blog

Tokenization: The New Market Infrastructure

David Vatchev, Head of Tokenization

17 March 2026

From Experiment to Core Market Infrastructure

Tokenization has progressed from a fringe concept to a foundational layer in global finance. At its core, it’s a simple idea with potentially profound consequences: recording asset ownership on secure, programmable blockchains. This allows any financial instrument, from credit and real estate to sovereign debt, to exist as a single, verifiable digital record.

This evolution delivers two structural benefits: instant settlement and broader access.

Transactions that once took days can now settle in seconds, reducing counterparty risk and freeing trapped collateral. Meanwhile, traditionally illiquid assets, such as loan portfolios, infrastructure projects, or private credit funds, can be fractionalised, expanding access for a wider base of institutional and qualified investors.

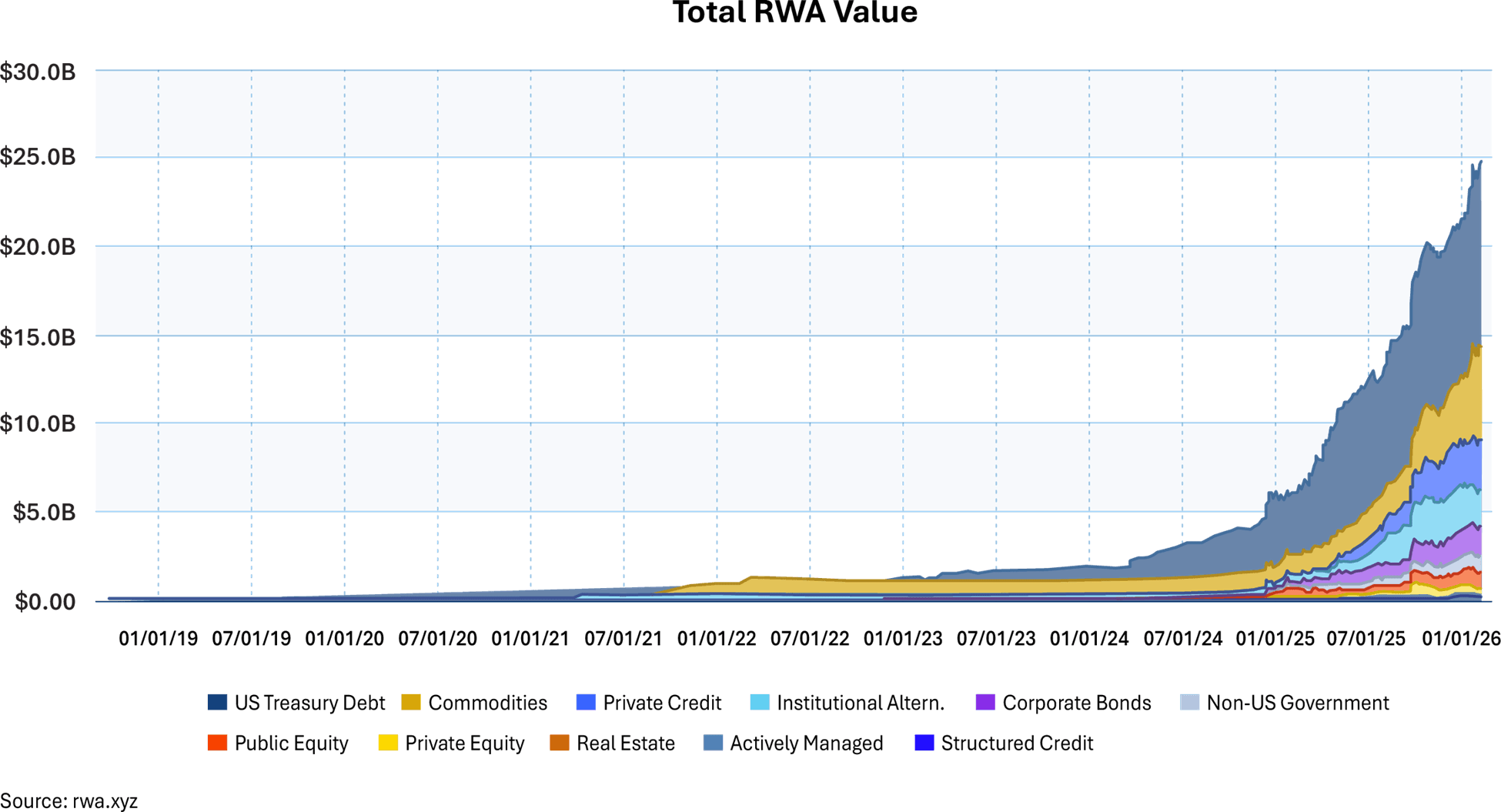

Global adoption confirms the acceleration. The value of tokenized real‑world assets has increased roughly 300% in under two years. Tokenization has moved firmly from the margins into the mainstream of financial market infrastructure.

