blog

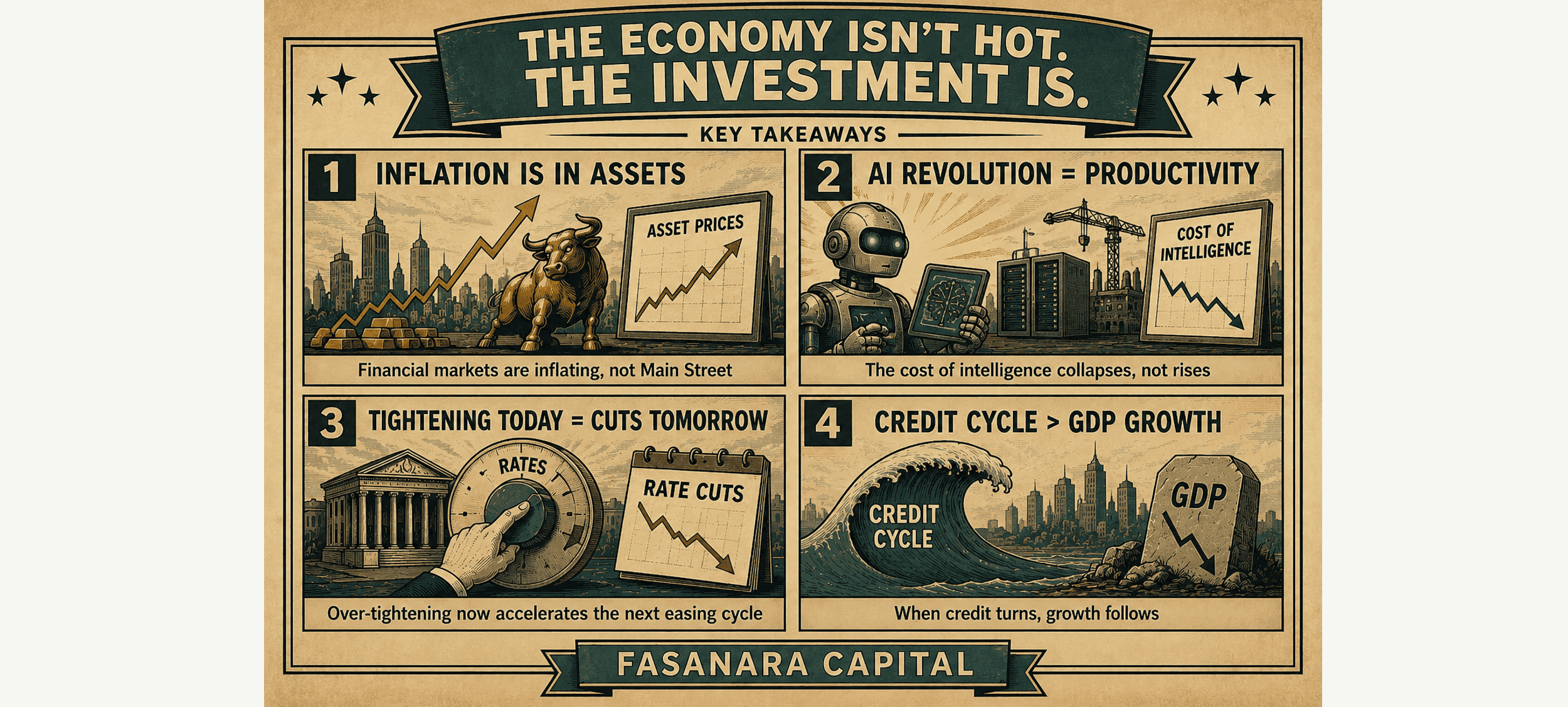

The Economy Isn't Hot. The Investment Is.

AI Capex , central banks, and the next credit cycle. Monetary policy operates on the whole economy. The boom does not.

