blog

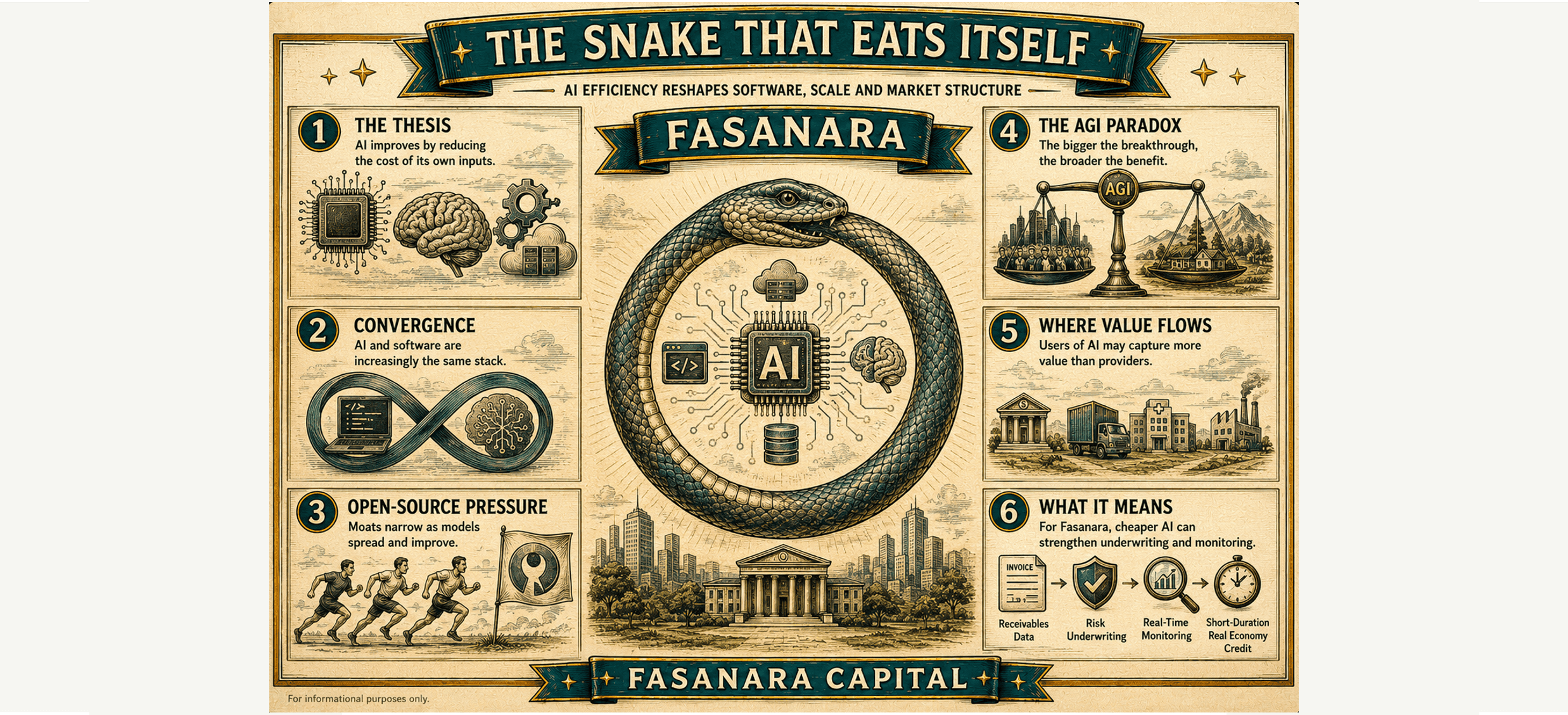

The Snake That Eats Itself

AI is eating software and coding. Then AI eats AI. The terminal direction of AI pricing is downward, even if the path is volatile and premium models retain pockets of pricing power.

Francesco Filia, Founder and CEO

1 June 2026

The convergence nobody is pricing

AI is software. Not metaphorically, but mechanically. It is code that writes code, infrastructure that replaces infrastructure, a tool that automates the production of tools. The venture capital community has priced it as something categorically different, a new layer of the technology stack exempt from the competitive dynamics that compress every other software market. That exemption will not hold.

The convergence argument is simple. AI and coding are, in a number of respects, the same thing. They compete for the same use cases: documentation, debugging, architecture, testing, deployment. They run on the same cloud infrastructure. They are priced by the same institutional buyers. There is no stable equilibrium in which the cost of coding falls toward zero and the cost of AI tokens rises without limit. One will pull the other. The only question is the speed of the adjustment.

