blog

AI: Boom, Bust, or Productivity Surge? All Three at Once

David Vatchev, Head of Tokenization

18 June 2026

Introduction

In our Fasanara Key Themes for 2026, we argued that AI would not follow a linear path. Instead, it would play out unevenly across markets, the real economy and credit, with financial markets, the real economy, and credit outcomes moving at different speeds.

A few months into the year, this is beginning to play out. While parts of the public market narrative around AI are facing increased scrutiny, underlying adoption across the real economy continues to accelerate. Financial expectations, real-economy productivity, and sector-level disruption are unfolding at different speeds.

Geopolitical fragmentation, capital intensity in AI infrastructure, and rapid technological iteration are reinforcing this divergence across sectors and asset classes.

For allocators, the focus is on distinguishing financial narrative from economic substance, and understanding how AI-driven change translates into real cashflows and risk.

AI in financial markets and the real economy

AI has been one of the dominant drivers of equity market performance in recent years. In 2026, the market is shifting from narrative-led valuations toward closer scrutiny of earnings, monetisation and capital efficiency. As expectations normalise, parts of the market are experiencing greater volatility and selective repricing.

At the same time, AI adoption across the real economy continues to accelerate, with companies deploying AI to:

- automate workflows

- reduce operational costs

- improve decision-making

- enhance productivity

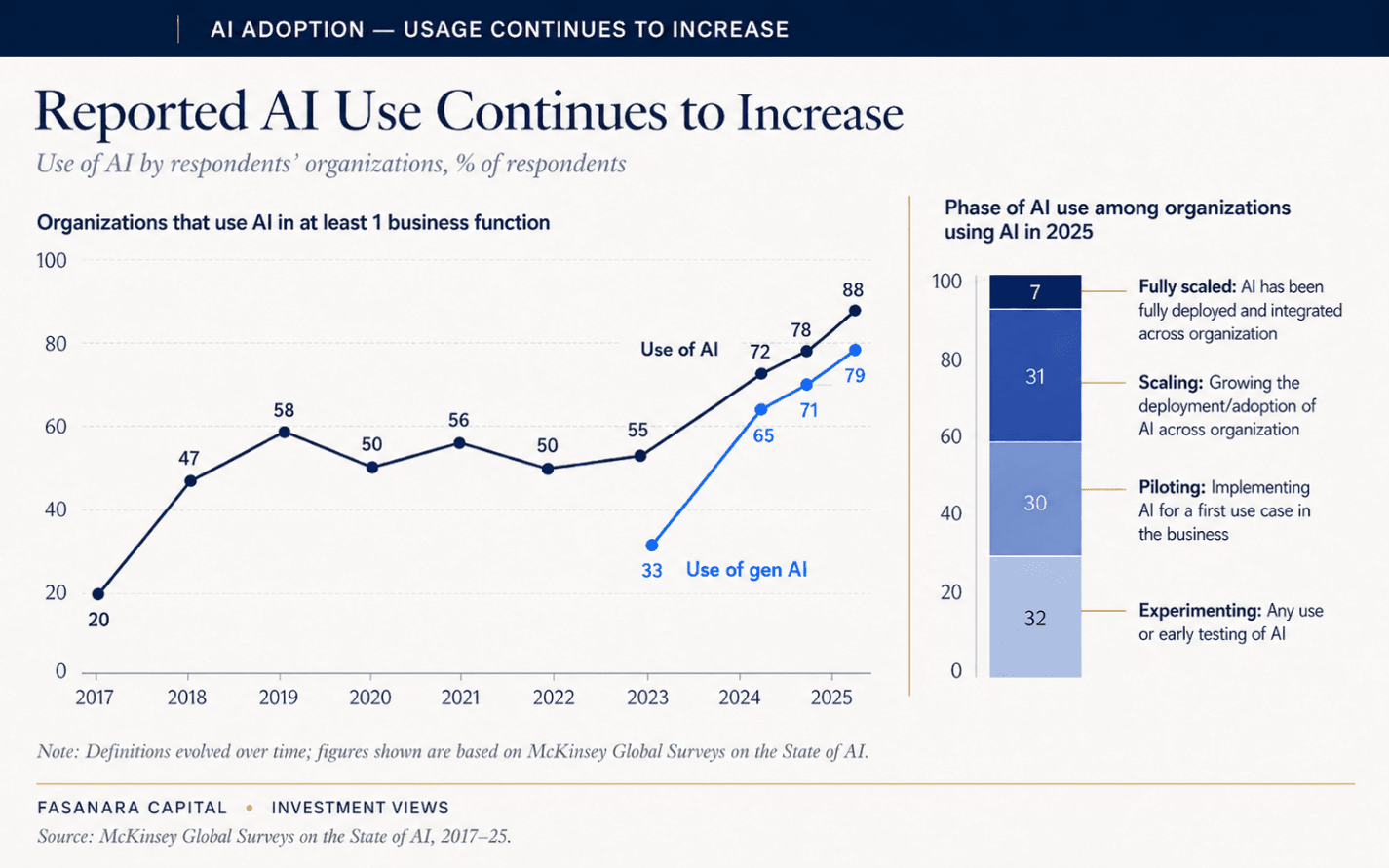

This is increasingly visible across core business functions:

