blog

The Return of Income and the Rise of Dispersion

David Vatchev, Head of Tokenization

18 May 2026

In our Fasanara Key Themes for 2026 article, we observed that markets were entering a new regime defined by tighter liquidity, higher rates, and increasing dispersion across asset classes.

A few months into the year, this is now playing out. The shift in rates and financial conditions has brought income back into focus, following a decade dominated by capital appreciation and multiple expansion.

However, the defining feature of the current environment is not simply higher yields, but greater dispersion. Assets that appear similar on the surface are behaving very differently beneath it, with outcomes increasingly driven by structure, refinancing dynamics, and exposure to real economy cashflows. Geopolitical fragmentation, macro uncertainty and rapid technological change are reinforcing this divergence across markets and sectors. For allocators, the focus is on identifying income streams that are durable and resilient across cycles.

The return of income

After years of compressed yields, income is once again a meaningful contributor to total returns. Higher base rates and wider spreads have restored carry as a central component of portfolio construction. This shift, visible across asset classes, reflects a structural reset in the cost of capital. Allocators are increasingly prioritising stable, recurring cashflows over uncertain capital gains.

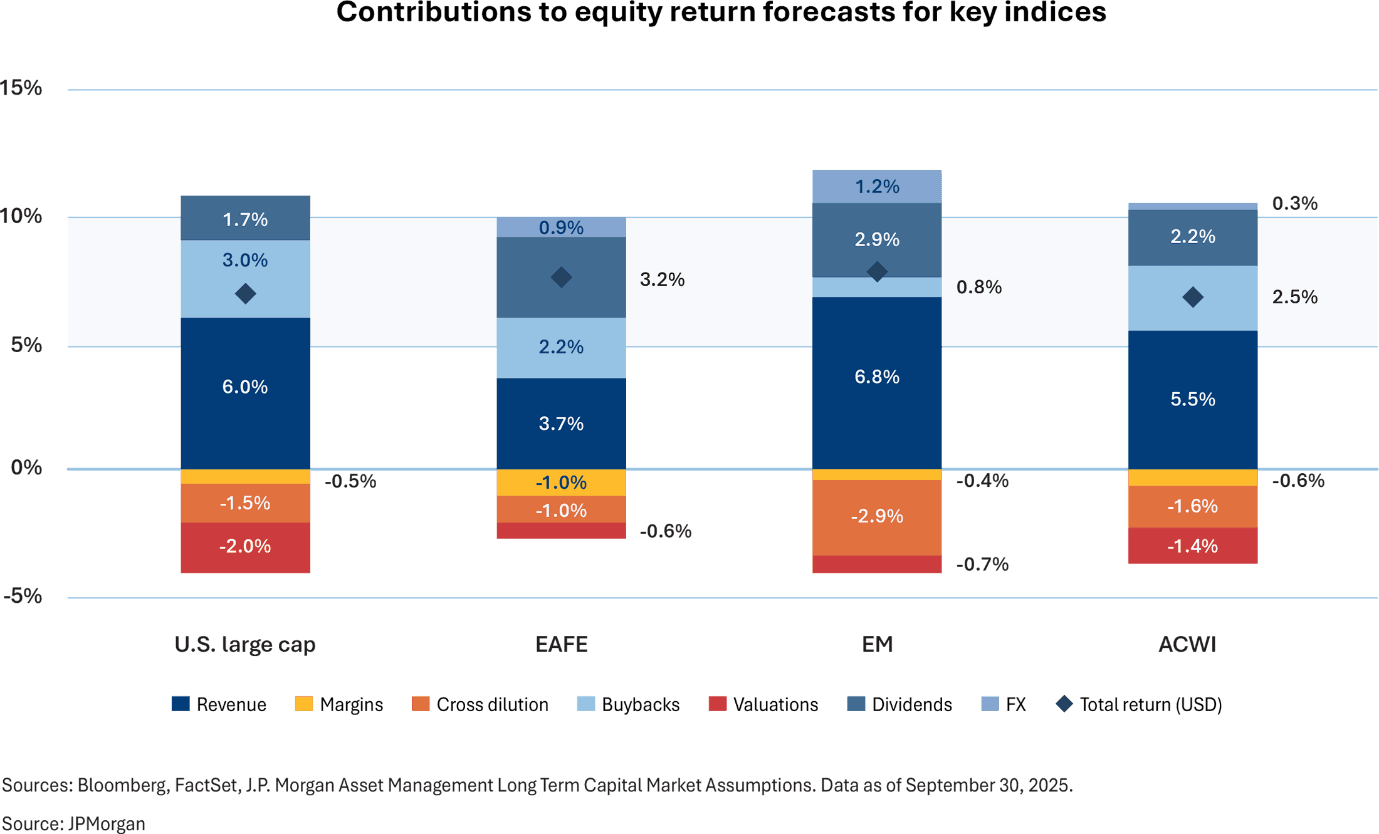

However, the re-emergence of income does not imply uniformity. The underlying drivers of yield have become more complex and more differentiated. As JP Morgan’s 2026 outlook illustrates, the era of multiple expansion has inverted into a valuation drag, leaving dividends and carry as the primary anchors of total return. This transition can be understood as a shift from capital-driven to income-driven return profiles:

Not all yield is equal

Assets labelled as “yield” now encompass a wide range of risk profiles, with outcomes increasingly driven by differences in leverage, duration, liquidity and structure.

Two investments offering similar headline yields may carry very different exposures:

- Duration (multi-year vs short dated)

- Repayment source (enterprise value vs cashflow)

- Concentration (single-name vs granular)