It appears that some developer communities are already debating whether AI coding workflows are becoming less predictable and, in certain agentic use cases, less obviously cheaper than junior engineering capacity. That is still more anecdote than settled evidence, but the signal matters: once token consumption becomes a procurement variable rather than a novelty cost, the pricing curve begins to change.

A race to the bottom, by design

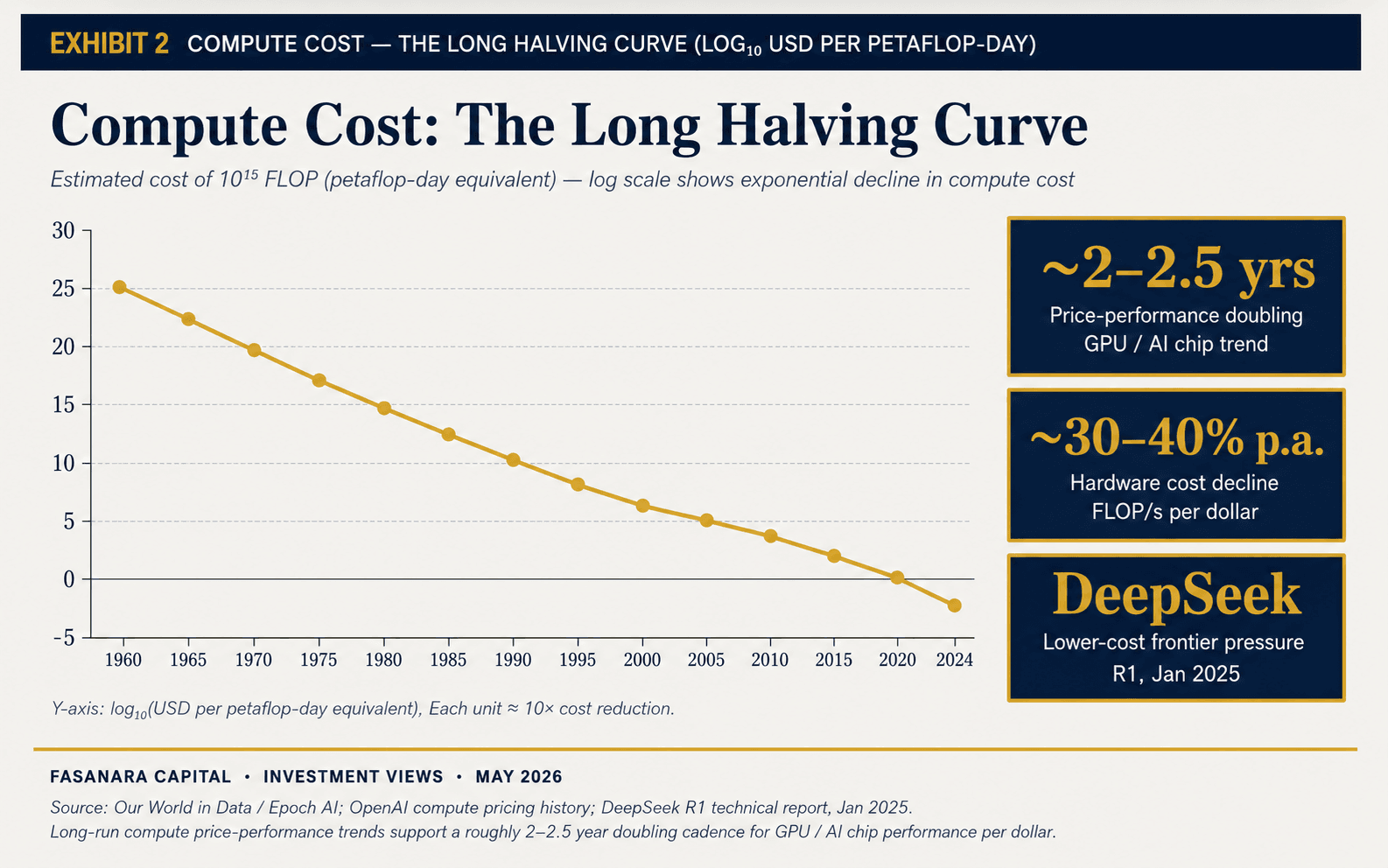

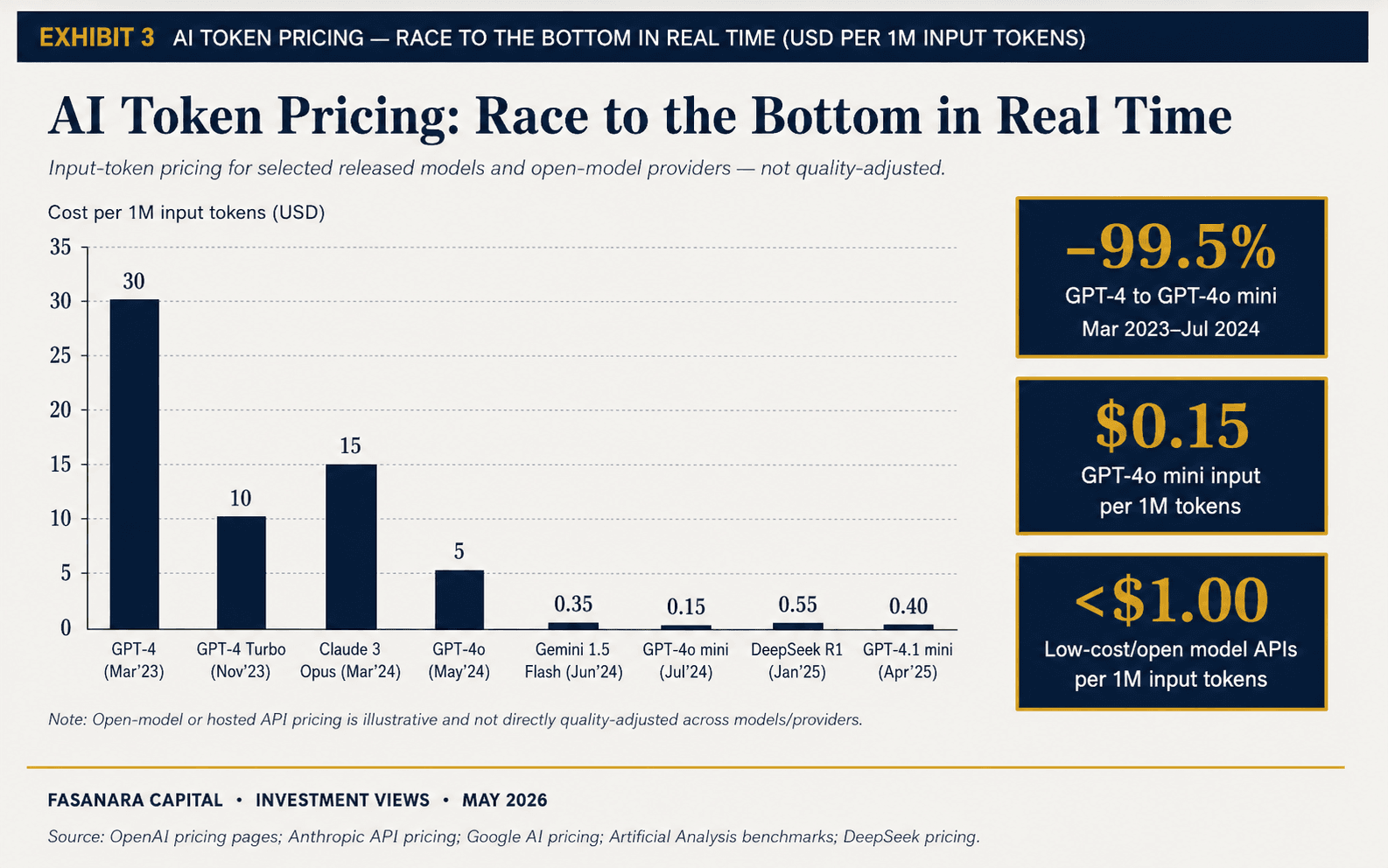

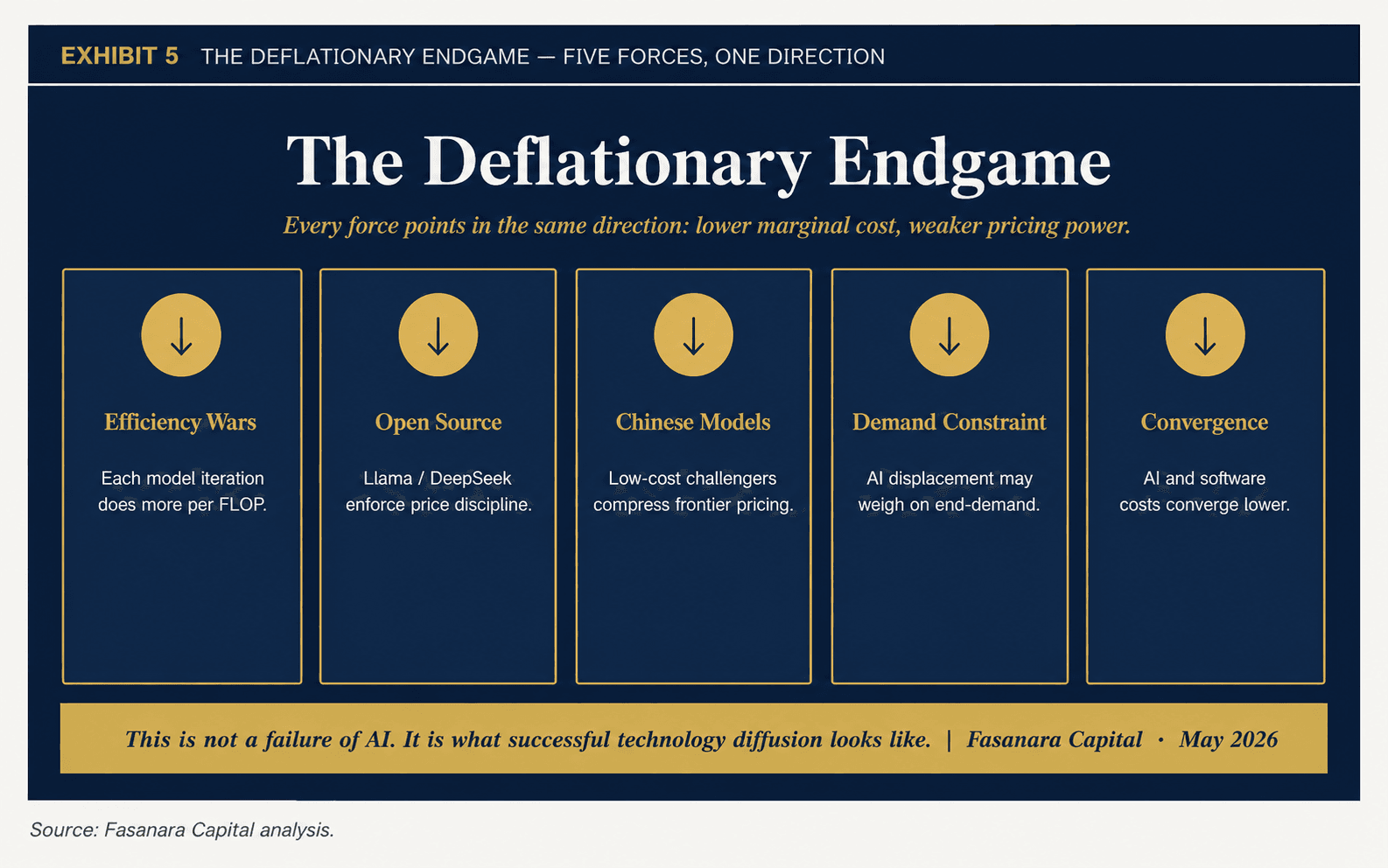

Every major AI lab is optimising for the same thing: doing more with less compute. DeepSeek showed that open and lower-cost model architectures could close much of the perceived performance gap with leading closed models across several reasoning and coding benchmarks. The precise all-in cost comparison remains contested, but the market signal was clear: frontier capability is becoming harder to defend through scale alone. Mistral, Llama, Qwen — the open-source stack is compressing the frontier faster than closed models can monetise it. This is not an anomaly. This is the race working exactly as designed.

Each iteration of the AI arms race does three things simultaneously: it expands what is possible, it reduces the cost per token, and it narrows the moat of whoever was ahead. The leaders are not building durable infrastructure; they are building a staircase that their competitors climb behind them, one step lower per quarter. Every dollar spent on frontier model training is, in part, a donation to the open-source community that reverse-engineers it six months later.