Source: rwa.xyz

Institutional Adoption Hits Escape Velocity

The biggest shift in the last 12–18 months is who is building on-chain. Major exchanges, custodians, and banks are integrating tokenized rails directly into their market infrastructure.

A defining example is the New York Stock Exchange, which announced a new tokenized securities platform in early 2026. The venue is designed to support 24/7 trading of tokenized stocks and ETFs, instant on chain settlement, and dollar sized orders, all while preserving existing protections and regulatory standards. It aims to make tokenized shares fully fungible with traditional securities so that investors retain dividends and governance rights, irrespective of whether they hold a conventional or tokenized form.

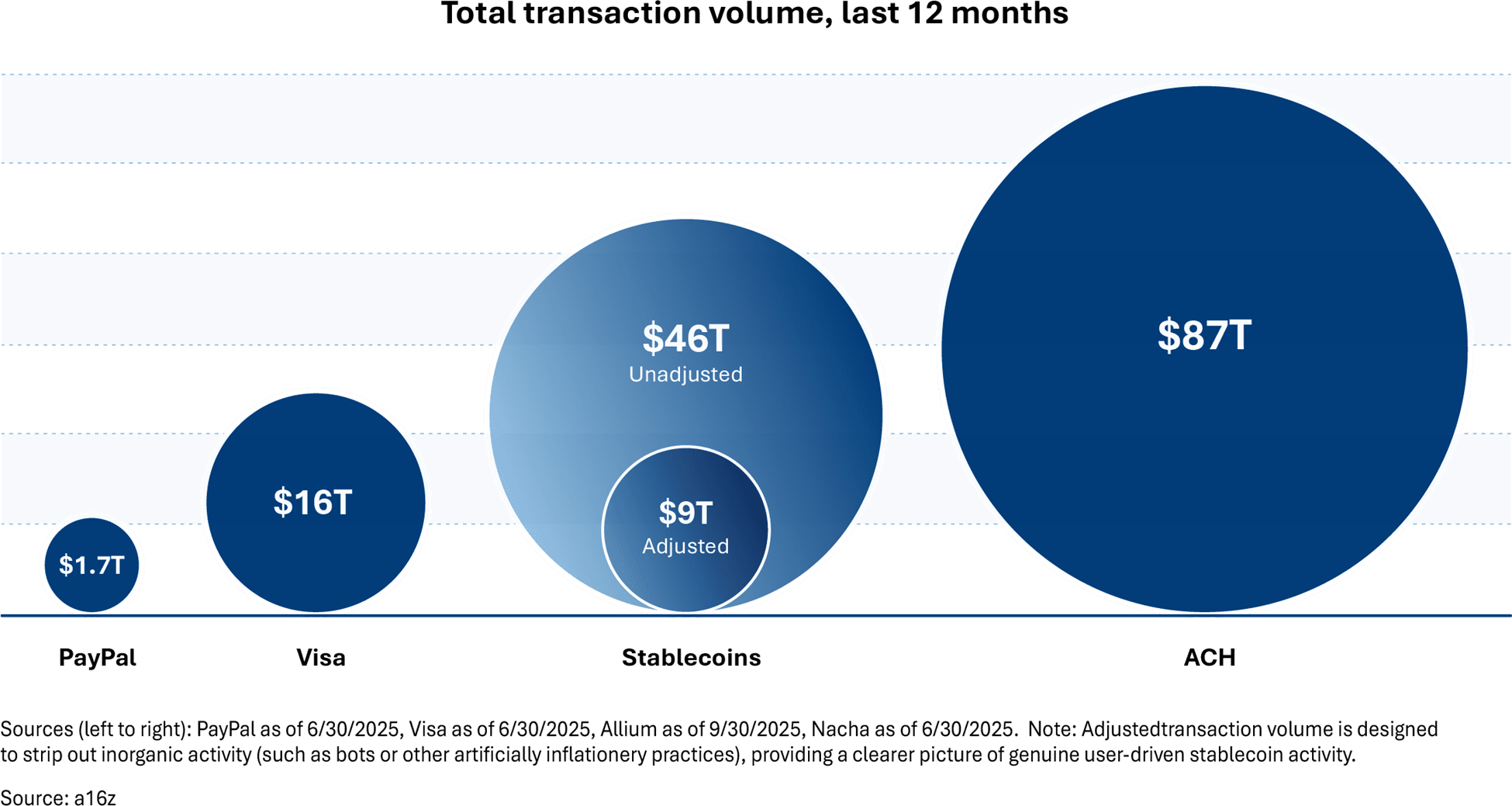

In parallel, the “cash leg” of markets continues migrating to digital rails. Stablecoins are now processing more adjusted volume each month than major payment networks such as Visa and PayPal, according to Delphi Digital.