- Liquidity profile

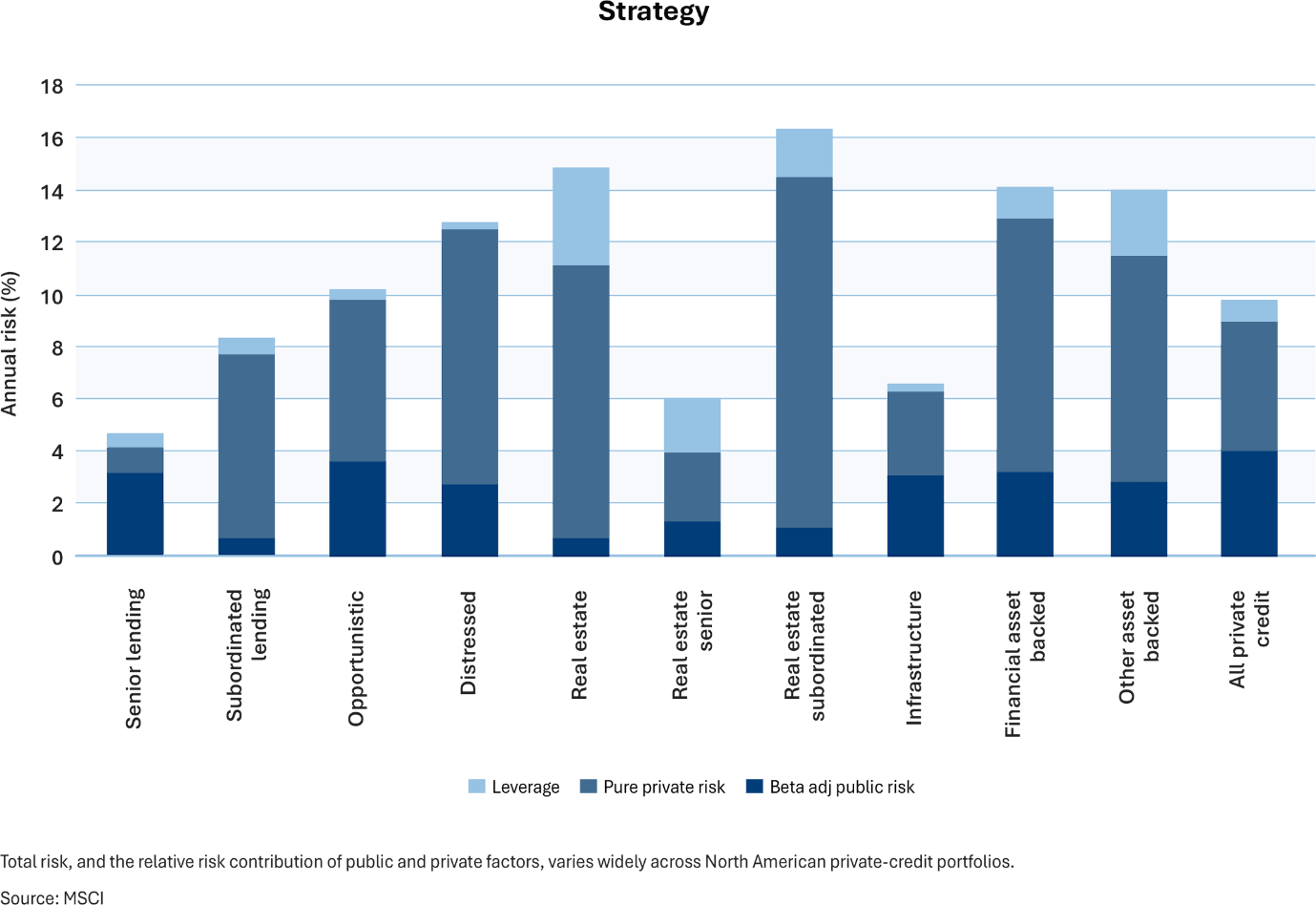

As a result, headline “yield” becomes a surface-level metric, often masking underlying structural differences and risk assumptions. These differences frequently sit beneath similar yields, making comparisons misleading. As MSCI shows in its Private Credit Factor Model 'yield' is a composite of very different drivers.

Their decomposition analysis reveals that public market proxies often miss the pure private risk component entirely. For instance, while strategy-level data may suggest similar risk profiles, security-level analysis shows total risk can range from 2.3% to 7.4%, with drivers shifting from broad market credit spreads to concentrated, asset-specific risks as portfolios mature.

Dispersion becomes the dominant feature

As financial conditions tighten, dispersion across credit markets is increasing. Stronger borrowers and structures continue to access capital on reasonable terms, while weaker credits face rising costs or limited availability. This dynamic is now visible across sectors, sponsors and strategies. Refinancing conditions, sector-specific pressures and varying underwriting standards are driving widening performance gaps.