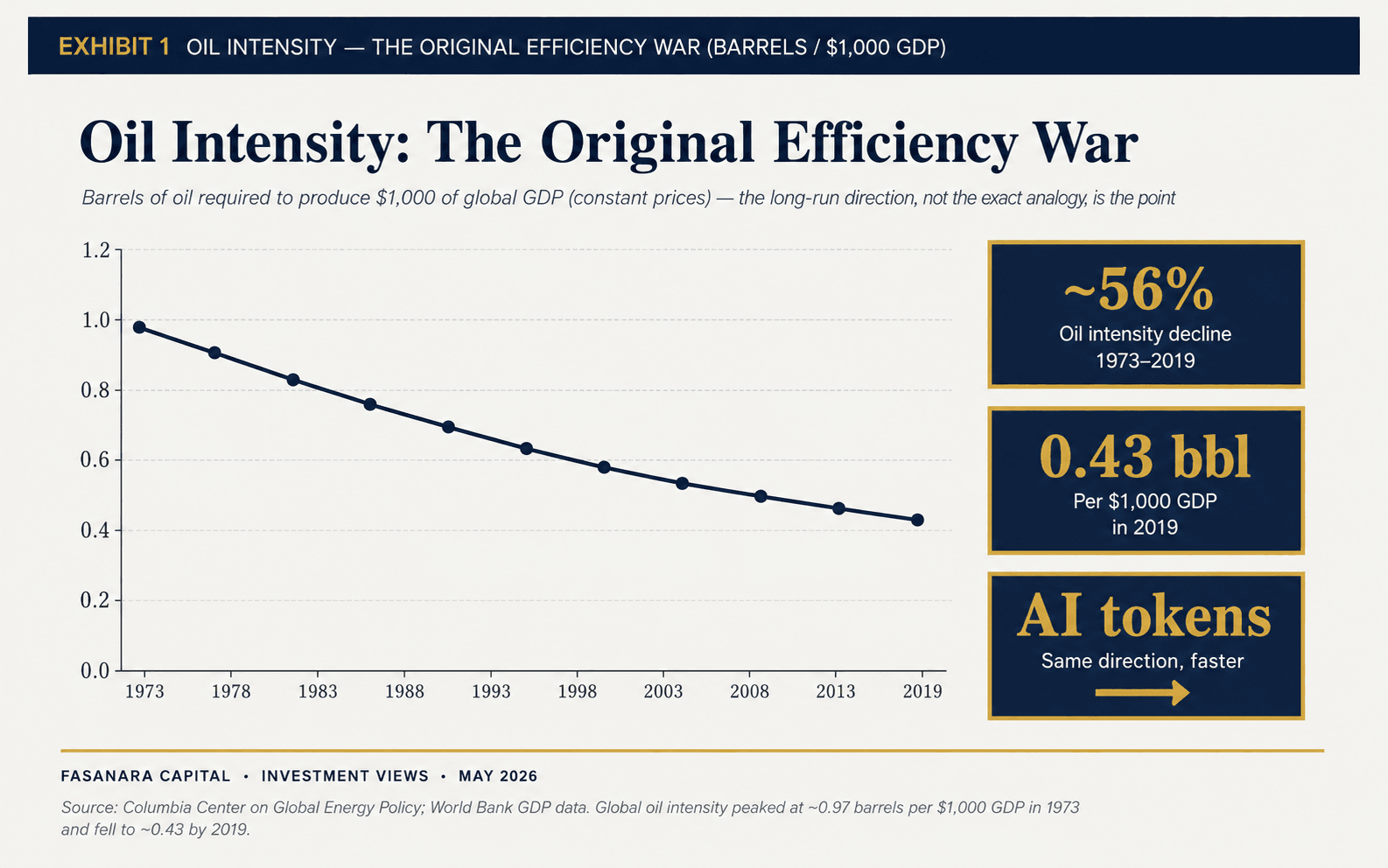

The historical analogy is oil. Global oil intensity has fallen sharply over time: Columbia’s Center on Global Energy Policy estimates that oil consumption per $1,000 of global GDP peaked at around 0.97 barrels in 1973 and had fallen to 0.43 barrels by 2019. The lesson is not that demand disappeared, but that the economy became progressively more efficient in its use of oil. AI tokens are oil. The economy will adapt. The price will fall. The only debate is timing.