Source: a16zcrypto

This convergence of tokenized assets and tokenized money is driving the next growth of market infrastructure evolution.

Efficiency, Liquidity and Access: Use Cases in Action

The most compelling use cases of tokenization are emerging where today’s frictions are greatest: private markets and collateral management. Tokenized systems allow delivery versus payment to occur atomically: assets and cash change hands simultaneously through smart contracts. This reduces settlement risk and can materially improve capital efficiency for dealers, prime brokers, and asset managers. Freed from multi‑day settlement windows, firms can redeploy capital more quickly and support larger portfolios with the same balance sheet.

For private credit and loan funds, long characterised by multi‑year lockups and narrow redemption windows, the opportunity could be even clearer. Tokenized fund shares can now be fractionalised and used as collateral in on‑chain lending venues, creating broader investor access and an additional liquidity layer on top of illiquid underlying assets2. New global investors can access private markets previously out of reach, while existing holders who previously had to wait for annual redemption cycles can now access liquidity by selling or borrowing against tokenized positions when needed.

Source: Tokenized assets in a decentralized economy: Balancing efficiency, value, and risks

2Investments in private credit and loan funds, including tokenized forms, may be illiquid and subject to significant risks. There may be occasions when you experience a delay or receive less than expected when selling your investment.

At the system level, tokenization also improves collateral mobility. Analysis from the World Economic Forum suggest that only $25 trillion of securities are currently eligible for collateral use, out of a potential $230 trillion, because of fragmentation and settlement frictions. In this regard, tokenization has the potential to expand liquidity and capital efficiency.