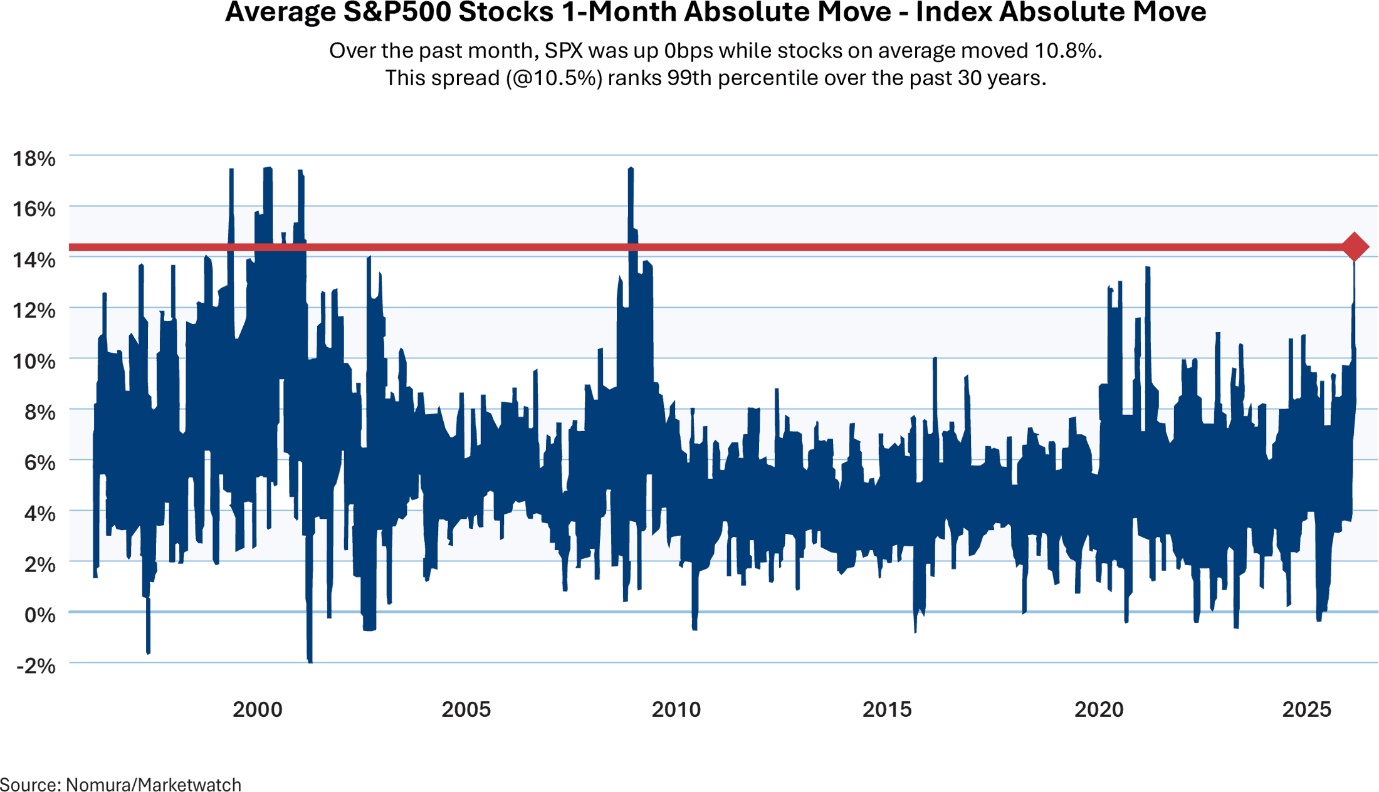

The most visible dispersion has been a dramatic repricing of software and software-related leveraged loans. The sell off has spilled into business development companies and alternative asset managers, where software is a large underlying exposure. The 2026 market exhibits extreme dispersion, with a 99th-percentile performance gap separating leading sectors from the sharp rout that has dropped software equities by 30%.

While the S&P 500 remains range bound, this selective pressure is driving a violent repricing of risk. This late cycle environment is defined by selective pressure and differentiated outcomes. In an income driven environment, the temptation to chase higher yields increases. However, this can obscure underlying risks. Higher yields may reflect:

- Greater leverage

- Longer duration

- Weaker covenant protection

- Reliance on favourable exit conditions

As dispersion widens, these risks become more pronounced. Strategies that appear attractive on a headline basis may prove less resilient under stress. This widening dispersion is a natural outcome of tighter liquidity and higher refinancing costs.

What drives resilience in income strategies

In a more fragmented market, outcomes are increasingly determined by how income is structured and how risk is carried over time. These structural characteristics shape how portfolios behave under stress, how quickly risks emerge, and how effectively positions can be adjusted as conditions change. Strategies built around shorter-duration, cashflow-based exposures tend to offer greater visibility into performance and more flexibility in managing evolving risks.