A race to the bottom, by design

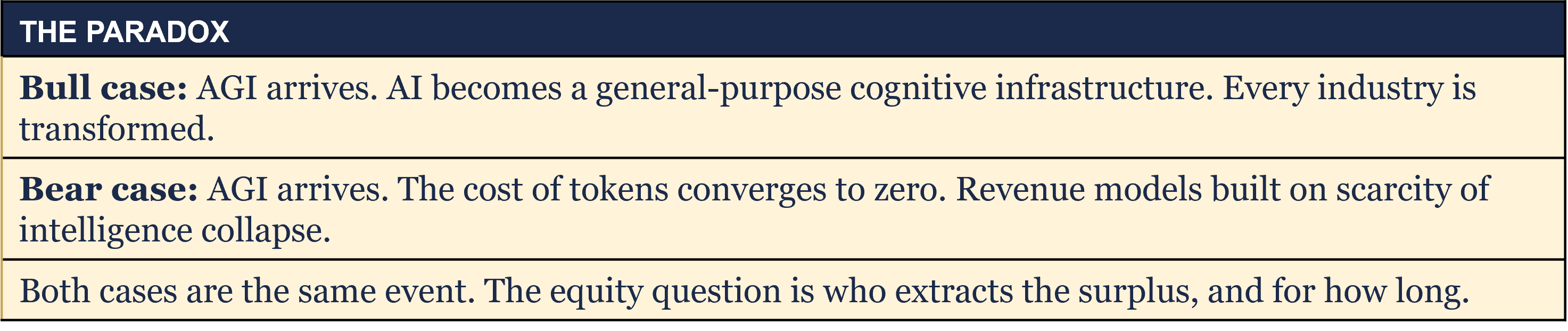

The most powerful argument against AI equity valuations is not that AI will fail. It is that AI will succeed, completely, and on its own terms. AGI, by most definitions that matter to the people evangelising it, means general cognitive capability at or beyond human level. It also means, inescapably, that the cost of intelligence approaches zero. You cannot have unlimited cognitive supply and sustained token pricing. The two are arithmetically incompatible.

The valuation argument for AI companies depends on a specific, narrow window: AGI is close enough to price in the upside, but far enough away that current infrastructure and pricing power have time to compound. If AGI arrives faster than the bull case assumes, the collateral implodes by the same promise that inflated it. If AGI takes longer, the efficiency wars of the intervening period compress margins to SaaS levels before the breakthrough arrives.

Either way, the AI companies are not a category apart from software. They are software houses, very good software houses, in some cases, but subject to the same dynamics that have always governed the sector: competition, commoditisation, and the relentless march of open-source alternatives.

Demand is always the signal

There is a second deflationary vector that the AI bull case consistently underweights: demand destruction from the thing it is supposed to serve. AI is being deployed in an economy where, by the explicit design of the people deploying it, large numbers of workers in knowledge-intensive roles will lose their jobs or see their income compressed. Those workers are also consumers.

Inflation assumes that someone buys something at the posted price. It is a clearing mechanism. Real economies are not Giffen goods — demand does not rise automatically with price. If AI-driven automation removes sufficient purchasing power from the middle of the income distribution, the addressable market for AI-priced products shrinks alongside the workforce that is being replaced. This is not purely theoretical. The macro effect of labour-displacing technology depends on the balance between productivity gains, investment demand and household income effects. If income compression arrives faster than new demand formation, the result can be disinflationary.