Source: McKinsey

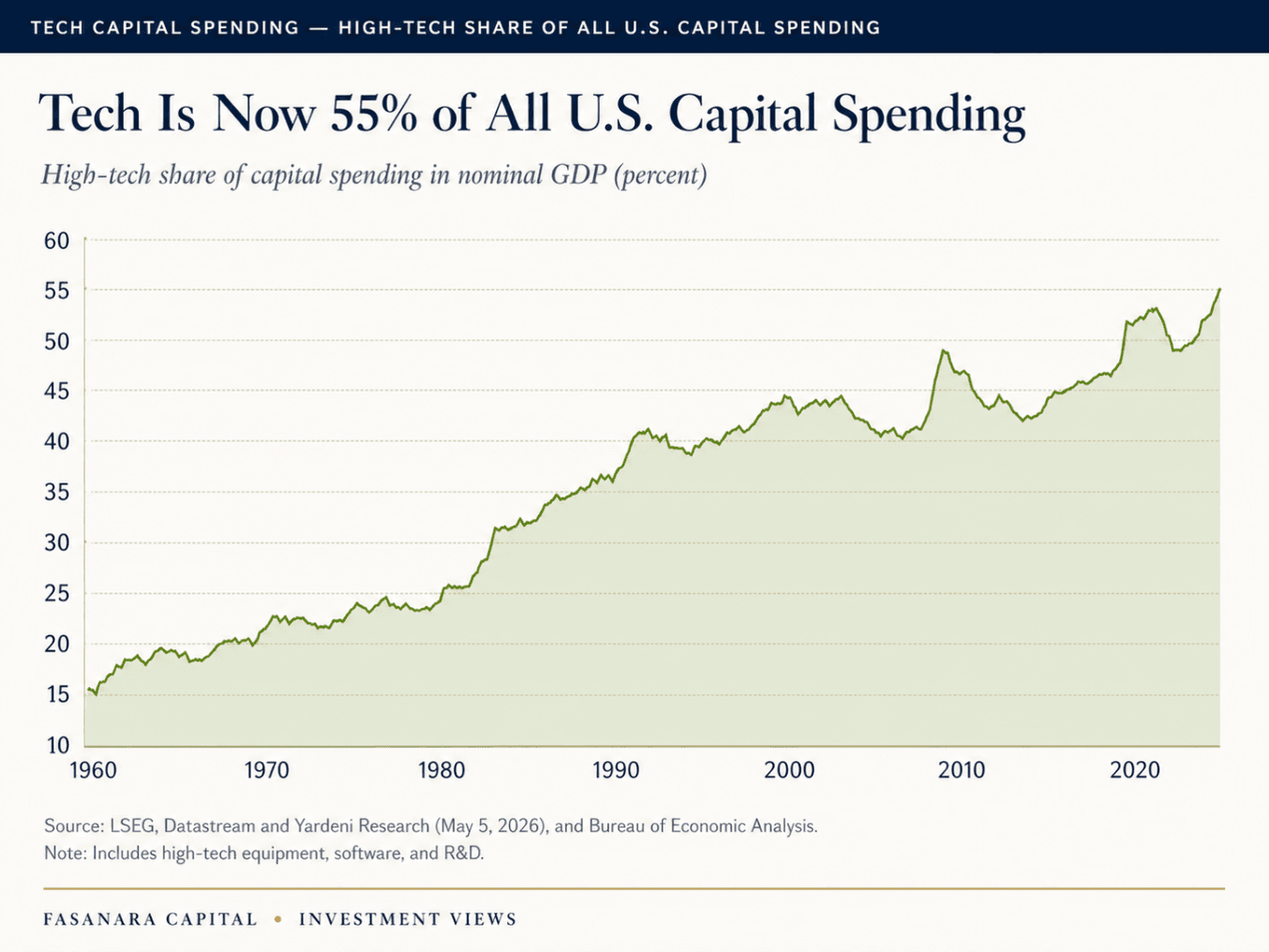

The scale of investment reflects a critical point: intelligence has always been economically valuable. Companies have always competed for talent, data and technology that improve decision making, productivity and market access. AI extends that logic by making advanced analytical and operational capabilities more scalable across the economy.

This is why AI capex has become such an important macro signal. Recent data highlighted by a16z shows high-tech investment, including equipment, software and R&D, now represents around 55% of U.S. capital spending.

Source: a16z

The key distinction is timing. Market expectations can reset quickly, while enterprise adoption tends to be gradual but persistent. The result is a gradual improvement in efficiency and cost structures across a wide range of industries.

Unlike financial markets, where expectations can shift rapidly, real-economy adoption tends to be gradual but persistent. The result is a gradual improvement in efficiency and cost structures across a wide range of industries.

This is driving a structural shift in how value is generated, with productivity gains and cost compression becoming embedded in operating models.

Disinflation and disruption at the same time

AI is pulling the economy in two directions. On one hand, automation and efficiency gains are disinflationary:

- lower labour intensity

- reduced marginal costs

- faster processing and decision cycles

At the same time, AI is highly disruptive:

- business models are being tested

- competitive dynamics are shifting

- revenue visibility is weakening in some sectors

The result is an environment where lower inflation does not equate to stability. Instead, disinflation coexists with volatility, as sectors adjust at different speeds and with varying degrees of resilience.