Francesco Filia, Founder and CEO

30 June 2026

The composition problem

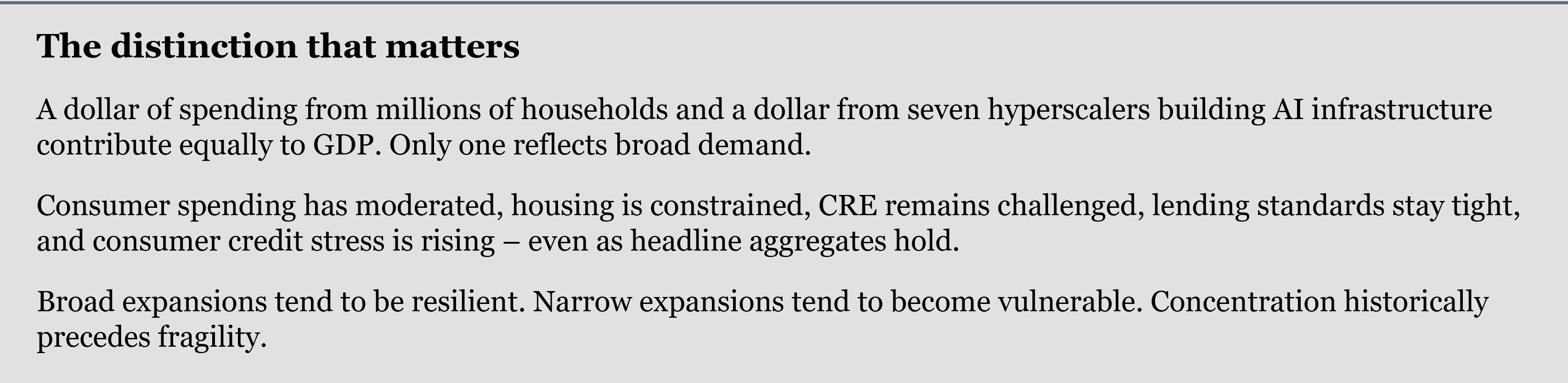

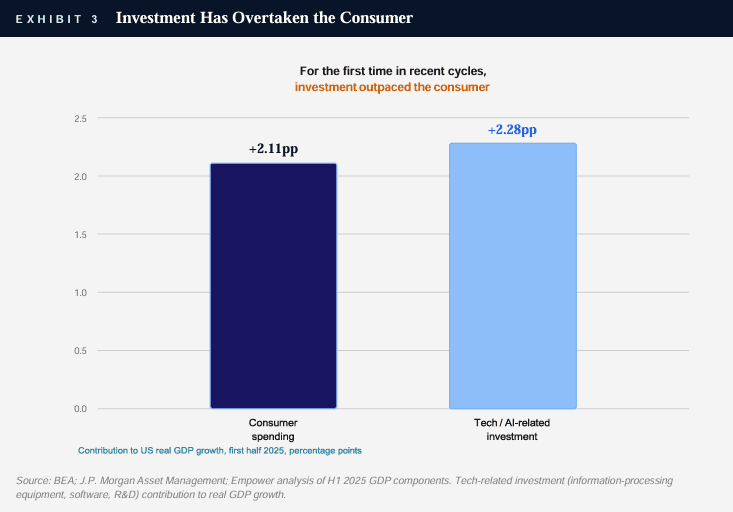

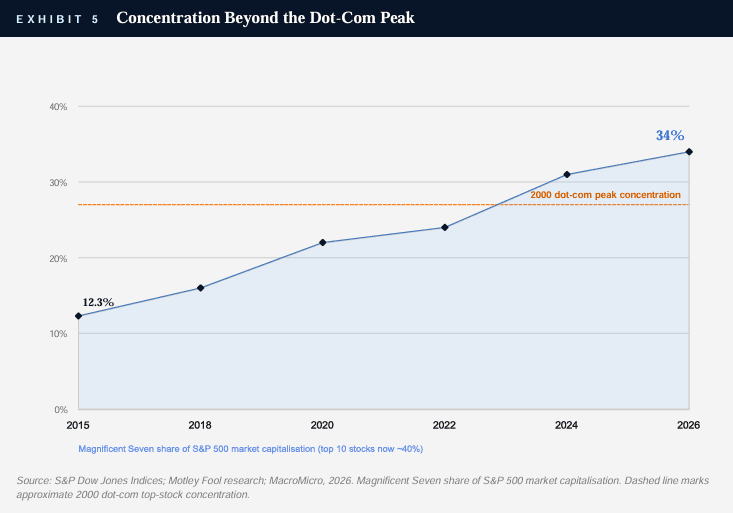

Economics focuses on aggregates. Markets focus on composition. The distinction is routinely ignored, and rarely with more consequence than now. GDP, employment, inflation and investment are all aggregates — yet turning points seldom emerge from aggregates. They emerge from concentration. The composition of growth matters more than the level of growth, and the composition of this cycle is quietly extraordinary.

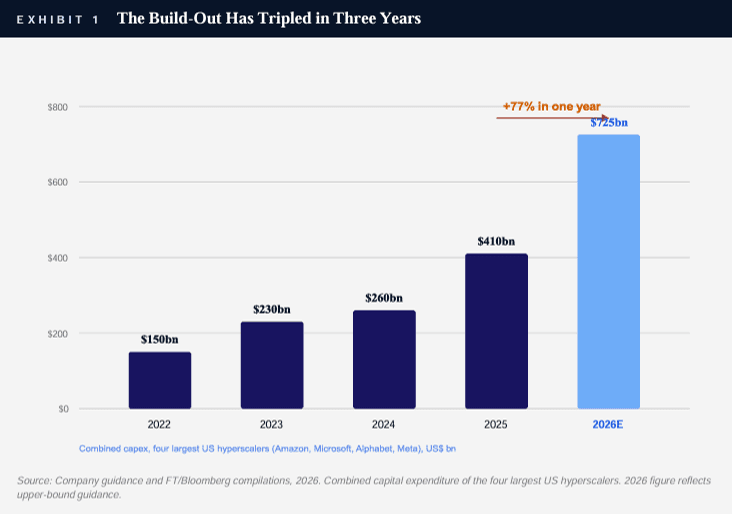

The apparent strength of the US economy masks growing concentration beneath the surface. Consumer spending has moderated. Housing remains constrained. Commercial real estate remains challenged. Bank lending standards remain tight. Consumer credit stress continues to rise. Meanwhile, a small group of companies are investing hundreds of billions of dollars annually into computational infrastructure. Aggregate statistics blend these realities into a single reassuring number. Investors should not.

This is not because the investment is unproductive — quite the opposite. It is because the system becomes dependent on a narrow set of growth engines, and when growth becomes concentrated, forecasting errors become more consequential. Policymakers may therefore be interpreting concentrated strength as broad strength. The economy appears broad. The growth increasingly is not.