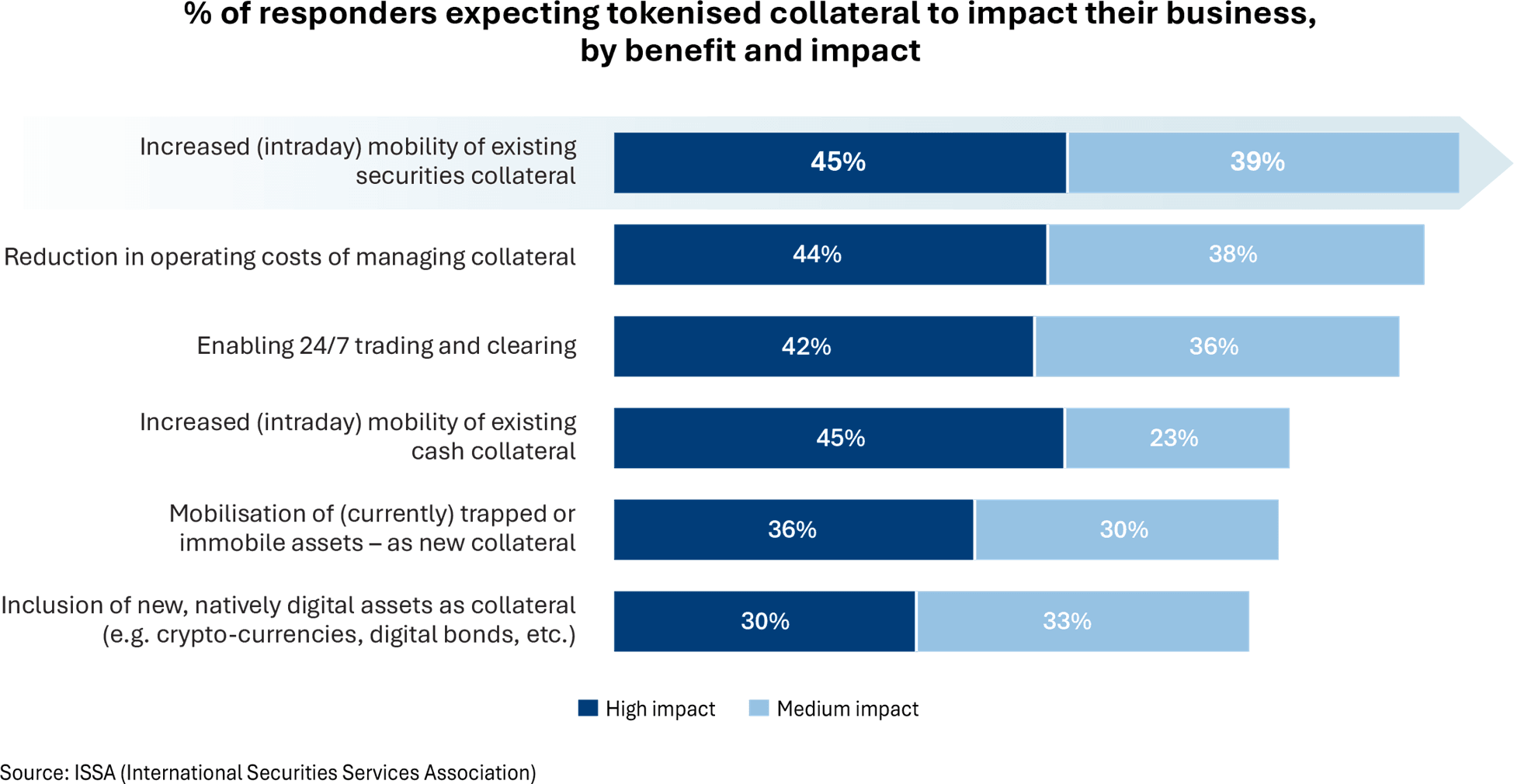

Increasingly, more major market participants see tokenization as a critical enabler of collateral mobility, as evidenced below.

Source: ISSA (International Securities Services Association)

By standardising how assets are represented and moved, tokenization allows the same asset to support multiple financing and hedging needs over shorter timeframes, without losing traceability.

However, it should be borne in mind that while Tokenization can streamline settlement and improve record-keeping, it does not entirely remove risk. The underlying economics still depend on credit performance, valuation assumptions and market liquidity, and any additional liquidity layer relies on secondary-market depth and vehicle terms, which can weaken in stressed conditions. On-chain structures may also introduce operational and technology dependencies (smart-contract/oracle risk, custody and key management, platform governance and third-party infrastructure), and where stablecoins are used as the cash leg, de-pegging and liquidity shocks can affect settlement and collateral values. Regulatory requirements on eligibility, market infrastructure and disclosures continue to evolve across jurisdictions.

Conclusion: Embracing the New Infrastructure

What began with Bitcoin over a decade ago has evolved into a broad movement to upgrade how value is issued, traded, and settled across the financial system. Blockchain‑based networks are enabling a world of always‑on markets with instantaneous exchange of value. This begins to optimise capital efficiency on a grand scale.

For investors and asset managers, the implications could be profound. Early adoption of tokenized platforms may offer the chance to shape industry standards and capture new opportunities. Just as past financial revolutions (from electronic trading to exchange‑traded funds) rewarded first movers, it may be that today’s pioneers of on‑chain finance stand to gain a competitive edge. That said, outcomes may be uncertain and adoption depends on market infrastructure, liquidity, technology resilience and evolving regulatory requirements.

In our view, tokenization could mark a significant shift in market infrastructure, converging traditional finance with the digital asset ecosystem. Whilst its potential downsides and uncertainty should be considered, tokenization connects the risk and return of traditional assets with the speed and programmability of digital networks. For private credit, it offers a path to observable cashflows, measurable risk in real time, and non‑episodic liquidity, features that could potentially redefine the asset class over the coming decade.

1Past growth is not a reliable indicator of future results. The value and adoption of tokenized assets may fluctuate and are subject to various risks.

Disclaimer

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell, or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investors or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with their financial professionals. The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Past performance does not predict or guarantee future results. Investing involves risk; principal loss is possible. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. Fasanara Capital Ltd, is authorised and regulated by the Financial Conduct Authority (“FCA”).

Important information on risk

Investing involves risk. The value of any investment and the income from such can go down as well as up, and you may not get back the full amount invested. Past performance is not a guarantee of future returns. Changes in the rate of exchange may also cause the value of overseas investments to go up or down. This information represents the views of Fasanara Capital Ltd and its investment specialists. It is not intended to be a forecast of future events and/or guarantee of any future result. Information was obtained from third party sources which we believe to be reliable but are not guaranteed as to their accuracy or completeness. There is no assurance that an investment will provide positive performance over any period of time. This information does not constitute investment research as defined under MiFID.