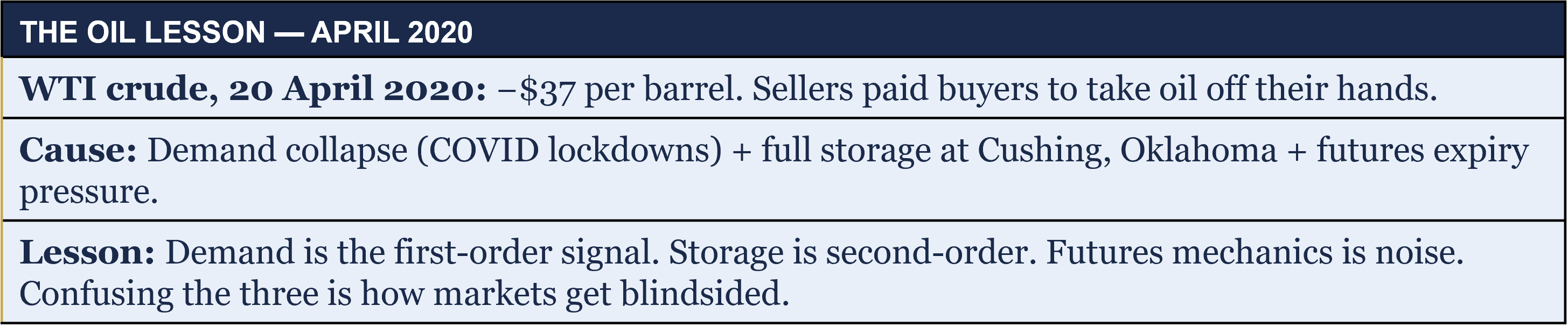

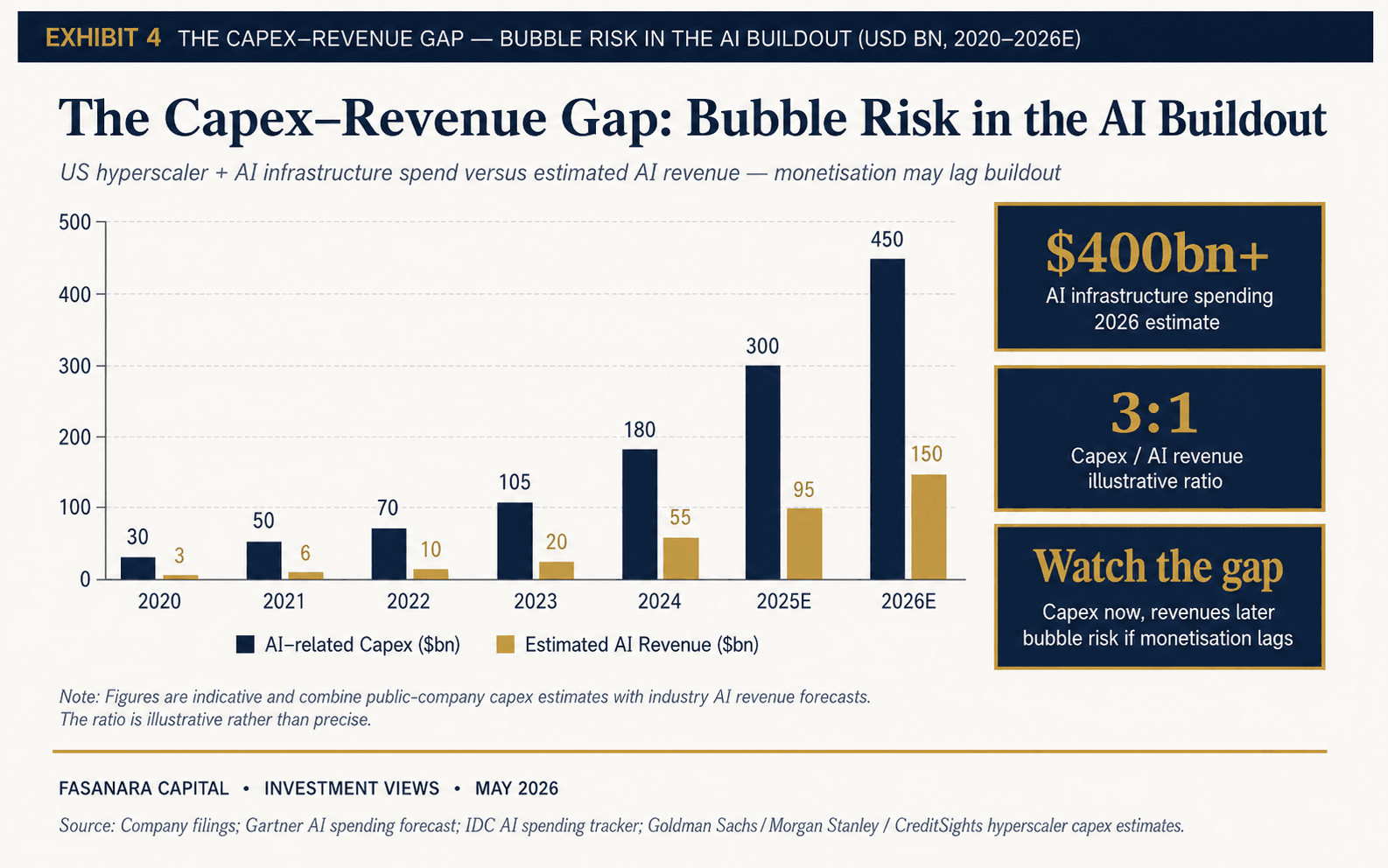

The April 2020 oil episode is instructive. West Texas Intermediate crude fell to negative $37 per barrel, not because oil became worthless, but because demand collapsed suddenly, storage filled instantaneously, and the futures market had nowhere to go. The cause was demand. Storage and futures mechanics were second-order effects, not the signal. Confusing signal with noise in 2020 was expensive. The same confusion, applied to AI demand assumptions, is the current version of that error.

The Fasanara position

None of this is an argument against AI as a technology. It is an argument against AI as a sustained pricing moat. The distinction matters. The economic value created by AI, particularly in logistics, healthcare, credit, and manufacturing, could be significant. But the value is likely to accrue to the users of AI, not primarily to the providers of the tokens. Just as the economic value of the internet accrued overwhelmingly to the businesses that ran on it, not to the telecommunications companies that sold the bandwidth.