The AI mirage

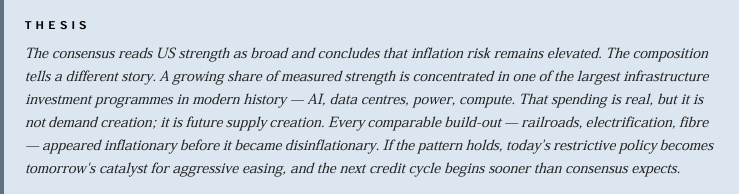

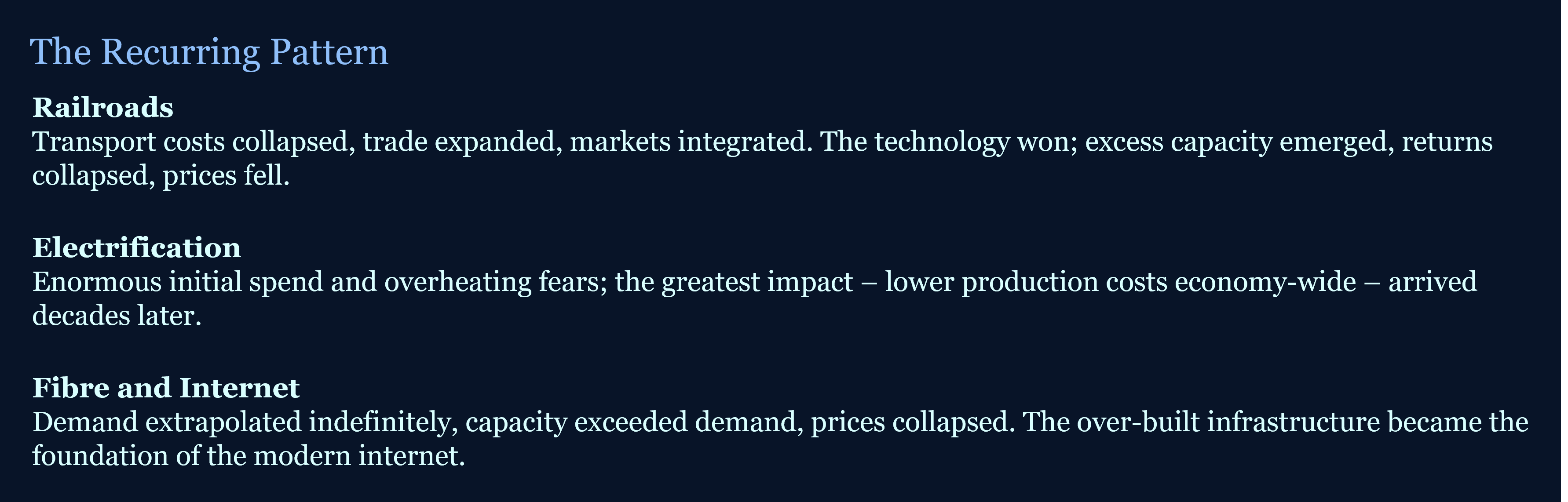

Every major technological revolution begins with construction. Railroads required tracks; electricity required grids; telecommunications required fibre; cloud computing required servers; artificial intelligence requires data centres. The early stages of these transformations look inflationary — construction rises, labour and energy demand rise, capex accelerates, commodity consumption increases, activity expands. Policymakers observe the spending; markets celebrate the growth.

Yet the purpose of the spending is not demand creation. The purpose is future supply creation, and that distinction changes everything. AI infrastructure exists to reduce future costs, to raise future productivity, to lower the marginal cost of intelligence itself. Today’s inflationary impulse therefore contains the seeds of tomorrow’s disinflationary one. The more successful the investment becomes, the larger the eventual supply response. Central banks may be responding to the visible investment while underestimating the invisible future productivity.

The lessons of the capital cycle

The railroad boom transformed the nineteenth century. It reduced transport costs, expanded trade, integrated markets and created enormous wealth — and generated one of the largest investment booms in history. Investors believed demand would be infinite. Capital flowed aggressively, construction accelerated, valuations exploded. The eventual outcome was unexpected: the technology succeeded, the capital cycle did not. Excess capacity emerged, competition intensified, returns collapsed, prices fell, the economy became more productive, and inflation declined.

Electrification followed a near-identical trajectory. Initial investment was enormous, activity accelerated, policymakers worried about overheating — yet the greatest economic impact emerged decades later, as electricity reduced production costs across virtually every industry. The ultimate result was not inflation but lower costs.

The late 1990s offer the closest modern comparison: telecoms laid millions of miles of fibre, investors extrapolated demand indefinitely, and capacity ultimately exceeded demand. The technology narrative was correct; the timing was not. Ironically, the excess infrastructure built during the bubble later became the foundation of the modern internet economy.

Looking for inflation in the wrong place

Perhaps the most important question of this cycle is not whether inflation exists — it clearly does — but where. Conventional analysis focuses on goods and services, yet many symptoms of excess increasingly appear inside financial markets: equity valuations, private market valuations, credit spreads, growth equities, venture capital, digital assets, luxury property. The inflation of this cycle may increasingly be asset-price inflation rather than consumer-price inflation, and that matters enormously.

