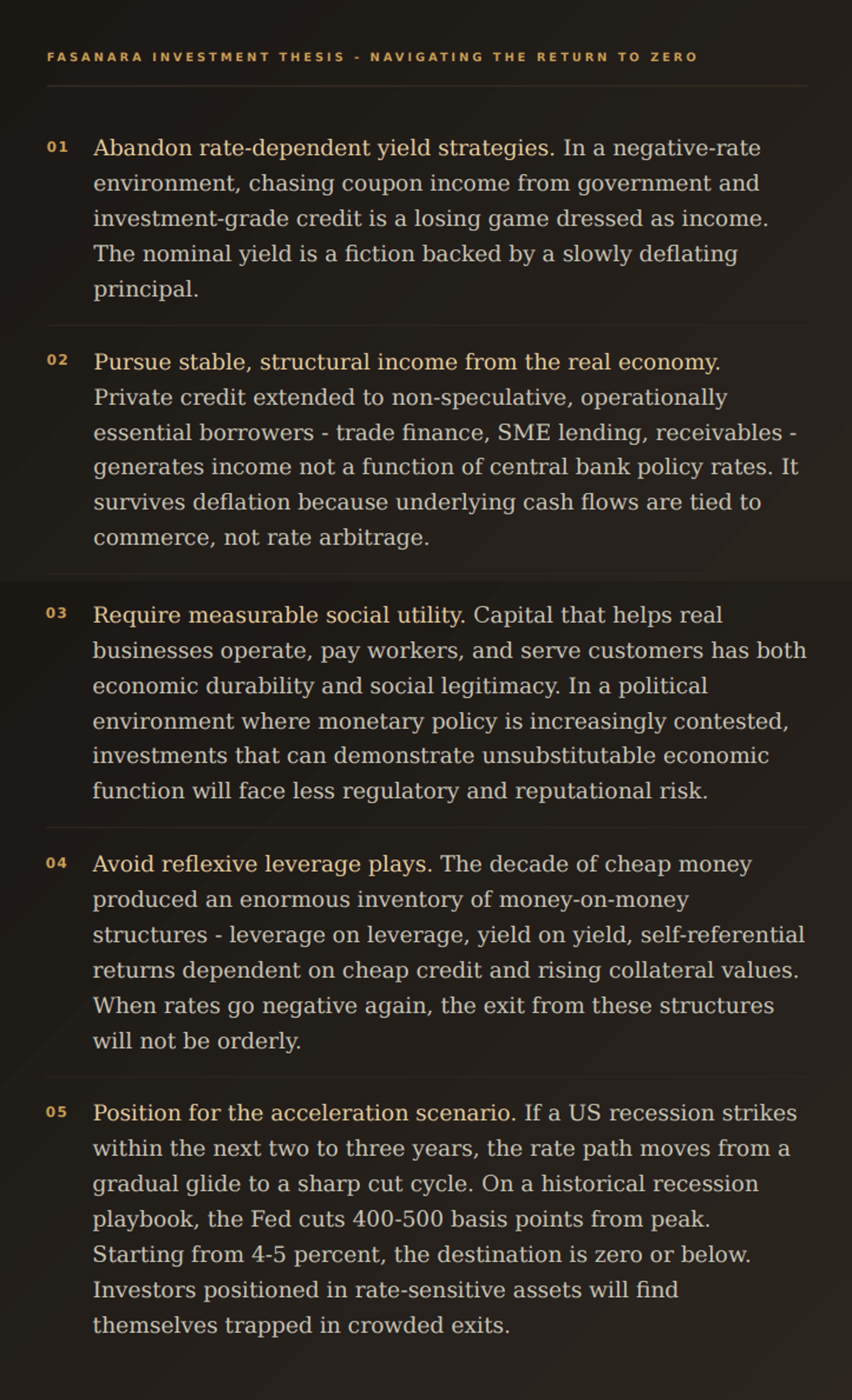

We believe that fixed income, as an asset class defined by its yield, cannot survive this environment intact. What replaces it is direct, productive, socially legible capital deployed in the real economy, earning a return that is not a bet on monetary policy but a function of commerce itself. That is not a niche thesis. That is, on the current trajectory, simply the correct one.

1Source: IMF, Gen-AI: Artificial Intelligence and the Future of Work / IMF Blog, January 2024.

Disclaimer

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell, or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investors or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with their financial professionals. The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Past performance does not predict or guarantee future results. Investing involves risk; principal loss is possible. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. Fasanara Capital Ltd, is authorised and regulated by the Financial Conduct Authority (“FCA”).

Important information on risk

Investing involves risk. The value of any investment and the income from such can go down as well as up, and you may not get back the full amount invested. Changes in the rate of exchange may also cause the value of overseas investments to go up or down. This information represents the views of Fasanara Capital Ltd and its investment specialists. It is not intended to be a forecast of future events and/or guarantee of any future result. Information was obtained from third party sources which we believe to be reliable but are not guaranteed as to their accuracy or completeness. There is no assurance that an investment will provide positive performance over any period of time. This information does not constitute investment research as defined under MiFID.