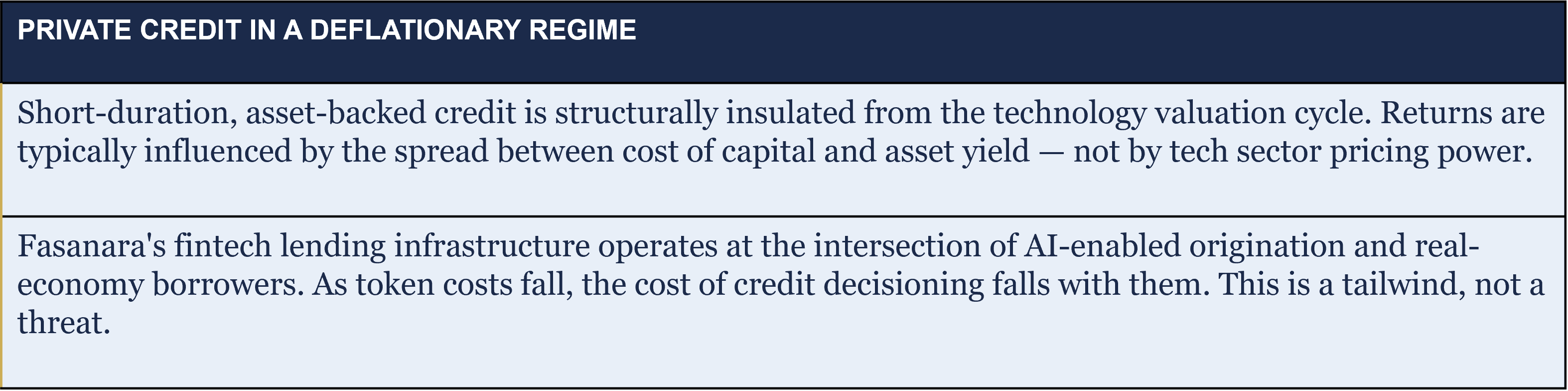

For Fasanara, the implication is a tailwind, not a headwind. We operate at the intersection of technology and real-economy credit. Our origination platforms use AI-enabled underwriting, fraud detection, and portfolio monitoring. As compute costs fall and model quality rises, the cost of building and running those platforms falls with them. The deflationary dynamic in AI is, for us, a reduction in the cost of our infrastructure, not a threat to our revenue model, which is driven by credit spreads on real assets, not by software licensing.

The allocation question for institutional investors is different. Portfolios with material exposure to technology equities built on the assumption of durable AI pricing power should be examined with fresh eyes . The deflationary logic of AI is not a tail risk — it is the central tendency of a technology that is explicitly designed to optimise itself out of expensive territory.

What to watch

The pace of open-source frontier model development is the most important variable. If models trained at a fraction of closed-model cost continue to close the performance gap, and the evidence from the last eighteen months suggests they will, the timeline for pricing compression accelerates materially. Watch DeepSeek, Llama, and the Chinese domestic model ecosystem in particular. These are not niche academic projects. They are the competitive pressure that enforces the terminal price.

The second variable is enterprise procurement behaviour. Corporations are beginning to negotiate AI contracts the way they negotiate cloud contracts, on volume, on lock-in risk, on the cost of switching. As procurement becomes more sophisticated, the premium attached to frontier models will compress. The shift from enthusiasm to procurement discipline is already underway in the US and European enterprise market.

The third variable is the labour market response. If AI-driven displacement moves faster than the fiscal and monetary framework can absorb it, the demand-side constraint on AI pricing becomes binding sooner than the consensus assumes. We are not predicting this. We are noting that it is the mechanism that most optimistic AI forecasts leave entirely out of the model.

Disclaimer

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell, or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investors or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with their financial professionals. The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Past performance does not predict or guarantee future results. Investing involves risk; principal loss is possible. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. Fasanara Capital Ltd, is authorised and regulated by the Financial Conduct Authority (“FCA”).

Important information on risk

Investing involves risk. The value of any investment and the income from such can go down as well as up, and you may not get back the full amount invested. Changes in the rate of exchange may also cause the value of overseas investments to go up or down. This information represents the views of Fasanara Capital Ltd and its investment specialists. It is not intended to be a forecast of future events and/or guarantee of any future result. Information was obtained from third party sources which we believe to be reliable but are not guaranteed as to their accuracy or completeness. There is no assurance that an investment will provide positive performance over any period of time. This information does not constitute investment research as defined under MiFID.