Asset-price inflation creates wealth effects; wealth effects create spending; spending creates earnings; earnings support valuations; valuations support investment. The process becomes self-reinforcing — what George Soros described as reflexivity. Crucially, reflexive systems operate symmetrically: the mechanism that generates inflation can eventually generate deflation. If financial inflation slows, wealth effects reverse, spending weakens, earnings disappoint, valuations contract, and the cycle reverses — rapidly. Central banks may be fighting inflation in the real economy while inflation increasingly resides in the financial one.

The deflation of intelligence

Every technological revolution reduces the cost of something fundamental. Railroads reduced transport costs; electricity reduced industrial costs; computers reduced information costs; the internet reduced communication costs. Artificial intelligence may reduce the cost of intelligence itself. Large portions of modern economies depend on expensive cognitive labour — analysis, research, programming, design, legal work, customer service, knowledge management — and AI directly targets these activities. Its purpose is cost reduction, productivity enhancement, economic abundance.

The current investment phase therefore represents only the first stage. The second stage is productivity. The third is disinflation. The fourth may be outright deflation across selected sectors. History suggests policymakers consistently underestimate positive supply shocks — and they may be repeating the mistake in real time.

Why higher rates could accelerate lower rates

One of the most counterintuitive possibilities of this cycle is that restrictive policy may raise the probability of future easing. Higher rates first bite on vulnerable borrowers — small businesses, regional banks, commercial real estate, consumers, private equity, leveraged firms. The largest AI investors remain comparatively insulated: they hold enormous liquidity, generate substantial free cash flow, and their investment plans remain intact. Policy therefore weakens large portions of the economy while leaving the primary growth engine untouched.

This creates divergence. Headline data stays resilient; underlying credit conditions deteriorate. Such divergences rarely persist indefinitely — eventually credit dominates, growth slows, defaults rise, risk appetite weakens, and policy reverses. The irony is striking: the longer central banks focus on concentrated investment strength, the greater the probability they inadvertently accelerate the next easing cycle.