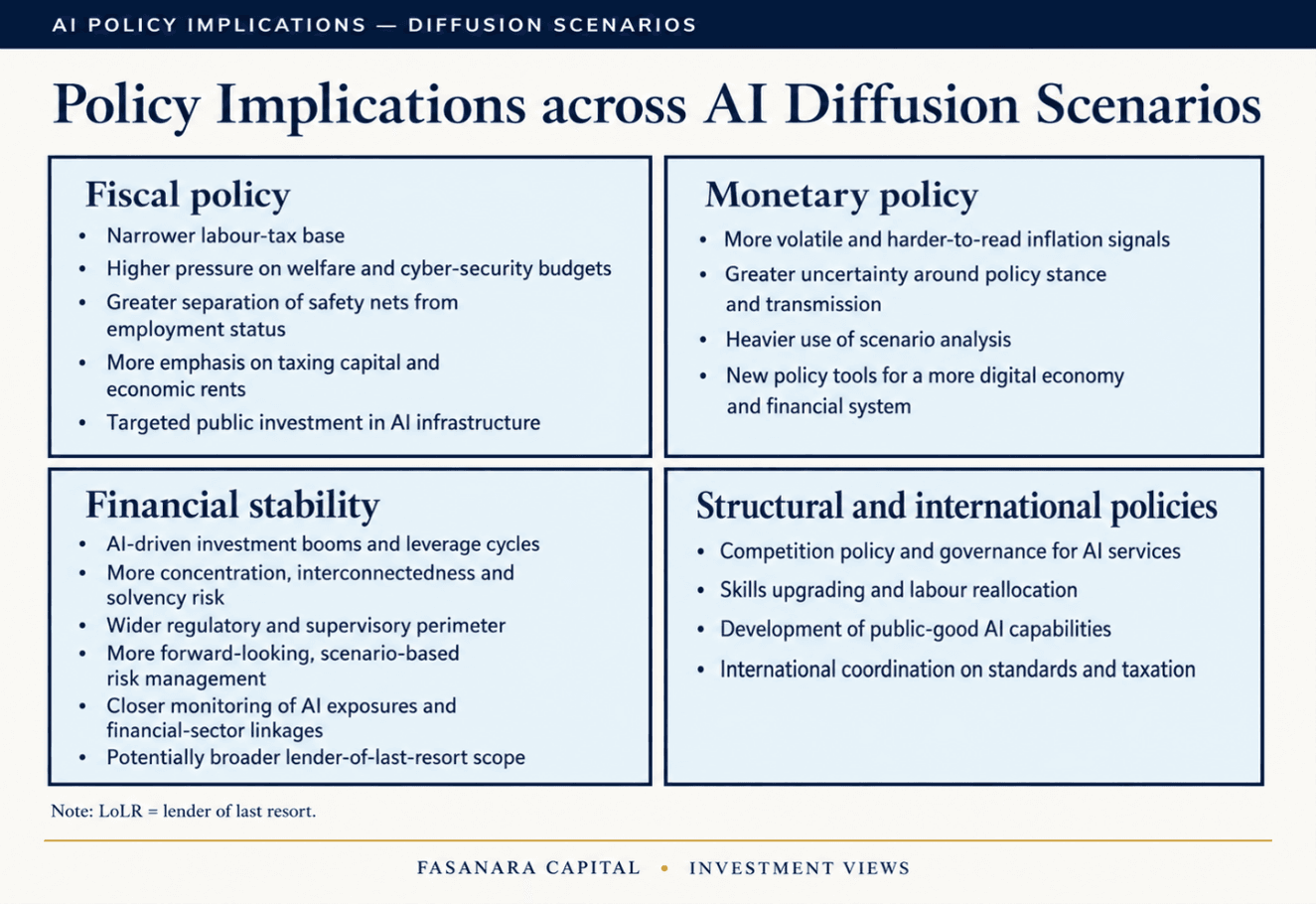

Policymakers are already preparing for this dynamic, seeking to capture AI’s productivity gains while managing transition risks:

Source: IMF

AI and credit market implications

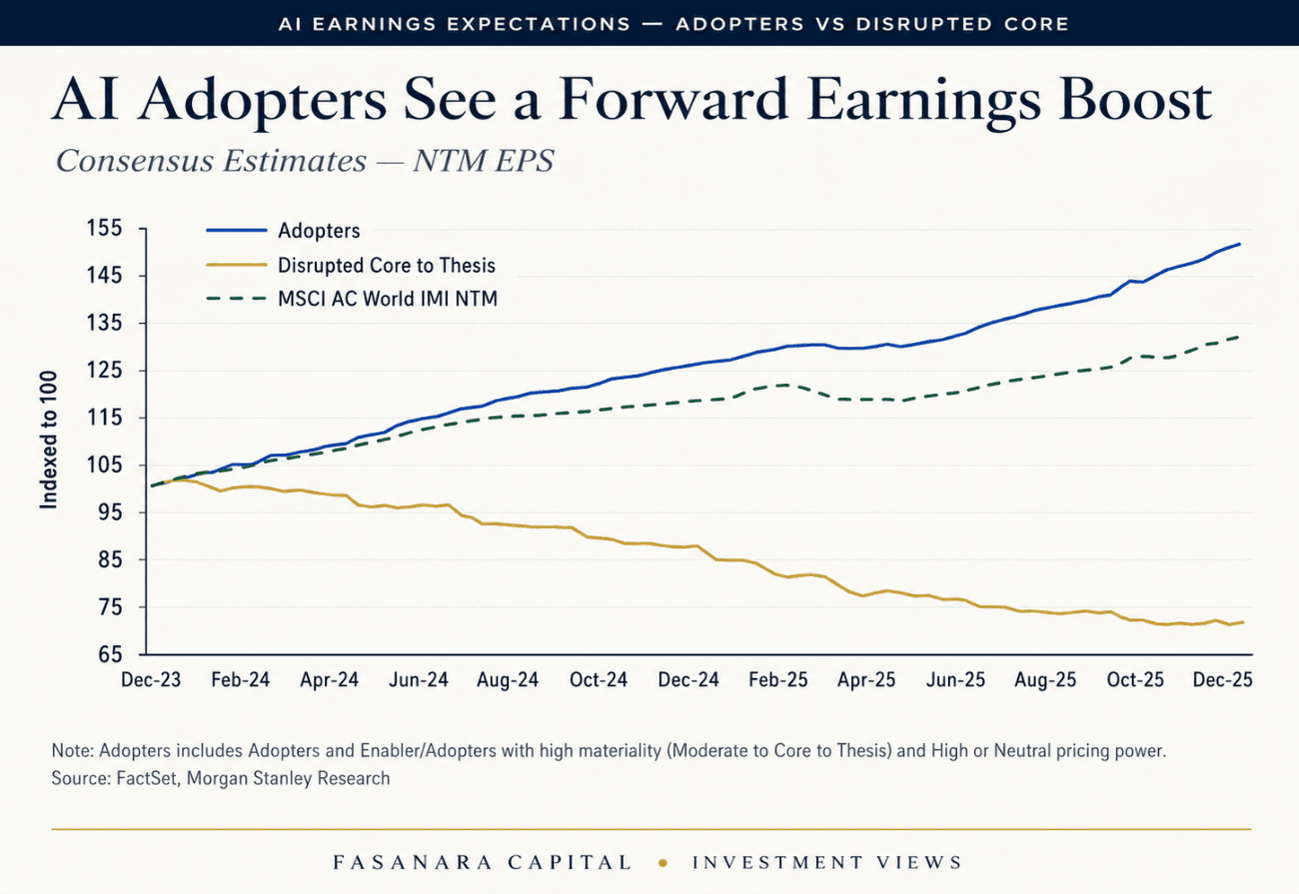

One of the most visible impacts of AI is the acceleration of dispersion across sectors and business models. Software is the clearest example. While AI can improve productivity, it is also compressing pricing power and intensifying competition in parts of the market. This is particularly relevant in SaaS, where growth expectations, valuations and margins are being reassessed.

Source: Morgan Stanley

This is now feeding through into both equity and credit markets, with increasing divergence between companies able to integrate AI effectively and those facing disruption or margin pressure.

The result is widening performance gaps across sectors, strategies and capital structures. Traditional drivers of credit risk, such as leverage and duration, are now interacting with:

- technology-driven disruption

- shifting competitive dynamics

- changing cost structures

The outcome is non linear: some borrowers improve margins and resilience, while others face structural pressure on revenues and valuations. This reinforces the importance of understanding underlying business models and cashflow drivers, rather than relying on historical performance or broad asset-class assumptions alone.