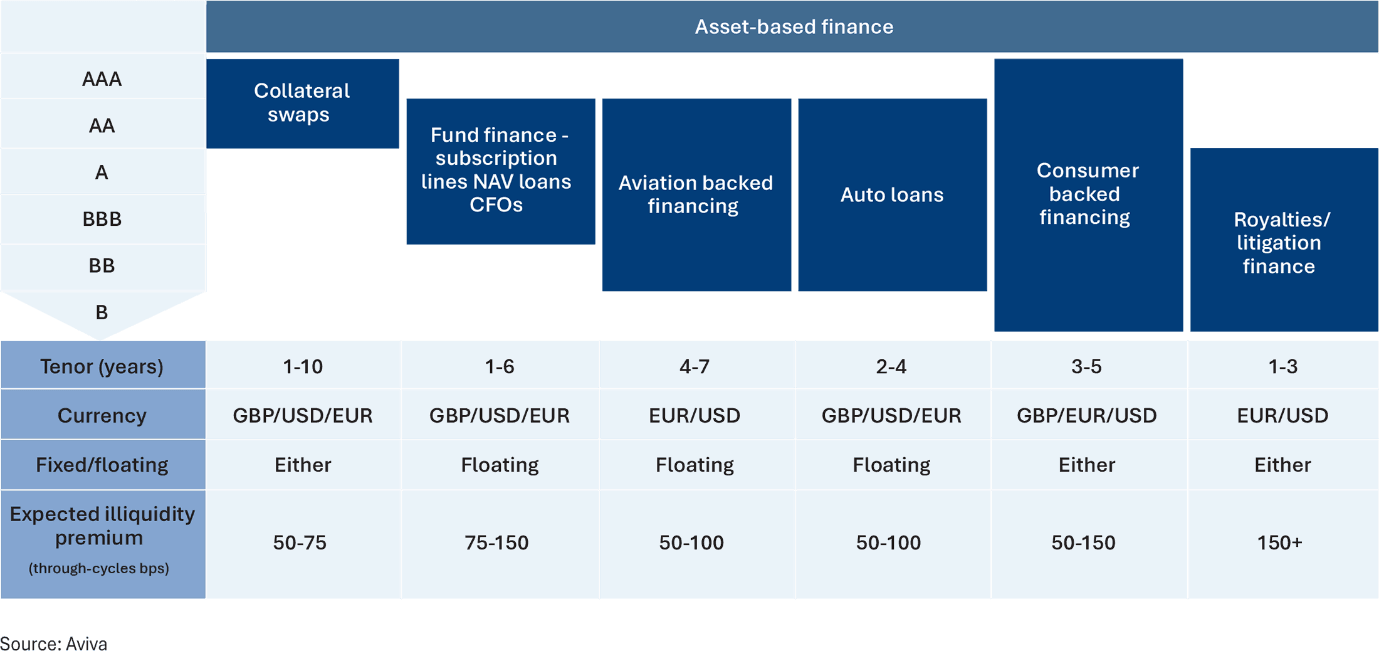

In our view, Asset-Based Finance (ABF) is one example of this approach, which aims to offer flexibility to meet diverse investor risk and return preferences, with strategies built around:

- Shorter duration

- Asset-level cashflows

- High granularity

- Self-liquidating structures

These structural characteristics translate directly into portfolio behaviour under stress, and underpin how real-economy credit strategies are increasingly being integrated into more transparent and liquid investment frameworks.

Conclusion: what this means for allocators

Markets are entering a phase where income and selection drive outcomes. Allocators are increasingly differentiating between underlying structures, risk drivers and liquidity profiles, with a more granular approach to portfolio construction.

As dispersion widens, greater emphasis is placed on how income is generated and how it behaves under different conditions. This environment rewards disciplined underwriting and thoughtful structuring, while the opportunity lies in identifying income streams that are durable and resilient across cycles.

Disclaimer

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell, or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investors or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with their financial professionals. The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Past performance does not predict or guarantee future results. Investing involves risk; principal loss is possible. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. Fasanara Capital Ltd, is authorised and regulated by the Financial Conduct Authority (“FCA”).

Important information on risk

Investing involves risk. The value of any investment and the income from such can go down as well as up, and you may not get back the full amount invested. Past performance is not a guarantee of future returns. Changes in the rate of exchange may also cause the value of overseas investments to go up or down. This information represents the views of Fasanara Capital Ltd and its investment specialists. It is not intended to be a forecast of future events and/or guarantee of any future result. Information was obtained from third party sources which we believe to be reliable but are not guaranteed as to their accuracy or completeness. There is no assurance that an investment will provide positive performance over any period of time. This information does not constitute investment research as defined under MiFID.