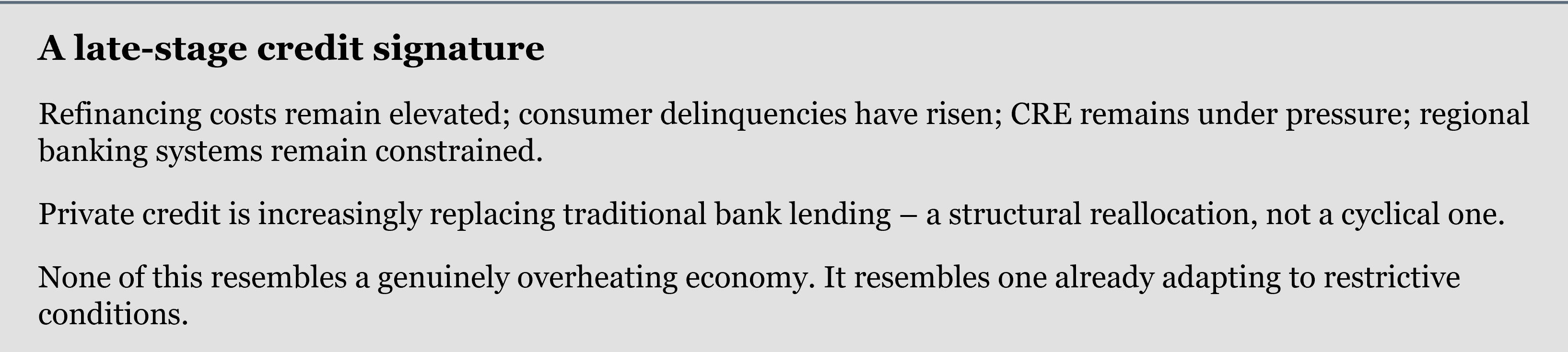

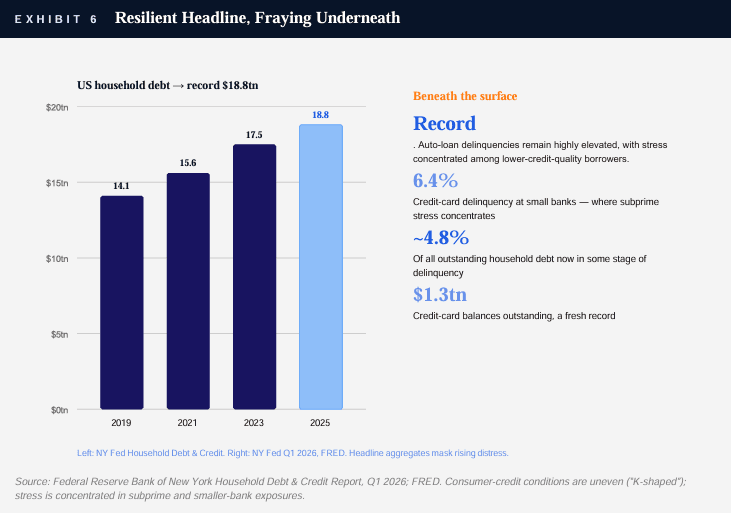

The credit cycle matters more than GDP

Investors consistently overestimate GDP and underestimate credit. Expansions rarely end because GDP weakens; they end because credit creation slows. Credit finances consumption, housing, investment and entrepreneurship — when it contracts, activity eventually follows.

Current conditions increasingly resemble a late-stage credit environment rather than an overheating one: refinancing costs elevated, consumer delinquencies rising, CRE under pressure, regional banks constrained, and private credit steadily replacing traditional lending. The credit cycle may be considerably weaker than aggregate growth suggests.