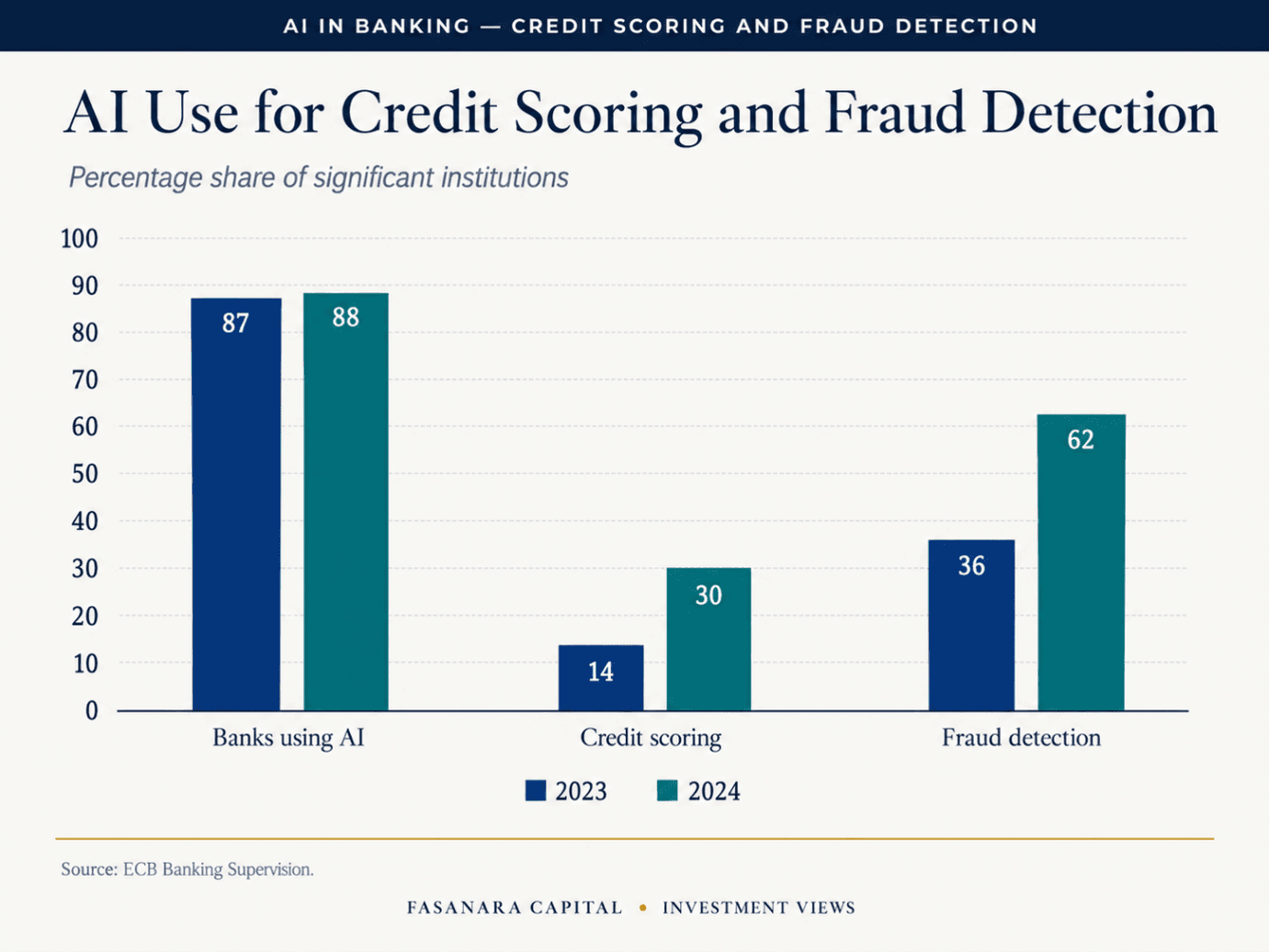

AI as a driver of underwriting and risk management

Source: ECB

The benefits are clear: faster decisions, more granular analysis and earlier risk detection. The governance burden also rises, requiring institutions to update compliance frameworks and introduce dedicated oversight for AI.

Across the industry, AI is increasingly used for:

- credit underwriting and scoring

- anomaly detection

- fraud identification

- portfolio monitoring

- operational automation

Over time, these capabilities are likely to become competitive moats, differentiating platforms that can integrate data, technology and credit expertise effectively.

Conclusion: What this means for allocators

AI is not a single investment theme. It is reshaping returns and risk through multiple channels, simultaneously driving productivity, disruption and volatility.

For allocators, the opportunity lies in identifying where AI translates into sustainable cashflows and resilient business models.

Allocators are increasingly required to:

- distinguish between narrative-driven and cashflow-driven opportunities

- assess sector-level exposure to AI disruption

- evaluate how AI affects underlying borrower resilience

- understand how technology is embedded within investment platforms

As dispersion increases, outcomes become more dependent on selection, structure and underwriting discipline. The key is identifying where AI-driven change turns into durable value.

Disclaimer

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell, or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investors or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with their financial professionals. The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Past performance does not predict or guarantee future results. Investing involves risk; principal loss is possible. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. Fasanara Capital Ltd, is authorised and regulated by the Financial Conduct Authority (“FCA”).

Important information on risk

Investing involves risk. The value of any investment and the income from such can go down as well as up, and you may not get back the full amount invested. Changes in the rate of exchange may also cause the value of overseas investments to go up or down. This information represents the views of Fasanara Capital Ltd and its investment specialists. It is not intended to be a forecast of future events and/or guarantee of any future result. Information was obtained from third party sources which we believe to be reliable but are not guaranteed as to their accuracy or completeness. There is no assurance that an investment will provide positive performance over any period of time. This information does not constitute investment research as defined under MiFID.