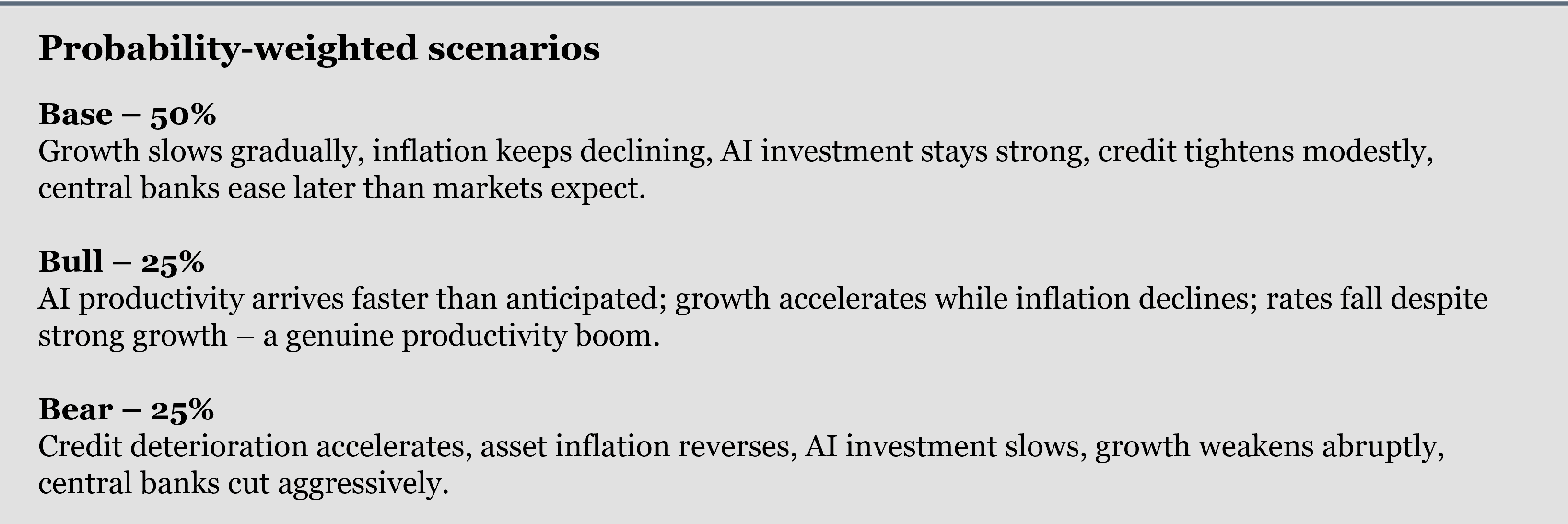

Scenarios and portfolio implications

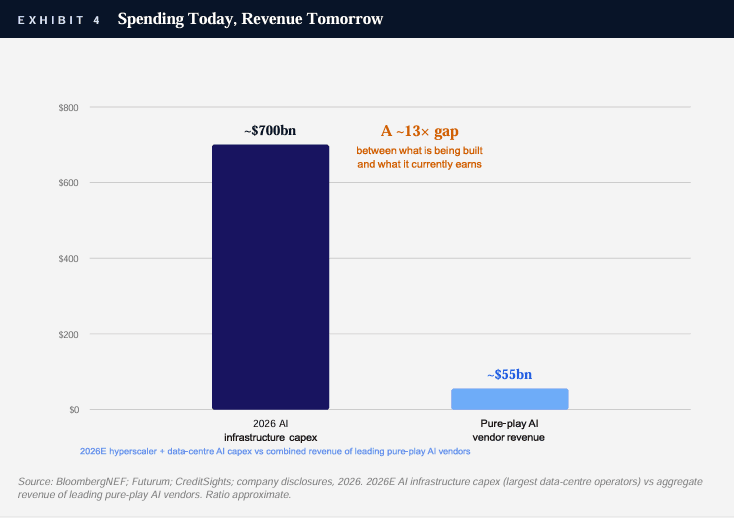

Across all three paths, one distinction stays critical: technological success is not the same as capital-cycle success. Investors should resist the assumption that technological winners automatically become investment winners — history argues otherwise. The most attractive opportunities may instead sit in high-quality credit, long-duration assets, dislocated risk premia, and the productivity beneficiaries rather than the productivity builders. Ironically, the bear case may ultimately create the strongest future investment opportunities — duration itself may become one of the most attractive ways to express the view if the disinflation thesis proves correct.

What to watch

The signal to track is not headline growth but the gap between it and credit. Watch the divergence between resilient aggregates and deteriorating underlying credit conditions — refinancing stress, delinquency trends, regional bank balance sheets, the pace at which private credit is substituting for retreating bank lending. The wider that gap grows while policy stays restrictive, the more loaded the eventual reversal becomes.

Watch, too, the composition of investment itself. If hyperscaler capex continues to carry a disproportionate share of measured strength, the economy is more fragile than its aggregates imply, and the supply response building behind that capex is larger. The first-order effect is investment; the second is productivity; the third is disinflation. Policy is currently calibrated to the first.

The defining policy question of this cycle is deceptively simple. Is the economy genuinely hot — or is a narrow segment of it investing at unprecedented scale? Technological revolutions often appear inflationary before they become deflationary; investment booms often masquerade as economic strength; policymakers often respond to visible demand while overlooking future supply. The economy is not hot. The investment is. Confusing the two may become one of the defining policy mistakes of this decade — and the next credit cycle may begin precisely when policymakers remain focused on the previous one.

This insight follows two pieces that explored similar themes in more detail:

Disclaimer

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell, or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investors or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with their financial professionals. The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Past performance does not predict or guarantee future results. Investing involves risk; principal loss is possible. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. Fasanara Capital Ltd, is authorised and regulated by the Financial Conduct Authority (“FCA”).

Important information on risk

Investing involves risk. The value of any investment and the income from such can go down as well as up, and you may not get back the full amount invested. Changes in the rate of exchange may also cause the value of overseas investments to go up or down. This information represents the views of Fasanara Capital Ltd and its investment specialists. It is not intended to be a forecast of future events and/or guarantee of any future result. Information was obtained from third party sources which we believe to be reliable but are not guaranteed as to their accuracy or completeness. There is no assurance that an investment will provide positive performance over any period of time. This information does not constitute investment research as defined under MiFID.